UAE VAT Reimbursement and Disbursement: Key Differences & Examples

Table of contents:

- What is Reimbursement under UAE VAT?

- What is Disbursement (Pure Agent) under UAE VAT?

- Reimbursement vs Disbursement Key Differences (VAT Impact Table)

- VAT Treatment of Reimbursements in UAE

- VAT Treatment of Disbursements (Pure Agent Rules Explained Simply)

- Accounting Treatment How to Record Reimbursement & Disbursement

- Common Mistakes Businesses Make

- How Daftra Handles Reimbursement & Disbursement Correctly

- FAQs UAE VAT Reimbursement & Disbursement

The UAE VAT Law is evolving day by day. But we still stumble upon some fundamental concepts of the UAE VAT Law. When you make transactions, it is essential to be aware of their VAT treatments to ensure proper accounting and reporting in compliance with the regulatory requirements of the region.

We should know first that any commercial transactions, a person may incur expenses and subsequently recover such expenses from another party. The VAT treatment of the subsequent recovery of expenses depends on whether the recovery is a “Disbursement” or “Reimbursement”.

In this article Daftra will discuss the VAT principles for key differences between Disbursement and Reimbursement and the VAT implications under UAE law, provide examples, and treatment.

To avoid confusion, we should first know the difference between Disbursement and Reimbursement.

- Disbursement: payment made on behalf of another party as an agent. And refers to money paid out in the present or future, usually a one-time transaction.

- Reimbursement: involves recovering of expenses that were incurred as a principal. And refers to money repaid in the past, which can happen multiple times over a period.

