What are Provisions and Reserves, and the Difference Between Them

Table of contents:

- Key Summary

- What is a Provision?

- What is a Reserve?

- The Difference Between Provisions and Reserves

- What are the Reasons for Forming Provisions?

- What are the Reasons for Forming Reserves?

- What are the Characteristics of Provisions and Reserves?

- Is it Permissible to Combine Provisions?

- The Difference Between Provisions and Expenses

- How to Calculate Provisions?

- What are Closing Provisions?

- Calculating End-of-Service Benefits Provision

- What are the Journal Entries for Provisions and Reserves?

- What are the Types of Accounting Provisions?

- What are the Types of Reserves in Accounting?

- Managing Provisions and Reserves in Daftra Software

- Frequently Asked Questions

Did you know that companies, regardless of their profit size, are required to save money just like you? Yes, the accounting system mandates two types of money saving for institutions: provisions and reserves. Each type has its own nature and serves specific objectives.

In this interesting article, we explore the concept of both provisions and reserves, their types, clarify the differences between them, and discuss the reasons for establishing each.

What is a Provision?

The term provision in accounting (Provisions) refers to funds saved from company revenues to compensate for certain or probable expenses or losses. For example, fixed assets owned by the company, such as vehicles, decrease in efficiency over the years, consequently reducing production, which negatively affects the company's success.

Here, provisions play their role, where their funds are used to compensate for depreciated assets or obligations. Examples of provisions include: allowance for doubtful accounts, allowance for bad debts, accumulated depreciation, inventory obsolescence reserve, tax provisions, and end-of-service benefit provisions.

What is a Reserve?

The term reserve in accounting (Reserve) refers to funds deducted from company profits to maintain the company's financial stability, development work, and compensate for expenses or losses that are not likely to occur. For example, if a company wants to undertake expansions and increase production volume, it turns to profit reserves rather than revenues or capital.

Examples of reserves in accounting include: legal reserves, contingency reserves, government bond purchase reserves, capital reserves, and expansion and development reserves.

