What are Debits and Credits and the Difference Between Them

Table of contents:

- What is a Debit?

- What is a Credit?

- What is the Difference Between Credit and Debit?

- Debit Accounts and Credit Accounts

- How Do Debits and Credits Affect Different Accounts?

- Explanation of the Effect of Credits and Debits in Accounting

- What Rules Govern Credits and Debits in Financial Accounting?

- Some Ways Debit and Credit Transactions Are Used

- Classifications of Credits and Debits

- Various Practical Examples of Debits and Credits

- Debit and Credit Accounts in Daftra

- Frequently Asked Questions

Debits and credits are among the most common terms in financial accounting. No accountant doesn't know these terms. However, there are several reasons that drive us to discuss debits and credits, not only because financial accounting is based on debits and credits.

But also because the debit and credit accounts of any entity, and identifying these accounts and not confusing them, is a major task to prevent errors in the entity's various accounts, such as journal entries, general ledger, and financial statements.

One of the most important things for any business owner is knowing the money coming in and going out of the entity, which is why the terms debit and credit emerged, and this leads to accuracy in various records and the financial position of the institution. Therefore, we will learn about credits and debits in detail.

What is a Debit?

A debit is considered the money incoming to the account and therefore represents debts owed by the entity. The other party that provides the money is called the creditor and can be individuals or institutions. This money is considered an increase in expenses for the entity.

For example, if the institution purchased furniture for 50,000 SAR and paid only 20,000, then the institution owes 30,000 SAR. Therefore, we see that the debit account is the account that requires the entity to pay the required money.

Synonyms for "debit" include borrower, debtor, obligated, liable, or debt holder. All these terms are synonyms for the concept of debit in accounting, which is the party that is obligated to pay an amount of money to another party.

What is a Credit?

A credit is considered the money going out of the account, and the crediting party is the debt holder. The party that was given the money is the debtor. For example, A customer was given 5,000 SAR as an advance. Here, the institution is considered a creditor and the customer is the debtor. Therefore, a credit is money granted by the entity.

Synonyms for "credit" include lender, giver, or creditor. All these are synonyms for the term credit, which is the entity, party, or person that provides credit to the other party, with this credit to be recovered in the form of money or goods, whether with interest or not, within a specified time period.