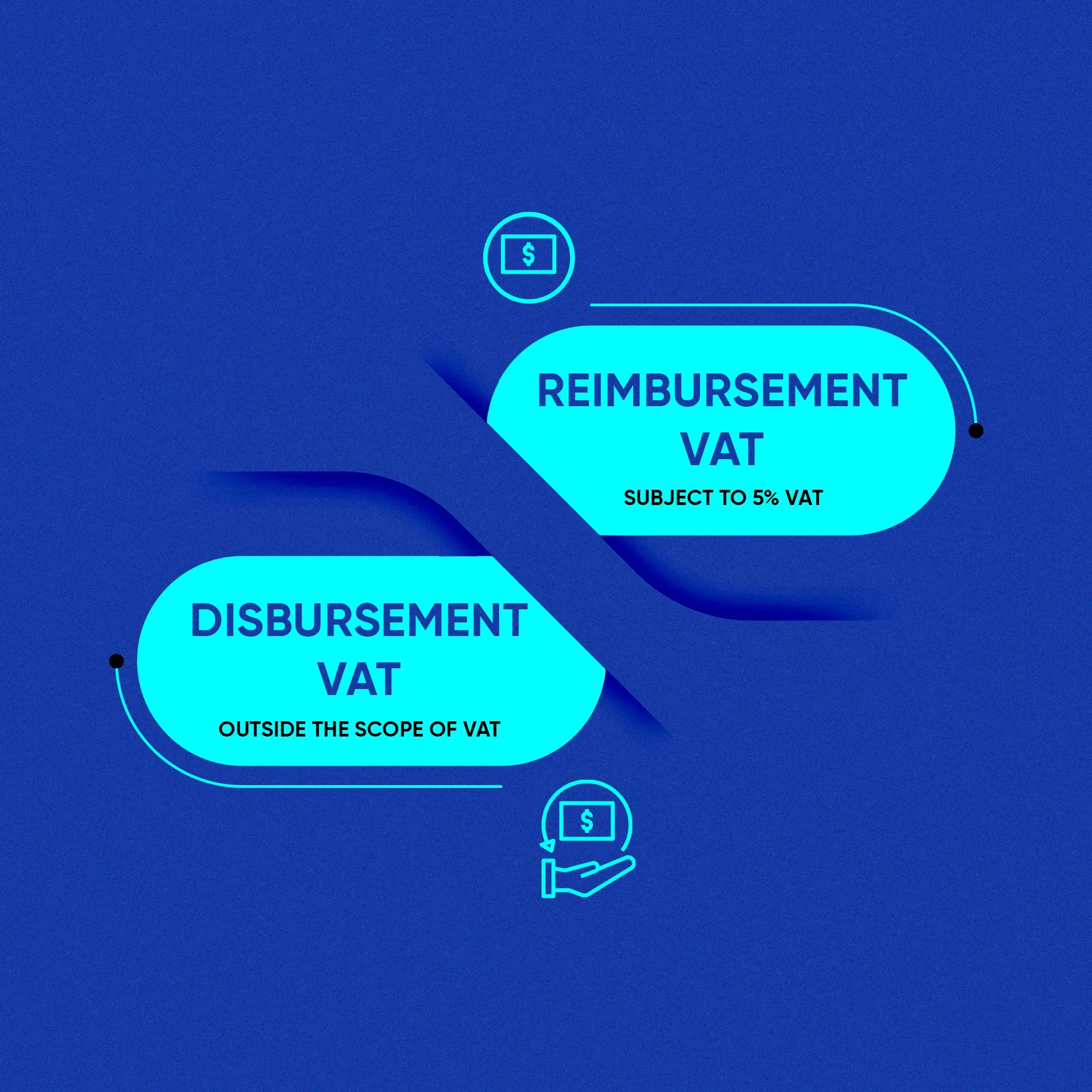

Disbursement and Reimbursement Vat Treatment:

- Disbursement: It is not a supply and falls outside the VAT scope, so it is not subject to VAT.

- Reimbursement: This is a supply and falls within the scope of VAT in which it is subject to VAT.

What is Reimbursement under UAE VAT?

The term “Reimbursement” refers to recovering costs where you acted as a "principal." This means you contracted the service or goods, received the invoice in your own name, and paid the supplier yourself. When you pass these costs to your client, it is treated as part of your main supply.

A reimbursement is treated as part of the consideration for the supply and follows the same VAT treatment as the main supply.

The public clarification issued by the FTA makes it clear that, in the context of UAE VAT law, where a taxable person acts in the capacity of principal, the recovery would generally amount to a reimbursement.

The principles of Reimbursement are:

- Goods or services received by you from the supplier;

- The supplier invoice should be in your name and you are under the legal obligation to pay for it;٠

- Contract for the supply of goods or services should be in your name and capacity;

- Ownership of the goods should be with you before making the onward supply to the other party.

Is reimbursement taxable?

The taxability of reimbursements under UAE VAT depends on whether the company is treated as the principal or the agent in the transaction. This distinction determines whether VAT applies and how the expense is recorded.

Example:

If the expenses of the Hotel incurred are first paid by the Principal and then recharged to the Client, it will be a Reimbursement and subject to VAT when billed to the client. The principal can claim the input VAT in his VAT return on these expenses.

What is Disbursement (Pure Agent) under UAE VAT?

The term “Disbursement” refers to the recovery of payments made on behalf of another.

The public clarification makes it clear that, in the context of the UAE VAT law, where a taxable person acts in the capacity of an Agent, the recovery would generally amount to disbursement, and does not constitute a supply and is therefore not subject to VAT.

It should be noted that you as an agent are not a party to the contract for the supply; you make payment for the supply on behalf of your client. You, as an agent, are not entitled to claim the input VAT since the goods or services are supplied to your client.

The principles of Disbursement are:

- The expense incurred is additional to the other supplies made by the agent to the principal

- The tax invoice was issued by the supplier in the name of the principal and the invoice was received by the principal

- The principal authorized the agent to make the payment on its behalf

- The principal is the actual recipient of the goods or services for which the expense was incurred

- The amount recovered by the agent from the principal should be the exact expense incurred without any mark-up

What is pure agent?