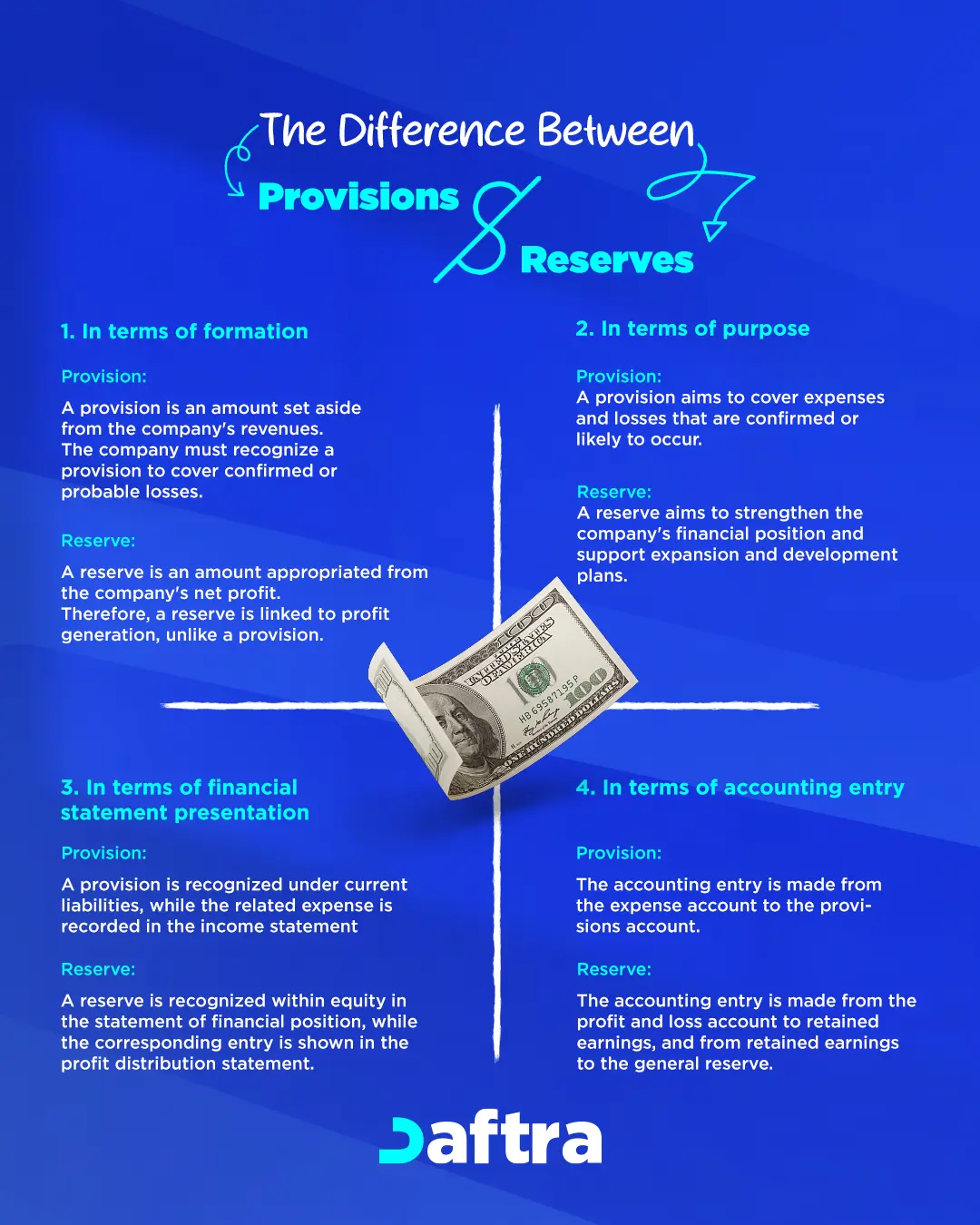

The Difference Between Provisions and Reserves

There are clear differences between provisions and reserves. Provisions are a burden on revenues, considered as a decrease in asset values or a new probable liability.

As for reserves, they are a portion allocated from the entity's profits to support its financial position and appear as an asset. While provisions are costs, reserves are linked to profits and will not appear in their absence. The most important differences between provisions and reserves are:

In Terms of Formation:

- Provision: Money is deducted for provisions from company revenues. Provisions must be established to compensate for certain or probable losses, whether the company achieves profits or not.

- Reserve: Money is deducted for reserves from the company's net profits, so reserves are linked to profit achievement, unlike provisions.

In Terms of Purpose:

- Provisions: Provisions aim to compensate for certain and probable expenses and losses, where these expenses are taken into consideration and compensated by provisions.

- Reserve: Reserves aim to strengthen the company's financial position, implement expansion policies and development plans, and face unexpected obstacles.

In Terms of Position on the Balance Sheet:

- Provision: Recorded under current liabilities, and the other side of the entry is recorded in the income statement because it's a burden on revenues.

- Reserve: Recorded under shareholders' equity on the balance sheet, and the other side of the entry is recorded in the profit distribution statement.

In Terms of Accounting Entry:

- Provision: From expense account to provisions account.

- Reserve: From profit and loss account to retained earnings account, and from retained earnings account to general reserve.

In Terms of Impact on the Project:

- Provisions: Provisions directly affect project operations because they meet actual necessary needs to complete the operational process. If the company cannot allocate part of its revenues as provisions, it won't be able to compensate for depreciated assets, thus directly affecting the operational process. Additionally, provisions are deducted from revenues.

- Reserve: Unlike provisions, reserves are not considered highly impactful on the operational process and project continuity, as reserves are primarily deducted from net profit after meeting primary needs, and are not considered expenses but rather distributions for investment purposes.

The differences between provisions and reserves can be summarized in several key points. In terms of formation, provisions are deducted from revenues whether profits are achieved or not, while reserves are deducted from net profits only. In terms of purpose, provisions are used to face probable losses, while reserves are for supporting the financial position.

On the balance sheet, provisions are listed under current liabilities, and reserves under shareholders' equity. In terms of accounting entries, provisions are recorded as expenses, while reserves are recorded from retained earnings. Finally, provisions directly affect operations, while reserves have an indirect impact as they are not considered operational costs.

What are the Reasons for Forming Provisions?

Accounting provisions are an important tool in the financial system of institutions, used to meet future obligations and potential losses that may affect a company's stability. There are several reasons that necessitate forming accounting provisions, the most important being:

Compensating for Fixed Asset Depreciation

Assets are certainly subject to depreciation over time, so fixed asset depreciation compensation provisions are a major type of provision.

Compensating for Bad Debts

For any reason, a company may not be able to collect its receivables from others. To cover any deficit that may arise from this, funds are allocated to compensate for bad debts or doubtful accounts.

