VAT Invoice in UAE - Format and Requirement

Table of contents:

- Key Summary

- What is a VAT (Tax) Invoice in the UAE?

- Tax Invoice vs Simplified Tax Invoice (and when each applies)

- VAT invoice requirements in UAE (mandatory fields checklist)

- VAT breakdown on invoice (how it should look)

- VAT invoice format UAE (sample template you can copy)

- VAT invoice number rules (sequence, uniqueness, and best practice)

- Reverse charge note (RCM) on invoices (when required)

- Common VAT invoice mistakes (and how to avoid them)

- Record keeping how long to keep VAT invoices in UAE

- How VAT invoices connect to VAT returns

- FAQs

A VAT invoice according to UAE-Law: A VAT invoice is a legal tax document issued by a VAT-registered supplier to a customer, showing VAT charged on taxable supplies. Under Federal Decree-Law No. 8 of 2017 and Federal Tax Authority (FTA) Executive Regulations, VAT invoices must meet specific content and format rules. Implemented in the UAE after thorough studies demonstrated its lack of negative impact on the country's business sector and investment environment. In fact, the UAE has implemented one of the lowest VAT rates globally.

What is a VAT (Tax) Invoice in the UAE?

The invoice a customer receives for the purchase of a good or service, multiplying the cost price by 5%, calculates the amount of value-added tax (VAT). It is a special type of invoice that includes sales tax. It details the goods and services provided, the price, whether the customer has a credit account, billing information, payment terms, and payment methods. Serves as notification to the customer of the amount of tax due on those supplies, which they must pay to the government.

Tax Invoice vs Simplified Tax Invoice (and when each applies)

Tax Invoice: An essential document to be issued by a registrant when a taxable supply of goods or services is made. Under VAT in the UAE. Require more detailed information to support tax deduction processes and financial review. Hence, 2 conditions to be met for issuing a Tax Invoice are: Issued by all registrants for taxable supplies to other registrants, or The consideration for the supplies should exceed AED 10,000 | A Simplified Tax Invoice: A simplified version of a Tax Invoice, in which fewer details are required to be mentioned, as compared to a Tax Invoice.

Issued by a registrant for taxable supplies of (goods or services) in either of the following 2 cases:

|

| Both are prepared with the same title "Tax Invoice". Simplified Tax Invoice is easier to prepare, as compared to a Tax Invoice. However, for retail businesses and businesses whose supplies to registrants are for a value less than AED 10,000, it is important to ensure that simplified tax invoices are issued for all taxable supplies of goods or services. | |

Helpful Template: Commercial Invoice Template

VAT invoice requirements in UAE (mandatory fields checklist)

- Place “Tax Invoice” prominently at the top in a clear, readable font

- Use the correct invoice type (based on customer & amount)

- Supplier's name, address, and TRN

- Recipient's name, address, and TRN (if VAT registered)

- Unique Invoice Number

- Date of Issue

- Description of goods

- Calculate VAT at 5% (Net Amount × 0.05)

- Total amount, discounts (if any), and gross amount in AED

- Exchange rate used, if invoiced in a foreign currency

Appropriate VAT invoice should be implemented with the Federal Tax Authority UAE to ensure the accuracy, completeness and consistency of invoice data at source, including validation checks and defined exception-handling procedures.

VAT breakdown on invoice (how it should look)

According to UAE Federal Tax Authority regulations, a compliant Standard Tax Invoice must show VAT clearly on a line-by-line basis, with a detailed totals summary at the bottom, especially for B2B transactions. Hence, to avoid incorrect VAT calculation.

How to Calculate your VAT Invoice

By following these steps, you will ensure every invoice you send is accurate and professional.

Example:

Step 1: Create a Detailed Item List

Start by listing every product or service you are charging for, along with its individual price. Crucially, you must decide if each item is standard-rated (5% VAT).

For this guide, we will focus on standard-rated supplies.

Service: Supply and Installation of Power Cable

v Quantity: 1

v Unit Price (Excl. VAT): AED 5,000.00

v Line Total (Excl. VAT): AED 5,000.00

Step 2: Calculate the Subtotal (Excluding VAT)

Add up the total of all your line items before VAT is applied. This is your net amount.