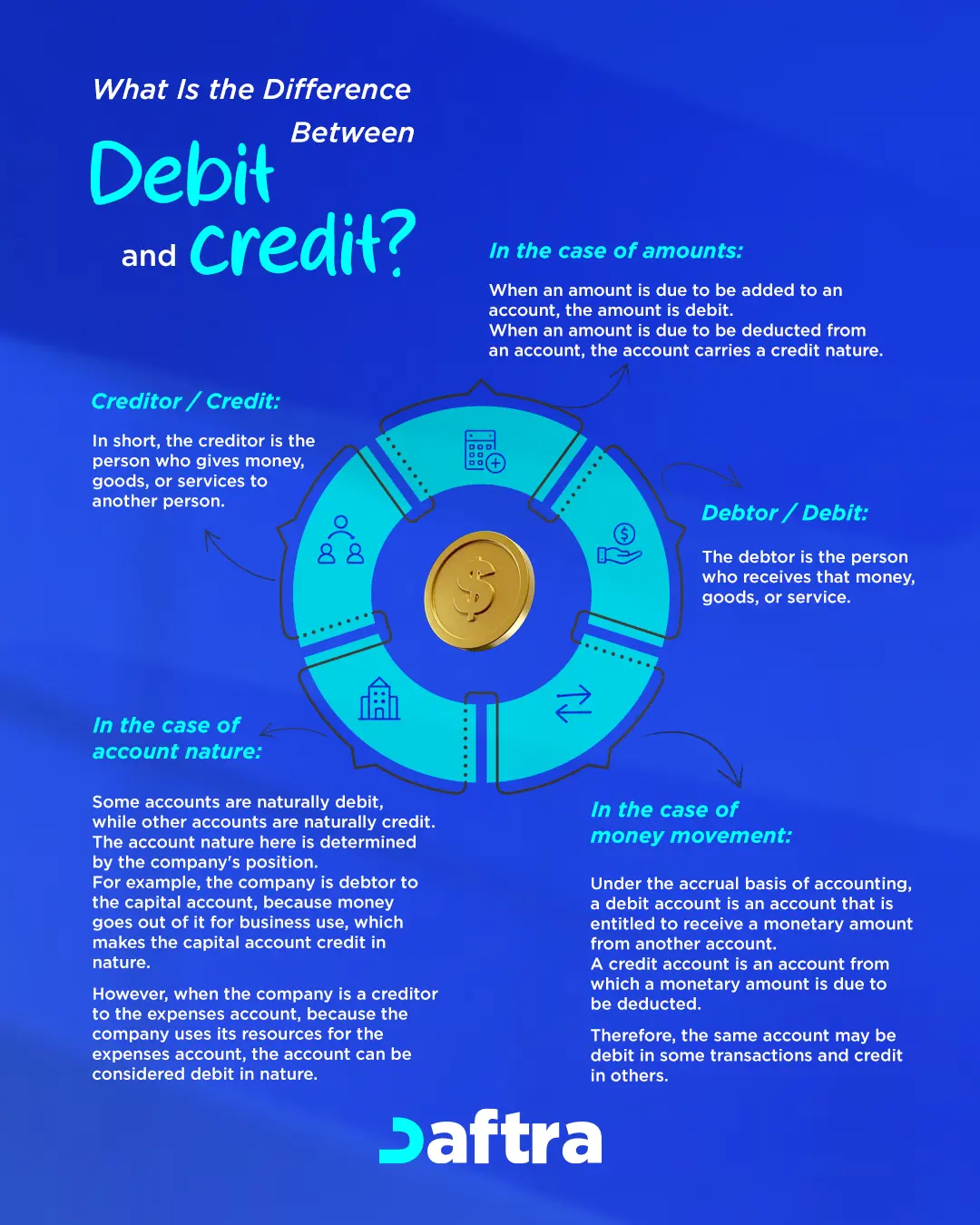

What is the Difference Between Credit and Debit?

To understand the difference between credit and debit in accounting, you should realize that both definitions are merely attributes that amounts and accounts can carry, and they are a practical application of double-entry bookkeeping theory. The difference between credit and debit can be summarized through the following comparison:

| Basis of Difference | Credit | Debit |

| Classification of Amount Status | When an amount is due to be deducted from an account, it is classified as a credit amount. | When an amount is due and must be added to an account, it is classified as a debit amount. |

| Nature of Accounts | The company is indebted to the capital account, from which money flows out for its use, making the nature of the capital account a credit. | When the company is a creditor of the expense account, for example, if the company spent 500 Saudi Riyals on utilities costs, this amount is recorded as an increase to the expense account, and its nature is a debit account. |

| Circulation of Amounts | The credit account is an account from which a monetary amount is due to be deducted. | Applying the accrual principle, the debit account is an account to which a monetary amount from another account is due to be added.d |

