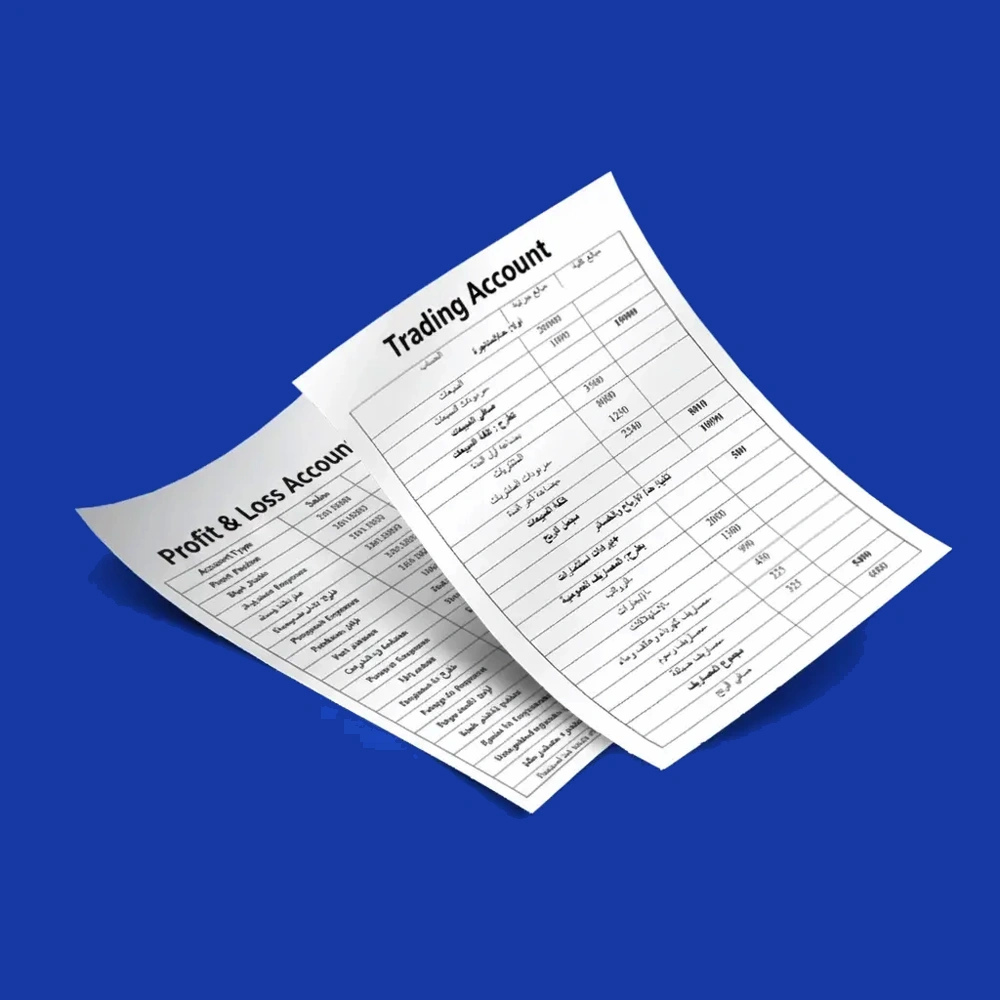

What is the Trading Account and How to Prepare It

Table of contents:

- Key Summary

- What is the Trading Account?

- What is the importance of the Trading Account?

- Components and Elements of the Trading Account

- How to Prepare the Trading Account?

- What Are the Accounting Formulas for Trading Account Items?

- Illustrative Example of a Trading Account

- What Are the Objectives of the Trading Account?

- The Difference Between the Trading Account and the Profit and Loss Account

- The Difference Between the Trading Account and the Income Statement

- When Is the Trading Account Used?

- How Is the Trading Account Reviewed and Audited?

- What Are the Posting Entries in the Trading Account?

- How Does Daftra Software Help in Preparing the Trading Account Automatically?

- Frequently Asked Questions

- Conclusion

How can the process of buying and selling goods and products be evaluated at the end of an accounting period? The answer lies simply in the Trading Account. It is one of the types of final accounts prepared by a company according to its activities, objectives, and nature. These final accounts include the Profit and Loss Account and the Cash Flow Statement.

All companies and institutions worldwide, at the end of any financial cycle, study and evaluate the success of their activities and business operations by preparing reports and final accounts. This is considered the most important step to determine the organization’s status and assess how effectively its operating system generates profits and revenues.