Compensating for Investment Price Declines

Investment activities are in constant rise and fall, so provisions handle the task of compensating for this depletion.

Compensating for Inventory Value Decline

Inventory value is subject to a decrease, especially if it remains for a long period, and this loss is compensated through provisions.

Providing End-of-Service Benefits

Labor law guarantees, according to certain conditions, that employees receive end-of-service benefits from the company they work for. Accounting-wise, these benefits are provided through provisions.

Meeting Tax Obligations

Taxes are obligations known in advance by the company. To meet any related obligations, part of the money is reserved under provisions.

Legal Case and Compensation Obligations

Legal case obligation provisions are reserved to meet obligations arising from cases and lawsuits that may be filed against the company and the resulting procedures, such as losing the case and facing penalties.

The reasons for forming provisions include compensating for fixed asset depreciation, compensating for bad debts or doubtful accounts, compensating for investment price declines, compensating for inventory value decline, providing end-of-service benefits, meeting tax obligations, as well as legal cases and compensation obligations.

What are the Reasons for Forming Reserves?

Reserves are important elements in institutional financial management, where part of profits is allocated for several purposes aimed at protecting the company's financial entity and enhancing its ability to continue and grow. There are several reasons why part of profits is reserved as reserve funds, including:

Legal Compliance

Most legislative policies require joint-stock companies to provide a percentage of profits as reserves to maintain company capital in emergency cases, securing shareholders' rights.

Capital Preservation

One reason for establishing reserves is capital preservation, where part of the profits is reserved to cover any deficit that may occur for any reason in capital.

Strengthening Financial Position

To strengthen the company's financial position and enhance its ability to face any sudden obstacles, what is known as a general reserve is established, which is one of the most important reasons for establishing reserves in accounting.

Expansion and Development

As the name suggests, part of the profits is allocated for expansion and development work of any type.

Supporting National Investment

Government bonds purchased by private companies contribute to strengthening companies' financial position as well as advancing national investment, which is one of the reasons for establishing reserves in companies.

Meeting Emergencies

To enable the company to face any future emergency situations, contingency reserves are established to maintain proper operational process flow and avoid negative impact.

The reasons for forming reserves are summarized as legal compliance, capital preservation, strengthening financial position, expansion and development, supporting national investment, and meeting emergencies.

What are the Characteristics of Provisions and Reserves?

While provisions are considered a burden, reserves are part of profit distribution. Provisions appear as separate accounts with all positive indicators that drive the company to allocate provisions. Accordingly, each appears differently in financial statements. You find that period provisions appear as expenses in the income statement, and accumulated provisions exist as liabilities on the balance sheet. As for accumulated reserve balances, you find them under shareholders' equity on the balance sheet. Because they don't affect company profit, you find reserves under profit distribution in the statement of changes in equity.

To summarize the comparison between provision and reserve characteristics, you can refer to the following table:

| Comparison Aspect | Provision | Reserve |

| Nature | Considered a burden on revenues | Considered part of profit distribution |

| Appearance in Financial Statements | Appears as an expense in the income statement and as an accumulated provision as a liability on the balance sheet | Appears as an accumulated balance under shareholders' equity on the balance sheet |

| Impact on Profits | Directly affects net profit | Does not affect net profit, but appears in profit distribution |

| Position in Statement of Changes in Equity | Does not appear | Appears under profit distribution |

Is it Permissible to Combine Provisions?

Provisions can be combined in some cases, but this depends on the nature of the provisions and the accounting standards followed. In general, the decision about combining provisions should be based on the principle of providing accurate and useful information to financial statement users. There are some basic points to consider when combining provisions:

- Similarity in Nature or Purpose of Provisions: If provisions are similar in nature or purpose, it may be logical to combine them in one classification in the financial statements. For example, provisions related to different warranty costs may be merged into one category.

- No Impact on Transparency and Clarity of Financial Statements: It's important that financial statements remain transparent and accurate. If combining provisions leads to loss of clarity or misleads financial statement users, it should be avoided.

- Compliance with Adopted Accounting Standards: Adherence to applicable accounting standards is required, such as International Financial Reporting Standards (IFRS) or Generally Accepted Accounting Principles (GAAP). These standards determine how to classify and present provisions.

- Periodic Assessment of Provisions: Provisions should be assessed periodically to ensure they still accurately reflect the company's obligations. When combining provisions, this assessment should be comprehensive for all merged categories.

