Tax Journal Entries: Their Importance and Implementation Methods

Have you ever wondered how accountants organize and analyze financial data to accurately estimate taxes? Would you like to learn more about the processes and challenges that accountants face in tax processing?

Tax journal entries are among the most important operations in accounting, as they play a crucial role in complying with tax laws and achieving financial transparency. The International Federation of Accountants (IFAC) estimates that companies spend up to 24% of their time processing taxes. With the continuous development in information technology and the evolution of tax laws, understanding tax accounting processes becomes increasingly important for both companies and individuals. In this article, we will explore tax journal entry processes in greater detail with practical examples.

What are Tax Journal Entries?

Tax journal entries refer to the series of steps that accountants take to estimate, record, and file taxes accurately and effectively. Recording tax entries is considered a fundamental part of this process, where all amounts payable to the state are recorded, whether representing the Tax Authority in Egypt, the Zakat, Tax and Customs Authority in Saudi Arabia, or any responsible government entity in your country.

Tax entries help clarify the company's tax obligations while determining the expected payment deadlines. This includes all issued invoices, assets, and any other business transactions. In other words, it encompasses everything recorded in the income statement or any other revenues.

Importance of Recording Tax Entries

Recording tax journal entries provides a strong and reliable foundation that can be depended upon for making important financial decisions. When tax data is reliable and accurate, it becomes easier for companies and individuals to identify financial trends and plan for future growth. The following are the main key points regarding the importance of recording tax entries:

Legal Compliance:

Recording tax journal entries helps ensure full compliance with applicable tax legislation in the country or relevant jurisdiction. Consequently, penalties and financial fines that can be imposed on individuals and companies in case of non-compliance with tax laws can be avoided, thereby protecting the financial and legal interests of both individuals and companies.

Accurate Determination of Taxes Due:

Through recording tax journal entries, accountants can accurately determine taxes due. This is accomplished by analyzing financial data, correctly estimating revenues and expenses, and applying applicable tax legislation. This allows companies and individuals to submit accurate and reliable tax returns, reducing calculation errors and increasing opportunities for tax compliance, while reducing the likelihood of audit requests from tax authorities.

Mitigating Financial Risks:

Accurate recording of tax journal entries reduces tax-related financial risks, where companies and individuals can plan their budgets more accurately and effectively, avoiding financial problems that may arise due to incorrect anticipation of tax obligations. This also contributes to improving financial stability and enhancing companies' chances of success.

Improving Financial Transparency:

Accurate documentation contributes to improving the level of financial transparency, providing precise and reliable information to shareholders, partners, and other external parties. When these parties have the ability to access accurate accounting information about taxes, they can make financial and investment decisions better and with more confidence.

Additionally, improving the level of financial transparency enhances confidence in the company or individual, contributing to strengthening relationships with business partners, customers, and investors. Therefore, companies and individuals can benefit from new opportunities for growth and expansion based on their positive reputation.

Saving Time and Effort:

Organizing tax journal entry processes helps save the time and effort required to prepare tax returns and deal with tax authorities more efficiently. When tax entries are documented and financial data is managed in an organized and systematic manner, it becomes easier and faster to prepare and submit tax returns on time.

Furthermore, organizing accounting processes reduces the need for additional procedures to ensure the accuracy of tax data and information, saving the time needed to correct errors and prepare returns correctly. Additionally, the organization contributes to reducing the human effort required to manage tax processes, where some operations can be automated and technical tools can be used to simplify and accelerate processes. In this way, companies and individuals can use the saved time and effort in business development and achieving financial goals instead of spending it on complex and costly tax procedures.

You can use the Daftra accounting software to calculate Value Added Tax when recording sales invoices or automatically recording income tax, which is then linked to the chart of accounts in the Daftra software.

Corporate Income Tax Journal Entries

Income taxes constitute significant expenses for most companies, requiring precise management and accurate accounting records to ensure compliance with tax laws and proper submission of tax returns. Income tax accounting involves recording tax expenses and liabilities based on the company's taxable income.

Two main accounts are used in income tax accounting that contribute to organizing accounting operations and determining taxes due:

- Income Tax Expense: This account records income tax expenses in the income statement. It represents the tax costs incurred by the company based on taxable income.

- Income Tax Payable: This account is credited when recording income tax expenses and represents taxes owed to the government. It contributes to determining the company's tax obligations and providing accurate and timely tax reporting.