Through our accounting expertise, we provide a detailed explanation of the Trading Account, its importance, and its components. You will also find additional details that can help you manage your financial affairs methodically to achieve profit and business expansion.

What is the Trading Account?

The Trading Account is one of the types of final accounts prepared by a company at the end of the financial year or cycle. The Trading Account represents the first stage in evaluating the results of the company’s business activities, by determining profits and losses, as well as understanding the costs of activities and comparing them.

If sales exceed purchases, the difference is gross profit; if purchases exceed sales, the difference is gross loss. The Trading Account reflects the movement of sales and purchases to identify which type of operation predominates.

The Trading Account also serves as an indicator of the accuracy of closing accounting entries, as it occupies a part of the general ledger. Its purpose is to show the gross profit or loss, which is eventually transferred to the Profit and Loss Account.

What is the importance of the Trading Account?

The Trading Account represents the first stage in preparing the final accounts. Based on it, the rest of the account types are prepared, which highlights the importance of this type of account.

The importance of the Trading Account is as follows:

- Analyzing expenditure and rationalizing expenses: Identifying activities and sectors where significant money has been spent, as well as areas that require more spending, and providing solutions to rationalize expenditure.

- Evaluating profits and losses: Determining the volume of profits and revenues, alongside losses and expenses, which later helps assess the financial performance of institutions and companies before investors and shareholders.

- Assessing company efficiency: Measuring the company’s efficiency in managing business operations such as sales and purchase transactions.

- Comparing and improving financial performance: Results from the Trading Account are used to compare financial performance between different periods and to determine the improvement strategies required, whether in inventory management, sales strategies, pricing, or others.

- Identifying business expansion opportunities: Helping to determine the feasibility of expanding activities and transactions.

In summary, the Trading Account is an important financial tool that helps companies understand the scale and distribution of expenditure, analyze profits and losses accurately, and measure commercial performance efficiency.

It is also used to compare performance across different periods, develop improvement plans, and support expansion decisions to achieve sustainable financial growth and stability.

Components and Elements of the Trading Account

The Trading Account is used in commercial and financial companies, industrial institutions, and many profit-oriented organizations. It consists of several accounts that reflect the movement of purchases and sales within the company. The main components and elements of the Trading Account are as follows:

1- Purchases Account (Trading Expenses)

This appears on the debit side of the account (the right side) and includes:

- Opening Stock: Goods purchased at the beginning of the financial year or remaining stock from the previous year.

- Purchases: All purchases made during the financial year.

- Sales Returns: Returns of goods, which negatively affect revenue by reducing sales by the value of the returns.

- Allowed Discounts: Discounts permitted by suppliers when purchasing goods.

- Selling and Distribution Expenses: Expenses incurred to sell products or services, such as marketing costs, agent commissions, transportation and distribution expenses, salaries and incentives for sales and marketing staff, and rent or purchase of properties, warehouses, and sales centers.

2- Sales Account (Trading Revenues)

This appears on the credit side of the account (the left side) and includes:

- Closing Stock: Goods and items that have not generated any profit or revenue because they were unsold by the end of the year.

- Sales: Revenue from goods and merchandise sold.

- Purchase Returns: Returns of goods, which reduce expenses by decreasing the value of purchases.

- Earned Discounts: Discounts received when selling goods to customers.

In short, the Trading Account consists of two main sides: the debit side, which includes expenses such as purchases, sales returns, allowed discounts, and selling and distribution expenses; and the credit side, which includes revenues such as sales, purchase returns, earned discounts, and closing stock.

The importance of these elements lies in providing a clear picture of the company’s commercial activity and determining the gross profit or loss before accounting for other operating expenses.

How to Prepare the Trading Account?

The data and information from other final accounts, such as the Profit and Loss Account, rely on the results of the Trading Account. Therefore, accuracy in preparing it is essential. The following are the main steps to prepare the Trading Account:

- Record expenses at the beginning of the financial year.

- Close debit and credit accounts.

- Close the closing stock account.

- Close the Trading Account balance.

- Transfer the results of the Trading Account.

1- Recording Expenses at the Beginning of the Financial Year

First, it is recommended at the beginning of each financial year to record all expenses from the start until the moment of preparing the Trading Account, and to keep all records that show the volume of profits and expenses resulting from the company and its activities.