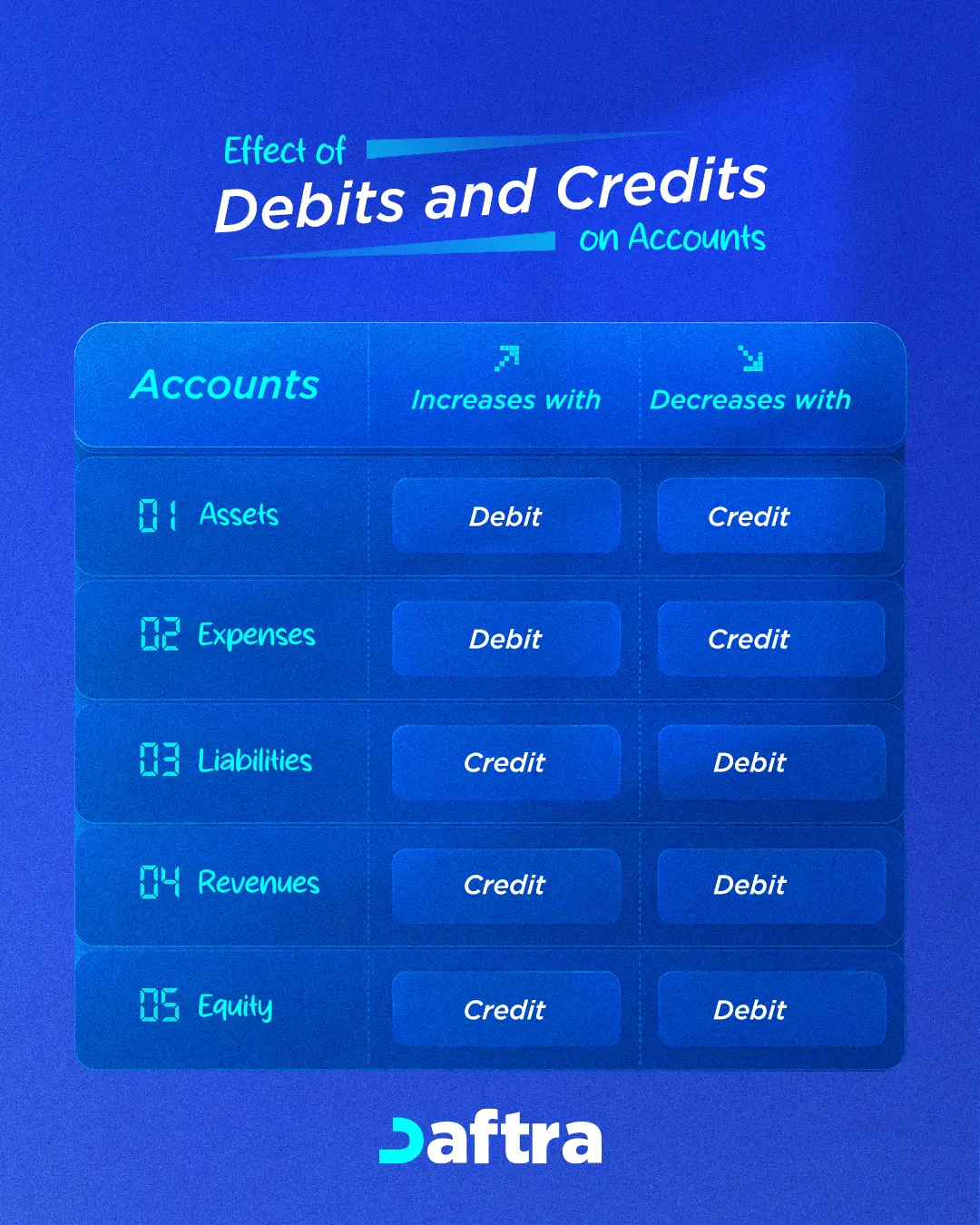

Debit Accounts and Credit Accounts

There are five basic accounts that explain the debit and credit rule for any entity. These accounts are used to track money that is received or given within the framework of business transactions, and these accounts are:

1- Assets:

These are the resources owned by the institution that have value, whether they are land, cash, furniture, buildings, inventory, or other various asset accounts. These accounts are affected when they increase or decrease and can be debited at one time and credited at another, depending on their status.

If land is purchased specifically for the entity, then the land account is considered a debit. But if one of the assets, such as furniture, is sold, then the furniture becomes a credit.

2- Expenses:

These are the costs that occur during business operations, such as wages, salaries, and many operating expenses specific to the entity.

Most of the time, these expenses come as a debit account, because expenses by nature are amounts that flow out of the entity and become a debt that must be paid.

3- Liabilities:

These are the amounts owed by the entity to another person or institution, such as accounts payable, like accrued wages.

Therefore, any obligation on the institution is considered a liability account. Note that liability accounts, when increased, are considered credit accounts, but when decreased, are considered debit accounts.

4- Revenues:

These are the funds that flow into the entity through sales. Revenues come as credit accounts, and when revenues increase, they become credits, but if they decrease, they become debits.

5- Equity:

These are assets minus liabilities and are considered the owners' rights after net assets. They can be: treasury stock, retained earnings, and paid-in capital. Therefore, if these accounts increase, they are considered credit accounts, but if they decrease, they are considered debit accounts.

Read also: Accounts Payable and Accounts Receivable

How Do Debits and Credits Affect Different Accounts?

The debit and credit table shows the effect of the entity's different accounts as either a credit or a debit, and this depends on the increase and decrease of the account.

Therefore, we find, for example, that when expenses increase, this means that the entity has incurred a new debt. But in case of a decrease, the entity has paid part of the expenses and thus became credited with that amount.

| Account | Increases | Decreases |

| Assets | Debit | Credit |

| Expenses | Debit | Credit |

| Liabilities | Credit | Debit |

| Revenues | Credit | Debit |

| Equity | Credit | Debit |

Explanation of the Effect of Credits and Debits in Accounting

- When adding a debt to the debit account, the debt amount increases in all debit accounts and decreases in credit accounts. Examples of this include expense accounts, asset accounts, and dividend accounts.

- In credit accounts, when the value increases, the account becomes a credit, and when it is reduced, it becomes a debit. The accounts to which this rule applies are: revenues, liabilities, and equity.

- In business transactions, the total debit amounts must equal the total credit amounts. Therefore, if the account is not balanced, it is not accepted in any of the various accounting books or in the financial statements.