Several points must be considered when combining provisions: similarity in nature or purpose of provisions, no impact on transparency and clarity of financial statements, compliance with adopted accounting standards, and periodic assessment of provisions, including all merged categories.

The Difference Between Provisions and Expenses

In accounting and financial management, there is a clear difference between "provisions" and "expenses." A provision is an amount allocated from profits to cover an expected loss or future obligation. This loss or obligation must be probable and reasonably estimable. Expenses are costs consumed in the process of generating revenue, such as rent costs, employee wages, electricity costs, and marketing expenses. An expense is considered an operating cost that occurs during a specific accounting period.

How to Calculate Provisions?

Provisions can be calculated through various methods, and the method used differs according to the company's accounting policies and applicable accounting standards.

Ultimately, in all cases, these provisions should accurately reflect the company's estimates of debts it may not be able to collect, and should be reviewed regularly to ensure they reflect the current situation. The most common methods for calculating allowance for doubtful accounts include:

- Percentage Method (Percentage of Sales): A certain percentage of total credit sales is calculated as an allowance for doubtful accounts. This percentage is based on the company's historical experience and current conditions.

- Aging Method (or Accounts Receivable Analysis): Outstanding debts are classified according to their aging periods (such as 30 days, 60 days, 90 days, and over), then different percentages are applied to each aging category. It should be noted that the percentage increases as the non-collection period increases.

- Individual Method: This involves evaluating each customer's account individually and determining an allowance for each account based on estimating the probability of non-collection.

- Therefore, methods for calculating allowance for doubtful accounts include: the percentage method based on a percentage of credit sales, the aging method that classifies debts according to aging periods and applies varying percentages, and the individual method that relies on evaluating each account individually based on collection probability.

What are Closing Provisions?

Closing provisions are the process by which accounting records for a specific period are finalized, and necessary procedures are performed to prepare final financial statements for that period.

Closing provisions are an important part of the annual or monthly accounting cycle and aim to provide accurate and transparent accounting reports for the company, and provide final financial data that reflects the company's financial performance for a specific period, helping make future decisions and comply with adopted accounting standards.

The basic steps for closing provisions are as follows:

- Review and Correct Accounting Records: To ensure their accuracy and completeness, and verify that accounting entries have been applied correctly and all accounts have been reviewed.

- Close Income and Expense Accounts for the Provision Period: By transferring the balance of these accounts to the retained earnings account or profit and loss account.

- Estimate the Value of Potential Provisions: Such as provisions for uncollectible debts or provisions for marketable securities. This requires analyzing and estimating available information and applying adopted accounting standards.

- Prepare Final Financial Statements: Including retained earnings, profit and loss, balance sheet, and cash flows.

- Review Final Financial Statements: Review by financial auditors or approved external parties to verify the accuracy and reliability of financial information.

The steps for closing provisions include reviewing and correcting accounting records, closing income and expense accounts, estimating the value of potential provisions, preparing final financial statements, and reviewing these statements by approved parties to verify their accuracy and reliability.

Calculating End-of-Service Benefits Provision

End-of-service benefits provision is an amount allocated to cover the company's obligations toward employees upon termination of their service. The calculation method depends on local laws and company policies, and is usually calculated based on factors such as the employee's length of service with the company, salary, and sometimes the circumstances under which service ended (such as resignation, termination, retirement, etc.). For example, in some countries, the calculation may be based on the employee's average final salary multiplied by the number of years of service.

What are the Journal Entries for Provisions and Reserves?

Provision and reserve entries are fundamental accounting concepts that aim to ensure the accuracy of financial reports and reflect policies followed in dealing with potential losses and profit distribution. Below is an explanation of the nature of each entry and how to record it in accounting books.

Provision Entry

A provision creation entry is the entry through which the establishment of a provision to cover expected costs or losses is recorded. This entry usually includes recording an expense in the income statement and creating a liability on the balance sheet. For example, to create an allowance for doubtful accounts, the entry could be as follows:

Debit: Bad debt expense (appears in the income statement). Credit: Allowance for doubtful accounts (appears on the balance sheet as part of liabilities).

The provision entry appears as follows:

| Description | Debit | Credit |

| From A/c Asset Depreciation Expense | XXXXX | |

| To A/c Accumulated Depreciation Provision | XXXXX |

Reserve Entry

A reserve creation entry is the entry through which part of the company's net profits is allocated and transferred to a specific reserve account (such as a statutory reserve). This entry appears under shareholders' equity on the balance sheet, without affecting the income statement because it's not an expense but a profit distribution.