In this step, a closing entry must be recorded for all debit accounts related to goods, by making them credit and the Trading Account debit with their total. The treatment is as follows:

| Particulars | Debit | Credit |

From Trading Account To the following: Purchases Account Freight and Distribtion Expenses Account Advertising Account Commissions Account Customs Duties Account Sales Returns Account Allowed Discount Account | xxxx | xxxx xxxx xxxx xxxx xxxx xxxx xxxx xxxx xxxx |

2- Closing the Credit and Debit Accounts

The next step is to close all credit accounts by making them debit and the Trading Account credit with their total. The treatment is as follows:

| Particulars | Debit | Credit |

From the following: Sales Account Purchase Returns Account Earned Discount Account To Trading Account | xxxx xxxx xxxx | xxxx |

3- Closing the Closing Stock Account

The closing stock account is closed to the Trading Account after it has been inventoried through a separate entry, as it represents an inventory process rather than a balance resulting from an accounting transaction like the previous steps. The closing entry for closing stock is as follows:

| Particulars | Debit | Credit |

From Closing Stock Account To Trading Account | xxxx |

xxxx |

4- Closing the Balance of the Trading Account

Finally, the balance of the Trading Account is closed by determining the gross profit or loss.

- In the case of profit, the entry is as follows:

| Particulars | Debit | Credit |

From Trading Account To Profit and Loss Account | xxxx |

xxxx |

- In the case of loss, the entry is as follows:

| Particulars | Debit | Credit |

From Profit and Loss Account To Trading Account | xxxx |

xxxx |

5- Transferring the Results of the Trading Account

If the credit total exceeds the debit total, the result of the account is gross profit. If the debit total exceeds the credit total, the result of the account is a gross loss.

The results of the Trading Account, whether gross profit or loss, are then transferred to the Profit and Loss Account to determine the net result of operations for the financial year.

In summary, the steps for preparing the Trading Account include recording all expenses from the beginning of the financial year, closing the debit and credit accounts, closing the closing stock account, then closing the balance of the Trading Account, whether it results in a profit or a loss, and finally transferring the results to the Profit and Loss Account.

Performing these steps accurately ensures the correctness of the accounting results for the remaining final accounts.

With the Daftra Accounting Software, preparing the Trading Account has become easier and faster than ever before. The system allows you to automatically and systematically record all purchases, sales, expenses, and discounts, accurately calculating gross profit and loss without the need for complex formulas.

Whether you are tracking opening stock, sales returns, or discounts, Daftra consolidates all this data and provides you with a complete Trading Account report at the click of a button, saving time and effort and helping you make sound financial decisions with complete confidence.

What Are the Accounting Formulas for Trading Account Items?

Preparing the Trading Account relies on a set of accounting formulas that facilitate the calculation of key elements such as gross profit, cost of sales, and net sales. The most important formulas used in preparing the Trading Account are as follows:

- Gross Profit = Net Sales – Cost of Sales

- Net Sales = Sales – Sales Returns

- Cost of Sales = Cost of Goods Available for Sale at the Beginning of the Period – Closing Stock

- Cost of Goods Available for Sale = Opening Stock + Purchases – Purchase Returns

By using these accounting formulas for Trading Account items, organizations can accurately measure their commercial performance and determine the profitability of their activities, which helps in making more informed financial decisions.

Illustrative Example of a Trading Account

The balances of the ledger accounts of one trading company as of 31/12/2022 were as follows:

Opening Stock: 15,000 USD

Purchasing Agents’ Commissions: 1,000 USD

Purchases: 70,000 USD

Sales: 90,000 USD

Purchase Transportation Expenses: 100 USD

Sales Returns: 4,500 USD

Purchase Returns: 3,000 USD

Earned Discounts: 5,000 USD

Allowed Discounts: 2,500 USD

Closing Stock: 10,000 USD

| Debit (USD) | Purchases | Credit (USD) | Sales | ||

| 15,000 | Opening Stock | 10,000 | Closing Stock |

| 70,000 | Purchases | 3,000 | Purchase Returns |

| 100 | Purchase Transportation Expenses | 90,000 | Sales |

| 2,500 | Allowed Discounts | 5,000 | Earned Discounts |

| 4,500 | Sales Returns | ||

| 1,000 | Purchasing Agents’ Commissions | ||

| 15,000 | Gross Profit | ||

| 108,000 | Total | 108,000 | Total |

- Total Debit Side (Purchases) = USD 93,000

- Total Credit Side (Sales) = USD 108,000

If total sales exceed total purchases, then there is a gross profit.