The reason for the effect of credits and debits on different accounts is due to the famous accounting equation:

Assets = Liabilities + Equity

Therefore, debits must be understood well so that they are determined correctly from the beginning and no errors occur, from journal entries to financial statements, whether the balance sheet or income statement.

What Rules Govern Credits and Debits in Financial Accounting?

Credits and debits in financial accounting are governed by a set of basic rules that differ according to the type of account itself. These rules ensure the accuracy of accounting records and the transparency of financial reports created based on data from these records. The rules governing credit and debit accounts are:

1- Double-Entry Principle

Every financial transaction entered must affect at least two accounts, so that the values entered in both the credit and debit sides are equal.

2- Account Identification

Accounts must be clearly classified and identified, where credit accounts are usually considered liabilities, while debit accounts are considered assets. In recording credit and debit accounts, increases in assets are recorded as debits, while increases in liabilities or equity are recorded as credits.

3- Account Reconciliation

Regular reconciliation of credit and debit accounts such as bank statements and supplier reports, with the aim of ensuring the accuracy of financial records.

4- Account Documentation and Reporting

Every credit or debit transaction must be documented in the appropriate and correct account, which helps in tracking transactions and auditing accounts. These accounts must be reported accurately and transparently in financial reports, which helps in evaluating the financial position and making sound decisions.

Some Ways Debit and Credit Transactions Are Used

There are several methods used in accounting transactions with different examples:

1- Cash Sales:

Here, the cash account increases and therefore becomes a debit, while the revenue account increases and therefore becomes a credit.

2- Cash Received from Accounts Receivable:

So the cash account becomes a debit, and accounts receivable becomes a credit.

3- Supplies Purchased from Supplier:

Her supplies are considered expenses and therefore increased, becoming a debit, while the cash account here is a credit because it decreased by the value of the supplies.

4- Employee Payroll:

He, regarding the cash account, decreased by employee salaries so it becomes a credit, while the salary account increased so it's a debit.

5- Credit Sales:

Accounts receivable becomes a debit, and the revenue account becomes a credit because revenues increased here.

6- Purchasing Inventory from Supplier for Cash:

The inventory account increased, becoming a debit, while the cash account decreased, becoming a credit.

7- Purchasing Inventory from Supplier on Credit:

The inventory account is considered a debit, while accounts payable becomes a credit.

Classifications of Credits and Debits

Classifying debit and credit accounts in accounting has great importance in assessing financial risks, improving cash flow management equitably, analyzing financial performance accurately, and facilitating auditing and review processes for accounts and financial reports. The following is a classification of the most prominent accounts used in financial accounting and determining whether they are credit or debit:

- Profits: Profits are classified on the credit side of the income statement because they increase the entity's equity.

- Notes Payable: Notes payable are credits because they represent an obligation on the company that must be paid to the other party, and notes payable are issued as debt in the company's accounting records when issued.

- Purchases: Purchases are classified on the debit side because they result in an increase in assets and expenses.

- Customers: Customer accounts are usually debit, except in the case of advance payments from customers, which are classified as credit because they represent an obligation on the company toward customers.

- Allowances: Allowances are credited because they reflect an expected loss to the company, which increases the value of debts and obligations.

- Treasury: Treasury is classified as debit when receiving cash and payments, and treasury is credit when disbursing or withdrawing cash from it, resulting in a decrease in treasury funds.

- Cash: Cash is treated as credit or debit classification the same as treasury, so cash is debit when it increases, and credit when it decreases.

Various Practical Examples of Debits and Credits:

Here we will clarify some operations in double-entry bookkeeping:

- Company (1) sold its product to a customer for 5,000 SAR in cash.

The result of this operation is as follows: Cash increased by 5,000 SAR, and revenue increased by the same amount. Therefore, here cash is (debit) and revenue is (credit), and can be recorded in the journal as follows:

| Amount | Description | Transaction No. |

| 5,000 | Cash Account Dr. | 1 |

| 5,000 | To Revenue Account Cr. |

- Company (2) purchased a new building on credit for 300,000 SAR.

The result of this operation is as follows: Fixed assets (buildings) increased by 300,000 SAR, and the entity's liabilities increased by the same amount because the entity did not pay for the building. Therefore, here fixed assets are (debit) and the liability account is (credit,) and can be recorded in the journal as follows:

| Amount | Description | Transaction No. |

| 300,000 | Fixed Assets (Buildings) Dr. | 1 |

| 300,000 | To Liabilities Cr. |

- Company (3) sold a shipment of products on credit for 7,000 SAR.