Example: AED 5,000.00 (Supply and Installation of Power Cable)

Step 3: Calculate the VAT Amount

Apply the 5% VAT rate to the subtotal you calculated in Step 2.

Formula: Subtotal × 0.05 = VAT Amount

Example Calculation: AED 5,000.00 × 0.05 = AED 250.00

This AED 250.00 is the VAT you are collecting on behalf of FTA.

Step 4: Calculate the Final Invoice Total (Including VAT)

Add the subtotal (Step 2) and the VAT amount (Step 3) together to get the final amount your client needs to pay.

v Formula: Subtotal + VAT Amount = Invoice Total

v Total Calculation: AED 5,000.00 + AED 250.00 = AED 5,250.00

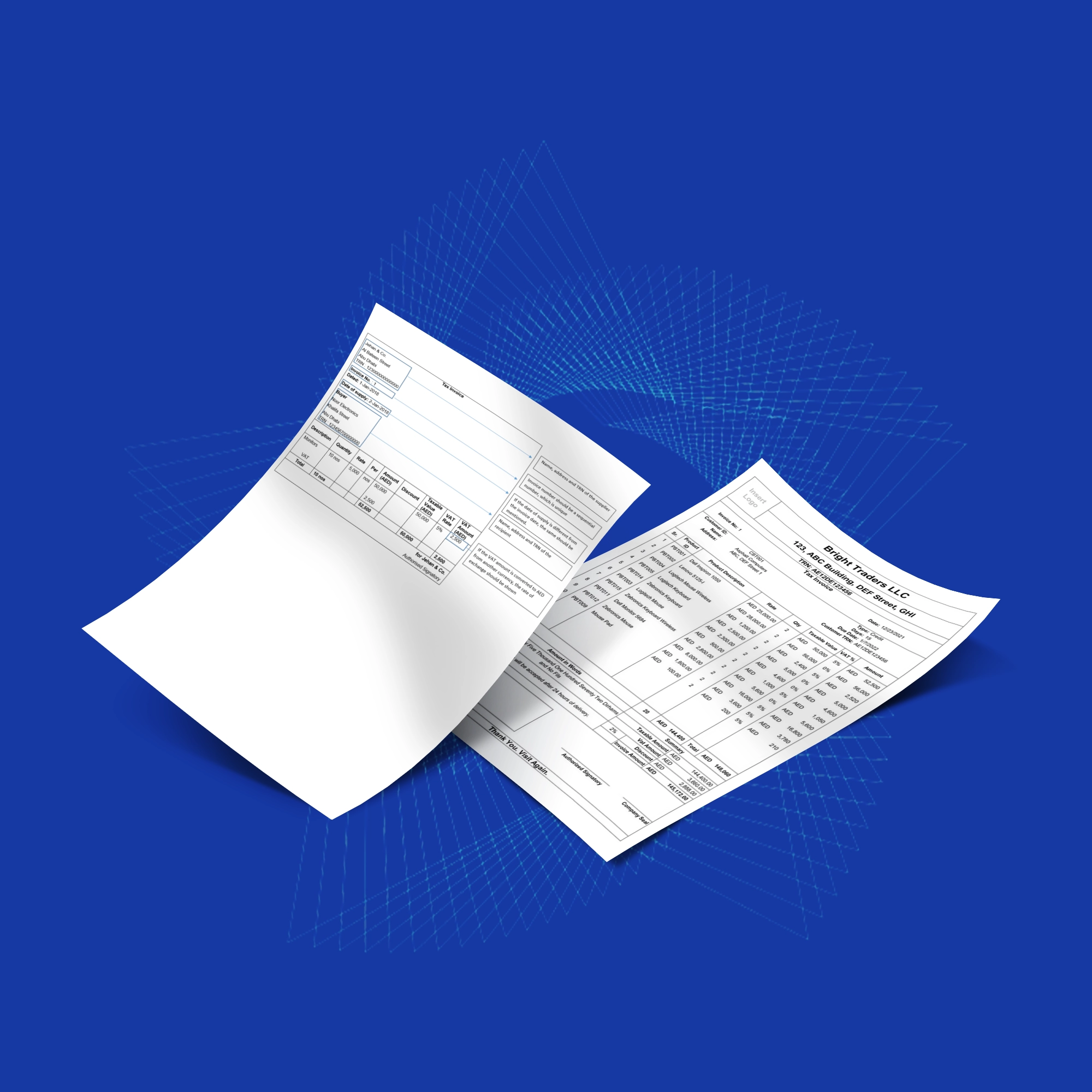

VAT invoice format UAE (sample template you can copy)