What Are the Objectives of the Trading Account?

One of the most important goals that companies and institutions seek to achieve is increasing capital and profits. Therefore, it can be said that the Trading Account is one of the most important tools that help evaluate a company’s profits and losses.

The main objectives of the Trading Account include:

- Ensuring the accuracy and effectiveness of the company’s commercial and financial transactions: This is achieved by determining the company’s profits and losses.

- Identifying the company’s financial position: By evaluating the company’s condition and activities over a specific accounting period.

- Preventing financial fraud: Limiting fraudulent practices and providing oversight of the company’s accounts and transactions.

- Evaluating performance and determining future investments: Helping investors assess the financial performance of companies and institutions in order to choose the most suitable entity for future investment.

In summary, the objectives of the Trading Account lie in being an effective tool for measuring a company’s profits and losses, accurately evaluating its financial position, contributing to the detection of any financial manipulation through account oversight, and serving as an important reference for investors in assessing the company’s financial performance and making future investment decisions.

Use Daftra's free discount calculator to automatically calculate the discount value and percentage for any price.

The Difference Between the Trading Account and the Profit and Loss Account

The difference between the Trading Account and the Profit and Loss Account appears in the complementary relationship between them. Below is a comparative explanation of the differences between the Trading Account and the Profit and Loss Account.

| Basis of Comparison | Trading Account | Profit and Loss Account |

| Time of Preparation | The Trading Account is prepared at the beginning of the preparation of the final accounts. | The Profit and Loss Account is prepared after the Trading Account. |

| Place of Presentation | The results of the Trading Account appear in the Profit and Loss Account. | The results of the Profit and Loss Account appear in the Capital Account and then in the Balance Sheet. |

| Objective and Focus | Focuses on calculating gross profit or loss by comparing sales revenue with the total cost of those sales during the financial period. | Focuses on calculating net profit or loss over a specific period of time. |

| Method of Calculation | Gross Profit or Loss = Net Sales – Cost of Goods Sold | Net Profit or Loss = Total Revenues – Total Expenses |

The differences between the Trading Account and the Profit and Loss Account demonstrate the sequence and interrelationship between them. The Trading Account is prepared at the beginning of the preparation of the final accounts to focus on determining the gross profit or loss by comparing net sales with the cost of goods sold.

The Profit and Loss Account is prepared afterward and is concerned with calculating the net profit or loss after deducting all revenues and expenses. Its results appear in the Capital Account and the Balance Sheet, highlighting the role of each account in presenting a comprehensive financial picture of the company’s performance during the financial period.

The Difference Between the Trading Account and the Income Statement

The difference between the Trading Account and the Income Statement lies in the scope of each. The Trading Account focuses on calculating direct expenses resulting from purchasing operations against the revenues generated from sales.

The Income Statement, on the other hand, provides a comprehensive overview of the entity’s financial performance by presenting financial information and data derived from both the Trading Account and the Profit and Loss Account.

The Income Statement consists of four elements: revenues, expenses, losses, and profits. It measures net profit or loss after deducting the cost of sales, administrative expenses, commissions, advertising costs, and taxes.

When Is the Trading Account Used?

The Trading Account is prepared at the end of the financial year and is generally used in industrial, financial, and commercial institutions. It represents the first step in preparing the final accounts.

The Trading Account is commonly used when making managerial decisions related to pricing, inventory management, identifying trends and required improvements in commercial performance, as well as determining the most profitable products.

How Is the Trading Account Reviewed and Audited?

The process of auditing and review is a means of preventing fraud and manipulation in financial data. In this context, there are many accounting software solutions that examine and review final accounts, including the Trading Account, which companies prepare to understand their financial position and conduct financial analysis of all their activities.

The Trading Account may also be reviewed and audited manually by accountants. The main steps for reviewing and auditing the Trading Account are as follows:

- Matching the sales amount with the sales shown in the inventory records.

- Ensuring there is no overlap between sales of the previous and current financial years.

- Ensuring there is no overlap between purchases of the previous and current financial years.

- Verifying that the cost of purchases recorded in the Trading Account matches what is shown in inventory records.

- Ensuring damaged goods are excluded from the purchase account.

- Reviewing the gross profit and identifying reasons for any changes compared to the previous year, if any.

- Ensuring that pricing is carried out in accordance with approved specifications and controls.

- Reviewing the statement of pricing bases, if available.