Recording income tax in company books is accomplished through several journal entries, including:

Income Tax Recognition Entry:

This entry is recorded to register the tax due on corporate income in the company's general ledger. This amount is deducted from net income to determine the net income subject to tax. There are two main methods for implementing journal entries for taxes imposed on corporate income: the indirect method and the direct method, applied as follows:

Indirect Method:

The company relies on tax payment information found in general financial statements, such as the income statement and balance sheet. It records taxes due based on taxable income, which is calculated according to applicable tax legislation. The indirect method also includes using specific tax rates to calculate taxes due, which may differ from actual rates applied to corporate income. The indirect income recognition entry is applied as follows:

| Description | Debit | Credit |

| Income Tax Expense A/C | xxxx | |

| To Income Tax Payable A/C | xxxx |

Direct Method:

Taxes due are estimated directly based on tax laws and rates applied to corporate income. Taxes due are recorded based on actual revenues, expenses, recoverable tax liabilities, and other specific accounting details. The direct method requires precise knowledge of applicable tax legislation and provides detailed accounting information to calculate taxes accurately. The direct income recognition entry is applied as follows:

| Description | Debit | Credit |

| Profit and Loss A/C (Income Summary) | xxxx | |

| To Income Tax Payable A/C | xxxx |

Corporate Income Tax Account Adjusting Entries:

This entry is recorded to adjust the income tax account at the end of each accounting period. The entry is adjusted based on any differences between taxes due and taxes paid, which may result from using tax liabilities or other tax improvements. When both sides are not equal, it is settled with less than the amount due or more than the amount due, applied as follows:

Settlement with Less Than the Amount Due

When the estimated income tax value is less than the amount due, a negative difference arises. This negative difference is recorded in the retained earnings account as an increase in taxes due. The income adjustment entry is applied as follows:

| Description | Debit | Credit |

| Retained Earnings A/C | xxxx | |

| To Income Tax Payable A/C | xxxx |

Settlement with More Than the Amount Due

When the estimated income tax value is higher than the amount due, a positive difference arises. This positive difference is recorded in the retained earnings account as a decrease in taxes due. The income adjustment entry is applied as follows:

| Description | Debit | Credit |

| Income Tax Payable A/C | xxxx | |

| To Retained Earnings A/C | xxxx |

Corporate Income Tax Payment Entry:

This entry is recorded when paying taxes to the tax authorities. The amount paid is debited from the company's cash account, and the paid item is recorded in expense or liability accounts, depending on the adopted accounting method, applied as follows:

| Description | Debit | Credit |

| Income Tax Expense A/C | xxxx | |

| To Cash A/C | xxxx |

Example

A construction company completed a building project with accounting profitability of 1,000,000 Egyptian pounds and tax profitability of 2,500,000. How should income entries be recorded, knowing that the comprehensive income tax rate is 22.5%?

- Corporate Income Tax = 2,500,000 × 22.5% = 562,500

- Income Recognition Entry

| Description | Debit (Egyptian Pounds) | Credit (Egyptian Pounds) |

| Income Tax Expense A/C | 562,500 | |

| To Income Tax Payable A/C | 562,500 |

- Entry to Close Tax Expense to Profit and Loss Account

| Description | Debit | Credit |

| Profit and Loss A/C (Income Summary) | 562,500 | |

| To Income Tax Expense A/C | 562,500 |

Sales Tax Payable Journal Entries

Sales tax payable journal entries represent the recording of accounting operations related to sales that include sales tax. These taxes are collected from customers through increased product prices. The customer pays the value of the goods plus sales tax to maintain your company's profit margin. Therefore, the total amount is collected from the customer, including sales tax payable, and recorded in the treasury. These entries are recorded as follows:

- At the beginning of the operation, the total amount due from selling products or services is recorded, including sales tax.

- The total sales amount is recorded in the sales account, with sales tax specified as a separate item.

- The sales tax payable amount is recorded as a credit in the sales tax account, and this amount is considered payable to tax authorities.

- The sales tax payable amount is deducted from the total amount due from selling products or services to determine net sales.

- At the end of the accounting period, the sales tax account is settled based on amounts due and paid, and any difference between them is recorded as a debit or credit amount, depending on the situation.

- Cash payments for sales tax are recorded when paid to tax authorities, and these payments are recorded as a deduction from the sales tax account.