VAT invoice Format in UAE is an important activity for all businesses registered for VAT. The Federal Tax Authority (FTA) has specific requirements for VAT invoices that businesses must follow. These requirements help ensure accurate reporting and payment of VAT.

Here are 2 UAE VAT invoice templates matches with the Federal Tax Authority requirements.

Templates

TAX INVOICE CHECKLIST | ||||||||||||||||||||||||||||

1. Tax invoice title should be mentioned on all Invoices issued 2. Tax Registration Number (TRN) to be displayed 3. Price displayed should be inclusive of VAT 4. Amount of VAT charged |

| |||||||||||||||||||||||||||

Tax Invoice | ||||||||||

Jehan Electronic, 7, Al Ittihad Road Emirate: Dubai TRN: 123456789098765 | Invoice No. | Dated 7-Mar-18 | ||||||||

Delivery Note | Terms of Payment | |||||||||

Supplier`s Ref. | Other Reference(s) | |||||||||

Buyer`s Order No | Dated | |||||||||

Buyer Cash Emirate: Dubai Country: UAE Place of supply: UAE, Dubai | ||||||||||

Despatch Document No. | Delivery Note Date | |||||||||

Despatched through | Destination | |||||||||

| Terms Of Delivery | ||||||||||

Sl No. | Description of Goods | Quantity | Rate | Per | Amount | VAT% | ||||

1 | Second Hand Cars | 1 nos. | 20.000.00 | Nos. | 20.000.00 | 0 % | ||||

| Total | 1 nos. |

|

| AED 20.000.00 | |||||

Amount Chargeable (in words) UAE Dirham Twenty Thousand Only (AED 20,000.00) Tax was charged with reference to the profit margin | E. & O.E | |||||||||

VAT% | Assessable Value | |||||||||

|

| |||||||||

|

| |||||||||

This is a Computer-Generated Invoice |

Read also: UAE Standard e-Invoice XML Format

VAT invoice number rules (sequence, uniqueness, and best practice)

Ensure Continuous Sequence: Every invoice that a company issues is given a unique alphanumeric code known as an invoice number. Also, invoice numbers must increase logically with each new invoice (e.g., INV-2026-000123 then INV-2026-000124).

It is important for facilitating efficient record-keeping and ensuring compliance with tax regulations. Help auditors rely on to confirm completeness.

- Avoid gaps in the FTA UAE tax invoice numbering sequence, as this can raise red flags during audits.

- Ensure that all invoice numbers are unique to prevent duplication, confusion, and potential compliance issues with FTA.

Reverse charge note (RCM) on invoices (when required)

For specific transactions like imports, a reverse charge note (RCM) invoice can simplify your business administration. Instead of chasing VAT invoices from multiple overseas vendors, you can calculate and pay the VAT directly.

Example:

Imagine your UAE-based company needs to import services from a supplier in Germany. In a typical domestic deal, a local UAE supplier would simply add 5% VAT to the invoice. But since the supplier is overseas, the tables turn, and the responsibility for handling the VAT shifts directly to you, the buyer.

The process kicks off the moment you make the purchase. The German supplier will send you an invoice, but it won't include any UAE invoice details. What should have a clear note stating that the transaction is subject to the reverse charge mechanism. That little sentence is a crucial flag for your accounting team, letting them know it's time to step in.

Example:

Aviation Corporation LLC, a VAT-registered business in Dubai, imports aircraft maintenance equipment worth AED 800,000 from Freight Aerospace Ltd, a supplier based in France.

The supplier (Freight Aerospace Ltd), issues an invoice for AED 800,000 without charging VAT.

The buyer (Aviation Corporation LLC), calculates VAT at 5% of AED 800,000 (800,000 × 0.05 = AED 40,000).