If the person was acting as an agent on behalf of another person while purchasing the goods or services, the recovery of the expenses incurred can be classified as a disbursement transaction. In other case where the person acted as principal, the recovery of expense will be of the nature of a reimbursement transaction.

Is disbursement subject to VAT?

In VAT Disbursement the disbursed amount is not subject to VAT because it is not considered a supply.

Example: If a business pays AED 7000 (including VAT) on behalf of a client and recovers that amount, it does NOT charge any additional VAT.

Reimbursement vs Disbursement: Key Differences (VAT Impact Table)

This table will provide a clear and definitive explanation of the difference between Disbursements and Reimbursements.

Aspect | Disbursement | Reimbursement |

Your Role | Agent, paying on client’s behalf. | Principal, incurring a cost yourself. |

Recipient of Supply | Your Client | You/Your Business |

Third-Party Invoice In... | Client’s Name | Your Name |

VAT on Recharge to Client | Outside the Scope (No VAT) | Standard-Rated (Add 5% VAT) |

Forms part of taxable value | No | Yes |

Input VAT Recovery | No | Yes |

VAT Treatment (Output Tax) | The amount you charge to your client is outside the scope of VAT. You do not add 5% VAT to this charge. | The amount you recharge to your client is considered part of the total payment for your services. You must add 5% VAT to this charge. This applies even if you don't add a markup. |

VAT Treatment (Input Tax) | You cannot recover the input VAT on the third-party supplier's invoice, because the supply was not made to you. Your client can recover the VAT, provided they have the supplier's tax invoice (which is in their name). | You can recover the input VAT on the third-party supplier's invoice (subject to normal recovery rules), because the supply was made to you. |

Example: Reimbursement

MYX Company sent Ali on task as an employee to buy new goods to stock up on inventory. Ali goes to meet the supplier in person and pay for taxi fare out of his own pockets. Ali is the principal in this case because he rode the taxi for himself and was required by law to pay the taxi driver. But as he incurred expenses while doing his job, he can seek reimbursement from MYX.

Example: Disbursement

Importer “X” hires freight forwarding company “Z” to receive his shipment at the Port of Dubai. “Z” pays the import customs duty. And, as the shipment has to be stored in a warehouse at the port for a few days due to an unavoidable customs delay, “Z” covers the warehousing fee as well. Here, “X” is the importer and owner of the goods and is legally bound to pay the customs duty and warehousing fee. “Z” was simply acting as “X”’s agent. Hence, “Z” can recover the expenses it incurred from “X” as a disbursement.

VAT Treatment of Reimbursements in UAE

Reimbursement: Under the current UAE VAT regime, reimbursement of such expenses is considered as a supply and is, therefore, subjected to VAT treatment of the main supply. This means if a business pays AED 5,000 for supplies and VAT is included, it can claim back the VAT amount from the FTA if the supplies are eligible.

When selling goods or services, your business incurs various costs and expenses. Following internal auditing, these expenditures are categorized as the cost of goods or services. The recovery of these costs constitutes reimbursement, and VAT is applicable to the reimbursed amount.

- For example: A logistics company pays storage charges in its own name before shipping goods. The final invoice to the customer includes those charges on top of the transport fee.

VAT Treatment of Disbursements (Pure Agent Rules Explained Simply)

The UAE VAT law defines "Disbursement", where a taxable person acts in the capacity of an agent, the recovery would generally amount to disbursement, and does not constitute a supply and is therefore not subject to VAT.

The term Payment can be treated as a disbursement (Pure Agent) if;

- Invoice or tax invoice should be in the name of the other party

- The other party should authorize you to pay on his behalf

- The other person is the recipient of goods or services

- The responsibility to pay for the goods or services shall be of other party

- The goods or services paid for should clearly be added to the supplies the taxable person makes to him

- For example: A Lawyer pays a government fee for translation or attestation processing in their personal name and later recovers the money. Since the company is not the recipient of the service, the recovery falls outside VAT.