Recording sales payable in the company books is accomplished through several journal entries, including:

Sales Tax Recognition Entry:

The sales tax recognition entry is used to record the amount required from the company as sales tax based on completed sales. This entry is recorded as a credit amount in the sales tax account to reflect the amount that must be paid to tax authorities. This amount is determined based on the applicable sales tax rate, and accounting records are updated according to correct tax information, applied as follows:

| Description | Debit | Credit |

| Cash A/C | xxxx | |

| To Sales Revenue A/C | xxxx | |

| To Sales Tax Payable A/C | xxxx |

Sales Tax Payment Entry

The sales tax payment entry is used to record cash payments, checks, or bank transfers paid to tax authorities as sales tax. This entry is recorded as a debit amount in the sales tax payable account to reflect the amount paid. The amount paid is determined based on tax invoices or tax settlements related to sales tax.

| Description | Debit | Credit |

| Sales Tax Payable A/C | xxxx | |

| To Cash A/C | xxxx |

Example

A household goods company's sales invoices during January 2019 totaled $11,000 before tax, and purchase invoices during the same period totaled $9,000 before tax. On February 10, 2019, the company paid the tax amount due for January 2019 to the authority. Given that the sales tax rate on goods sales equals 10%, how should sales entries be recorded?

Sales tax payable amount = Pre-tax sales value × Tax rate 11,000 × 10% = 1,100

Therefore, the cash amount collected from sales = 11,000 + 1,100 = $12,100

| Description | Debit | Credit |

| Cash A/C | 12,100 | |

| To Sales Revenue A/C | 11,000 | |

| To Sales Tax Payable A/C | 1,100 |

Tax Payment Due Sales tax payable account balance of (1,100 - 900 = $200), and when paying this amount to the tax authority, the following entry is recorded:

| Description | Debit | Credit |

| Sales Tax Payable A/C | 200 | |

| To Cash A/C | 200 |

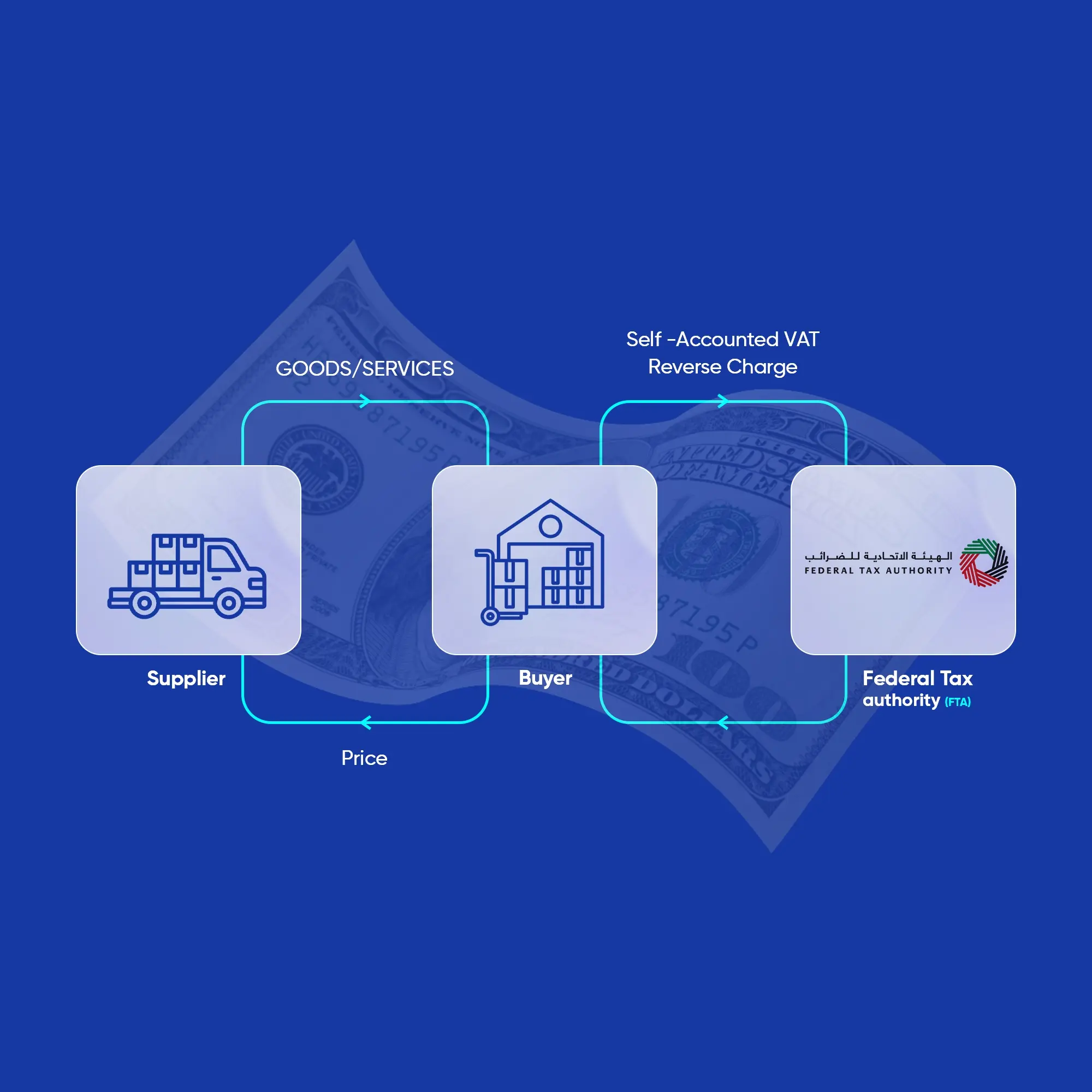

Value Added Tax (VAT) Journal Entries

Value Added Tax (VAT) is a tax imposed on goods and services at different stages of their circulation. For example, when goods are manufactured, VAT is imposed on them, then imposed again when sold to a wholesaler, and a third time when the wholesaler sells to a retailer, until the goods reach the end user.

It may appear that goods are taxed multiple times during these processes, but in reality, goods are taxed only once at each stage of circulation. In other words, the total VAT at all stages of goods circulation equals the final selling price to the end user plus VAT. These entries include the following operations:

- Sales Tax Entry: The total sales amount, including VAT due, is recorded in the ledger. This entry is recorded as a debit amount in the sales and VAT accounts.

- Purchase Tax Entry: The total purchase amount, not including VAT due, is recorded in the ledger. This entry is recorded as a credit amount in the purchases and VAT accounts.

- VAT Settlement Entry: Used to record VAT settlement amounts based on business transactions. This entry is recorded as a credit amount in the VAT account.

- VAT Payment Entry: Used to record cash payments, checks, or bank transfers paid to tax authorities as VAT. This entry is recorded as a debit amount in the VAT account.

Recording VAT in company books is accomplished through the previous entries, which are applied as follows:

Sales Tax Entry

| Description | Debit | Credit |

| Customer A/C | xxxx | |

| To Sales A/C | xxxx | |

| To VAT Collected on Sales A/C | xxxx |

Purchase Tax Entry:

| Description | Debit | Credit |

| Inventory A/C | xxxx | |

| VAT Paid on Purchases A/C | xxxx | |

| To Supplier A/C | xxxx |

VAT Settlement Entry:

The settlement entry is recorded to clear differences between taxes due and paid. If tax paid is greater than the tax due, the difference is recorded as a debit amount to correct the balance. If tax due is greater than the tax paid, the difference is recorded as a credit amount to correct the balance.

If Tax Paid is Greater Than Tax Due

| Description | Debit | Credit |

| VAT Collected on Sales A/C | xxxx | |

| To VAT Paid on Purchases A/C | xxxx | |

| To VAT Under Settlement A/C | xxxx |

If Tax Due is Greater Than Tax Paid

| Description | Debit | Credit |

| VAT Collected on Purchases A/C | xxxx | |

| To VAT Paid on Sales A/C | xxxx | |

| To VAT Under Settlement A/C | xxxx |

VAT Payment Entry:

| Description | Debit | Credit |

| VAT A/C | xxx | |

| To Cash A/C | xxx |

Example

At the end of the year, the owner of a shoe company decided to settle VAT, and the following appeared:

Total sales received: 900,000 Supplies valued at: 600,000 VAT: 15%

Started recording VAT entries on sales due and supplies.