For example, when transferring part of profits to the statutory reserve, the entry could be as follows:

Debit: Income Summary (represents a reduction in distributable profits). Credit: Statutory Reserve (appears under shareholders' equity on the balance sheet).

The reserve entry appears as follows:

| Description | Debit | Credit |

| From A/c Income Summary | XXXXX | |

| To A/c Statutory Reserve | XXXXX |

Thus, it's clear that a provision entry is recorded by recognizing an expense in the income statement against a liability on the balance sheet, while a reserve entry is recorded by transferring part of net profits to a reserve account under shareholders' equity, without affecting the income statement.

What are the Types of Accounting Provisions?

Provisions in accounting are classified according to the nature of the purpose for which they are allocated, so there are two types of accounting provisions:

First: Asset-Related Provisions

Under this type fall provisions for compensating fixed asset depreciation, as well as provisions for compensating bad debts and doubtful accounts.

Second: Liability-Related Provisions

Under this type fall funds that may arise in tax transactions, as well as settling obligations that may arise from legal cases and their associated compensations, fees, and penalties.

Accounting provisions are divided into two types: asset-related provisions, such as fixed asset depreciation and bad or doubtful debts, and liability-related provisions, such as taxes, legal cases, and their associated compensations.

What are the Types of Reserves in Accounting?

Reserves have multiple types that differ according to their purpose and the procedures taken behind them. Below are the most prominent types of reserves used in accounting:

Legal Reserve

This is the percentage imposed by law on companies.

Statutory Reserve

This is what is determined by company owners according to the system they follow.

Capital Reserve

This is what is set aside from funds to face any deficit that may affect the company's capital.

General Reserve

This is the percentage that the company approves as a reserve to strengthen the financial position.

Expansion Reserve

This is the percentage for implementing expansion and development work in the company.

Government Bond Reserve

This is the money withheld to purchase government bonds offered by the state.

Contingency Reserve

This is the percentage specified to face unexpected future emergency situations.

Types of reserves in accounting include: legal reserve, statutory reserve, capital reserve, in addition to general reserve, expansion reserve, government bonds reserve, and contingency reserve, each of which is allocated for a specific purpose that supports the company's financial position.

Managing Provisions and Reserves in Daftra Software

By tracking assets and liabilities in Daftra's accounting software as well as the balance sheet and related reports, you can access clear and accurate information formats through which provisions and reserves are calculated.

Frequently Asked Questions

What are the negative aspects associated with using provisions and reserves?

Applying the principle of prudence and caution leads to the creation of provisions, as the need for an account that bears expected losses resulting from a specific procedure becomes apparent. The negative point of provisions is that they are an obligation on the company that should be paid periodically to prevent financial risks. Despite the importance of provisions, they affect the company's image and make owners or partners think more than once before joining and participating, as these provisions are taken from revenues.

Although reserves contribute to supporting every needed situation related to expansions or creating additional expenses, they are still elements that lead to ambiguity in the company's financial position, and no knowledge of the strength of performance. Reserves may also lead to poor management of available financing and revenues if not employed wisely.

How do provisions and reserves affect stakeholders?

Provisions and reserves negatively affect stakeholders because they take from their expected share to be received at the end of the period to serve other obligations or objectives.

Are there specific types of reserves?

Yes, there are several types of reserves:

- Legal reserve

- Statutory reserve

- General reserve

- Contingency reserve

- Government bond purchase reserve

- Price increase reserve

- Capital expansion reserve

Where do reserves appear on the balance sheet?

Reserves appear under the liabilities section on the balance sheet.

When is an allowance for doubtful accounts created?

An allowance for doubtful accounts is usually created when there is doubt about the company's ability to collect the full amounts due from customers, resulting from several factors:

- If the customer has a history of late payment or non-payment

- When the customer faces difficult financial circumstances that may affect their ability to pay

- The impact of general economic conditions, such as a recession, may affect customers' ability to pay

A long period has passed on the debt - the longer the non-collection period, the greater the likelihood of classifying it as a doubtful debt.

Are provisions debit or credit?

Provisions are classified as credit in accounting entries. When a company creates a provision, it means it debits the expense account and places the provision amount on the credit side as a liability on the balance sheet, reflecting that the company has a future obligation or expected loss that needs to be covered.