In summary, the Trading Account is reviewed through precise steps that include matching sales and purchases with inventory records, ensuring no overlap between different financial periods, in addition to excluding damaged goods and verifying the accuracy of purchase costs.

It also involves examining gross profit and tracking the reasons for any changes compared to the previous year, as well as ensuring that pricing is applied according to approved controls and reviewing pricing bases, if any, to ensure the accuracy of financial data and prevent any manipulation or errors.

What Are the Posting Entries in the Trading Account?

After recording the three entries, closing accounts with debit balances, closing accounts with credit balances, and recording closing stock, these accounting entries are transferred to the Trading Account. The account is then balanced to determine whether there is a gross profit or loss. Finally, the result of the Trading Account is closed and transferred to the Profit and Loss Account.

How Does Daftra Software Help in Preparing the Trading Account Automatically?

Daftra’s accounting software provides automatic balancing of entries and posts them to the chart of accounts to calculate profits and losses automatically. This helps you issue final accounts, such as the Trading Account and the Profit and Loss Account, with minimal effort.

You can try it yourself with a 14-day free trial, using all of Daftra’s features without the need to add a payment method or incur any costs.

Frequently Asked Questions

What are the direct costs included in the Trading Account?

The direct costs included in the Trading Account refer to expenses that are directly related to the production or purchase of goods and materials used in producing the goods and services sold by the company.

Direct expenses in the Trading Account include wages and salaries of direct labor, costs of purchasing, transporting, and shipping raw materials from suppliers, and packaging costs. Direct expenses are used to determine the Cost of Goods Sold (COGS) applied in calculating gross profit.

What is the role of closing stock in the Trading Account?

Closing stock is used to calculate the cost of goods sold more accurately, which ultimately provides a clearer picture of the company’s commercial performance. The accounting formula is as follows:

Cost of Goods Sold = Opening Stock + Purchases During the Period – Closing Stock

What documents are required to prepare the Trading Account?

Preparing the Trading Account requires maintaining a set of essential documents, including sales invoices, sales return invoices, sales discount records, purchase invoices, purchase return invoices, inventory count reports at the beginning and end of the financial period, and payroll records for direct labor wages and salaries.

What are the most common mistakes when preparing the Trading Account?

Common errors that may affect the accuracy of results when preparing the Trading Account include:

- Relying on inaccurate estimates when valuing inventory leads to overstating or understating closing inventory and consequently affects the cost of goods sold and gross profit.

- Failing to record or include some direct expenses.

- Failing to record goods returned by customers or goods returned to suppliers, as well as neglecting to account for trade discounts granted to customers or received from suppliers, results in unrealistic sales and purchase figures and affects gross profit.

- Failing to update accounting records and journals makes it difficult to track financial transactions and increases the likelihood of errors.

Has the Trading Account been eliminated?

No, the Trading Account has not been eliminated. Rather, it is integrated into the Profit and Loss Account to present a comprehensive view of the company’s financial results. The Trading Account remains one of the basic final accounts prepared at the end of the financial year.

Which accounts are closed in the Trading Account?

Debit side (Trading Expenses):

- Opening Stock

- Purchases

- Transportation and Shipping Expenses

- Advertising Expenses

- Allowed Discounts

- Sales Returns

- Commissions

- Customs Duties

Credit side (Trading Revenues):

- Closing Stock

- Sales

- Purchase Returns

- Earned Discounts

What items are included in the Trading Account?

The following items are included in the Trading Account:

On the debit side:

- Opening Stock

- Purchases

- Sales Returns

- Allowed Discounts

- Selling and Distribution Expenses (such as transportation, advertising, and commissions)

On the credit side:

- Closing Stock

- Sales

- Purchase Returns

- Earned Discounts

At the end, gross profit or loss is calculated as the difference between the two sides.

What is the difference between the Trading Account and the Operating Account?

Both are final accounts, but the Trading Account focuses on presenting revenues and costs resulting from buying and selling operations, where gross profit or gross loss is calculated by comparing sales with the cost of goods sold.

The Operating Account, on the other hand, focuses on calculating direct and indirect production costs, showing the operating result, not just gross profit.

Conclusion

In conclusion, the Trading Account serves as a guiding tool for understanding the commercial performance of any business and evaluating the efficiency of managing core operations related to purchasing, production, and sales. Therefore, business owners and investors should use the Trading Account as a vital tool for making informed financial decisions and enhancing profitability.