Tax value = 15% × 900,000 = 135,000 Saudi Riyals

| Description | Debit (Saudi Riyals) | Credit (Saudi Riyals) |

| Customer A/C | 1,035,000 | |

| To Sales A/C | 900,000 | |

| To VAT Collected on Sales A/C | 135,000 |

VAT value for purchases from the supplier

Tax value = 15% × 600,000 = 90,000 Saudi Riyals

| Description | Debit (Saudi Riyals) | Credit (Saudi Riyals) |

| Inventory A/C | 600,000 | |

| VAT Paid on Purchases A/C | 90,000 | |

| To Supplier A/C | 690,000 |

Settlement Entry to be Paid

| Description | Debit (Saudi Riyals) | Credit (Saudi Riyals) |

| VAT Collected on Sales A/C | 135,000 | |

| To VAT Paid on Purchases A/C | 90,000 | |

| To VAT Under Settlement A/C | 45,000 |

Therefore, VAT under settlement to be paid = 45,000 Saudi Riyals.

Example of Tax Journal Entries Calculation

A furniture company received supplies valued at 1,000,000 Egyptian pounds with zero deferred value, and total sales due and received amounted to 1,500,000 pounds. After calculating all revenues and expenses, the taxable profit was determined to be 800,000 pounds, knowing that the tax rates imposed according to Egyptian law are as follows:

- Value Added Tax: 14%

- Income tax rate on net income: 22.5%

Corporate Income Tax Entry

Income tax is applied to taxable profit, which equals 800,000 in this case. Corporate income tax = 800,000 × 22.5% = 180,000 Using the indirect method, entries are recorded as follows:

1- Income Tax Recognition Entry

| Description | Debit (Egyptian Pounds) | Credit (Egyptian Pounds) |

| Income Tax Expense A/C | 180,000 | |

| To Income Tax Payable A/C | 180,000 |

2- Entry to Close Tax Expense to Profit and Loss Account

| Description | Debit | Credit |

| Profit and Loss A/C (Income Summary) | 180,000 | |

| To Income Tax Expense A/C | 180,000 |

Value Added Tax Entries

VAT Entries on Sales Due

Tax value = 14% × 1,500,000 = 210,000 Egyptian pounds

| Description | Debit (Egyptian Pounds) | Credit (Egyptian Pounds) |

| Customer A/C | 1,710,000 | |

| To Sales A/C | 1,500,000 | |

| To VAT Collected on Sales A/C | 210,000 |

VAT Value for Purchases from Supplier

Tax value = 1,000,000 × 14% = 140,000

| Description | Debit (Egyptian Pounds) | Credit (Egyptian Pounds) |

| Inventory A/C | 1,000,000 | |

| VAT Paid on Purchases A/C | 140,000 | |

| To Supplier A/C | 1,140,000 |

Settlement Entry to be Paid

| Description | Debit (Egyptian Pounds) | Credit (Egyptian Pounds) |

| VAT Collected on Sales A/C | 210,000 | |

| To VAT Paid on Purchases A/C | 140,000 | |

| To VAT Under Settlement A/C | 70,000 |

Therefore, VAT under settlement to be paid = 70,000 Egyptian pounds

Frequently Asked Questions

What are the Value Added Tax rates in Saudi Arabia?

The Value Added Tax rate in Saudi Arabia is 15%.

What are tax provision entries?

Tax provision entries are entries recorded based on expectations set to cover anticipated costs or losses.

What are withholding and additional tax rates?

Withholding and additional tax rates range between 1% and 5%.

What are some examples of adjusting entries?

Examples of adjusting entries include: accrued salaries not paid by month-end, accounting services provided but not yet invoiced, rent paid in advance for 3 months, and other examples that represent adjusting entries.

What is the commercial and industrial profits tax entry?

Commercial and industrial profits tax entries vary according to the type of item subject to tax. For example, raw materials are subject to 0.5%, and maintenance services 2%.

What is a VAT accrual entry?

A VAT accrual entry is the recording of tax value upon the occurrence of a purchase or sale transaction to establish the amount due according to the accrual principle.

What is a VAT payment entry?

From ........................ A/C (VAT Payable) To Bank A/C

Conclusion In conclusion to this article, we recognize the importance of tax accounting treatments and journal entries in maintaining the integrity of financial software and ensuring compliance with applicable tax legislation. Through accurate and effective estimation and recording of taxes, companies and individuals can avoid financial penalties and ensure their financial stability.

Tax management requires a precise understanding of tax software and local and international laws, in addition to using advanced accounting techniques and best practices in recording and estimation. By employing these tools, organizations can achieve tax compliance and improve financial management.

Finally, companies and individuals must be aware of the importance of tax accounting treatments and journal entries, and work to improve their internal tax processes and software to ensure full compliance and achieve financial stability and business success.