The result of this operation is as follows: Revenue increased by 7,000 SAR and accounts receivable increased by the same amount. Therefore, here accounts receivable is (debit) and the revenue account is (credit) and can be recorded in the journal as follows:

| Amount | Description | Transaction No. |

| 7,000 | Accounts Receivable Dr. | 1 |

| 7,000 | To Revenue Cr. |

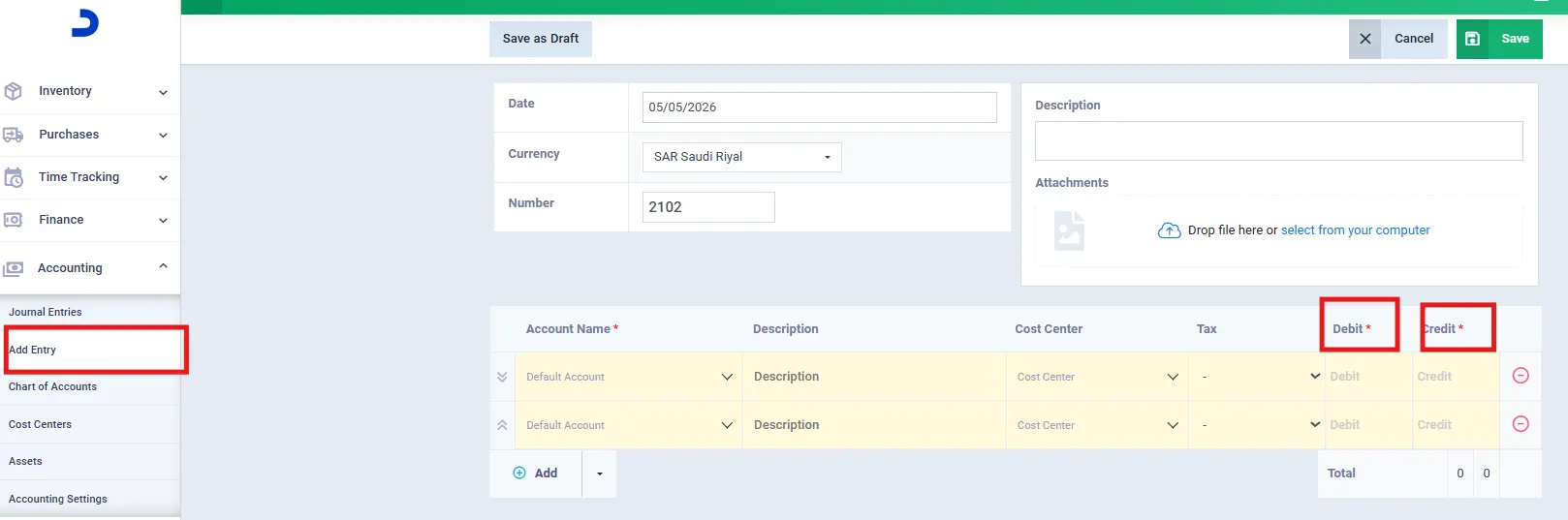

Debit and Credit Accounts in Daftra

When you perform any transaction in Daftra's accounting software, the entry is automatically created, which in turn transfers the transaction to the debtors or creditors account in the chart of accounts, without the need for any additional effort from you to record accounting entries or register them in the chart of accounts. By controlling both sides of your daily and ongoing accounting transactions, you can monitor your profits and losses and reach the maximum point of profitability you can achieve.

Frequently Asked Questions

Is the creditor the buyer?

No, the creditor is not the buyer but rather the seller who provides the goods or services in exchange for payment to the debtor, who is the buyer.

What are the three types of creditors?

Creditor types are classified into three categories: the ordinary creditor who carries no guarantee for debt recovery, the secured creditor who has a guarantee for debt recovery whether through mortgage or other guarantee, and the preferred creditor who has priority over other creditors in obtaining their debt from debtors.

What does credit interest mean?

Credit interest is the returns on investments or deposits that individuals leave with another entity.

When is revenue a credit?

Revenue is a credit when it increases the company's assets and reduces its liabilities.

What happens if you are indebted to creditors?

If you are indebted to creditors, this means you are required to pay a monetary amount to the crediting party, and payment must be made on time to avoid any legal procedures such as imprisonment or fines.

What are the types of credit interest?

Types of credit interest include loan interest, bond interest, and deposit interest.

Here we conclude that debits and credits and the difference between them are fundamentals that are indispensable in financial accounting. Therefore, it has become difficult for there to be a financial accountant who doesn't know the difference between them or makes errors in determining which accounts are debit and credit, to prevent any errors in recording journal entries through the general ledger and trial balance until reaching the balance sheet.