Accounting Treatment: How to Record Reimbursement & Disbursement

In determining the treatment as “Disbursement or Reimbursement”, it is necessary to establish whether you have acted as principle or an agent in incurring the expenses. Where you have acted as an agent, the recovery generally amounts to a “disbursement”. Disbursement does not constitute a supply and is, therefore, not subject to VAT.

But, if you acted as a principle, the recovery would generally amount to reimbursement and will consider to be a part of consideration for the supply and follows the same VAT treatment as the main supply.

Accounting Treatment for Reimbursements and Disbursements

Reimbursements | Disbursements |

| Reimbursed amount forms part of the taxable base. VAT is calculated on the full amount that the customer pays for the service, including reimbursable expenses. | No output VAT is recorded on the recovery. The client, whose name is on the underlying invoice, records the VAT in its own input tax claim subject to the normal rules. |

Common Mistakes Businesses Make

Common Mistakes UAE Companies Make with Reimbursements:

- Misclassifying reimbursements as disbursements

- Inconsistent treatment of staff allowances vs reimbursement

- Dealing with personal expenses as business reimbursements

- Not charging VAT on recharges

- Input VAT is not recoverable by the paying entity

Note: To correct an incorrect VAT return filing in the UAE (Form 201) regarding wrongly treated disbursements, you may submit a Voluntary Disclosure via the FTA EMARATAX portal if the error exceeds AED 10,000. If the error is less than AED 10,000, it can often be corrected in the next return. True disbursements (acting as an agent) are not subject to VAT and should not be in the return, whereas recharges are.

Read also: VAT penalty in UAE

How Daftra Handles Reimbursement & Disbursement Correctly

For more insights into streamlining these processes with automation and real-time analytics, explore Daftra's solutions for revenue recognition, such as:

- Prevent VAT being auto-applied incorrectly

- Separate VAT codes for reimbursements

- Tag transactions as disbursement (pure agent)

- Ensure clear VAT return reporting

FAQs: UAE VAT Reimbursement & Disbursement

Is reimbursement taxable in UAE VAT?

Yes, reimbursement is taxable in the UAE under VAT rules when the company is the actual recipient of the goods or services. VAT must be charged when the company recovers such costs.

Is disbursement subject to VAT in the UAE?

A disbursement (Pure Agent) is generally not subject to VAT on expenses reimbursed by a client, provided specific, as these payments are not considered part of the service provider's taxable value.

What documents do I need to prove a disbursement (pure agent)?

- The client is the recipient of the goods or services.

- The client is legally bound to pay the supplier.

- The invoice is issued under the client's name by the supplier.

- You have to be authorized by your client to pay on their behalf.

- The payment goes for goods or services in addition to the products you supply to your customer.

- You need to get back from your client the exact amount, no markup.

- The payment of the supplier must be clearly stated on the invoice you issue to your client.

Can I claim input VAT on reimbursed expenses?

Yes, you can claim input VAT on reimbursed expenses, provided you are a VAT-registered business, hold a valid tax invoice in your name, and the expense directly relates to making taxable supplies. The VAT is recovered through your VAT return, and the input tax shall be claimed in the period it was incurred.

How should I show reimbursement and disbursement on the invoice?

Under the context of the UAE VAT law, the term "Disbursement" refers to the recovery of payments made by a taxable person on behalf of another person. Payment can be treated as a disbursement if;

- The supplier's tax invoice or invoice is issued directly in the name of the client.

- The client is legally responsible for making the payment to the original supplier.

- The payment should separately be shown on the invoice and the taxable person should recover the exact amount paid to the supplier, without a mark-up.

How do you account for reimbursement vs disbursement?

In the UAE, reimbursement (recover costs incurred as a principal) is subject to VAT, while disbursement (acting as a pure agent to pay on behalf of a client) is outside the scope of VAT.

What happens if “pure agent” conditions are not met?

Treated as reimbursement, so the reimbursed amount forms part of the taxable base. VAT is calculated on the full amount that the customer pays for the service, including reimbursable expenses.