Aviation Corporation LLC records this AED 40,000 VAT as both:

- Output VAT (payable) to the FTA

- Input VAT (recoverable), if eligible, in the same VAT return.

So, this transaction is recorded under the reverse charge note.

Note: the buyer is in charge of figuring out, declaring, and paying the VAT directly to the FTA even when the supplier is located abroad and is not registered for VAT in the UAE.

Common VAT invoice mistakes (and how to avoid them)

Not adding all required info on the invoice: Make sure that you add supplier and customer names, addresses, and TRNs, Invoice date issue, clear description of goods or services, net amount, VAT rate, and total amount due, and sequential invoice number. | Incorrect VAT calculation (5% Errors): Ensure you apply the correct VAT rate to avoid underpaying or overpaying VAT. |

Misclassification of supplies: Accurately distinguish between standard-rated, zero-rated, or exempt supplies. It’s always worth double-checking guidelines to avoid misclassification. | VAT Invoices not matching VAT Returns: Use FTA systems because it`s automatically compared VAT returns with invoice data, payment timelines. Always remember Mismatch = audit trigger. |

Claiming VAT on non-allowable expenses: To avoid review the FTA list of non-recoverable expenses before claiming input VAT. Only claim VAT for business-related expenses supported by valid tax invoices. | Poor record-keeping and Documentation: Maintain a centralized document management system for invoices, receipts, and credit notes. Back up all files digitally and keep paper copies when required. |

Rightly calculating VAT is a fundamental skill for any business in the UAE. By avoiding these common mistakes, you protect your revenue, maintain professionalism, and stay on the right side of FTA compliance.

Read also: How to file VAT return in UAE

Record keeping: how long to keep VAT invoices in UAE

The FTA requires businesses to retain these records for at least 5 years following the end of the tax period (15 years for real estate transactions). Maintain comprehensive records supporting all VAT positions such as (tax invoices, credit notes, contracts, import/export documents, customs declarations, purchase orders, and general ledgers.) Hence, records may be maintained in physical, electronic, or cloud-based formats, provided they remain readily accessible for FTA audits.

Strong records underpin compliance, facilitate input tax recovery, and enable efficient responses to FTA inquiries.

How VAT invoices connect to VAT returns

Reverse Charge Mechanism (RCM) under VAT eliminates the responsibility for the businesses outside the UAE to register for VAT in UAE. The reverse charge mechanism under VAT is mainly used for transactions from across the border.

In any business, the supplier supplies goods to the customers and collects VAT from the customers, which is later paid to the Federal Tax Authority (FTA). Under RCM, the supplier does not charge VAT to the customer, the buyer or end customer pays the tax directly to the government authority.

The supplier shall not pay VAT on import items, so the obligation of reporting a VAT transaction is shifted from the seller to the recipient. The recipient will have to record the VAT on purchases (input VAT) and the VAT on sales (output VAT) in their VAT return each quarter.

If the supplier is from outside the country and does not have a business in the UAE, VAT is not implemented on businesses which are outside the UAE.

Example:

Recipients who are residents of the UAE and receiving goods from the supplier who is not in UAE are made to pay VAT on reverse charge basis.

FAQs

What does the VAT invoice number mean?

A VAT identification number is the unique number that identifies a taxable person (business) or non-taxable legal entity that is registered for VAT. It is also used to identify the tax status of a customer. For transactions that require an invoice, the VAT identification number of the taxable person supplying the goods or services is mentioned on the invoice.

Does VAT invoice need a unique number?

Yes, according to UAE-Law each tax invoice must carry a unique, sequential number that allows the FTA to identify the document and trace it within your records.

What happens if I don't calculate VAT correctly in the UAE?

Incorrect calculation VAT in the UAE can result in penalties, interest on unpaid VAT, or even suspension of your trade license. If you’re unsure about VAT calculations, Daftra can help.

How long must I keep VAT invoices in the UAE?

Record retention for VAT records generally 5 years, and 15 years for real estate-related records.

Can I issue a simplified TAX invoice for all types of transactions in the UAE?

No. A simplified TAX invoice can only be issued for B2C transactions where the total invoice value does not exceed AED 10,000, or for certain specific supplies allowed under UAE VAT regulations.