When should provisions be recognized in financial statements?

Based on International Accounting Standards (especially IFRS) and Generally Accepted Accounting Principles (GAAP), provisions should be recognized in financial statements in the following cases:

- Existence of a present obligation arising from past events

- It must be probable that settling this obligation will result in an outflow of funds or other resources from the company

- The amount of the obligation must be reliably estimable

If these conditions are not met, the provision is not recognized in the financial statements, but instead is referred to as a note or disclosure in the financial statements.

What is a claims provision?

It is a type of provision created to cover expected claims or debts that have not yet been settled. For example, in an insurance company, a claims provision may be created to cover expected compensation for claims that have not yet been settled. Claims provisions help provide a more accurate estimate of profits and losses for the accounting period, as potential future obligations are taken into account.

Is a provision a liability?

Yes, a provision in accounting is considered a type of liability. It represents an expected future obligation or potential loss resulting from past events, and is created when there is a present obligation that is likely to result in an outflow of funds or resources from the company.

What is a profit provision?

Profit provision refers to allocating part of the profits that the company decides for specific purposes instead of distributing them as dividends to shareholders. For example, the company may decide to allocate part of its profits to finance future investments, cover debts, or create a reserve fund.

Is a provision an asset?

A provision is not an asset and is considered a type of liability in accounting and financial management. Provisions are created to represent expected future obligations or potential losses. These provisions reduce net assets (assets minus liabilities) because they represent amounts the company expects to pay in the future; thus, they are classified as part of liabilities on the company's balance sheet.

What is a provision for price decline?

A provision for price decline is an amount allocated to cover the expected or actual decrease in asset values. This type of provision is commonly used, particularly for current assets such as inventory or investments. For example, if the market value of inventory is less than its purchase cost, the company may create a provision for price decline to reflect this decrease in its value in the accounting books.

What are fixed provisions?

Fixed provisions are amounts allocated regularly and consistently, often on an annual basis, to cover certain obligations. These provisions are usually related to expected and regular obligations, such as maintenance provisions or renewal provisions. Their purpose is to distribute the cost of these obligations equally over multiple periods to achieve stability in financial results.

What is the difference between provisions and reserves accounts?

A provision is a burden on revenues considered as a decrease in asset values or a new potential liability, deducted from revenues whether profits are achieved or not, and appears under current liabilities.

A reserve is a portion allocated from the entity's profits to support its financial position, appears only when profits exist, and is listed under shareholders' equity.

What is a provision whose purpose has been eliminated?

A provision whose purpose has been eliminated is a provision that was created for a specific purpose, and then the reason for its existence disappeared. In this case, this provision should be reviewed and confirmed that it is no longer needed, then it should be reprocessed accounting-wise in accordance with current obligations and the company's financial circumstances.

What is the nature of provisions accounts?

The nature of provisions accounts is credit accounts, recorded under current liabilities on the balance sheet, while the debit side in the accounting entry is recorded as an expense in the income statement, such as asset depreciation expense or bad debt expense.

What is the depreciation provision on the balance sheet?

It is a type of asset-related provision used to compensate for fixed asset depreciation. The purpose of the depreciation provision is to distribute the asset's cost over its useful life.

What is the difference between depreciation provision and accumulated depreciation?

Depreciation provision is the expense recorded periodically (monthly or annually) in the income statement to account for asset consumption during that period, while accumulated depreciation is an account appearing on the balance sheet showing the total accumulated depreciation on the asset since its purchase.

Where do provisions appear in the income statement?

They appear as expenses in the income statement, such as bad debt expense or asset depreciation expense.

What is a tax provision?

It is a type of provision withheld to meet tax obligations that are known in advance by the company.

When is a provision debit?

A provision is debited when used to record expected losses or obligations, such as doubtful debts or asset value declines.

Is a provision considered an expense?

Yes, a provision is considered an expense and is recorded in the income statement.

How is legal reserve calculated?

Legal reserve is usually calculated as a percentage of the company's net profits, often 5%. This amount is allocated to form a mandatory financial reserve deposited in a separate account and cannot be distributed to shareholders.

What is an expansion reserve?

It is a type of reserve allocated from profits for expansion and development work of any type.

What is a general reserve?

It is a percentage determined by the company as a reserve to strengthen the financial position.

In conclusion, we have covered in this article what provisions and reserves are, the difference between them, the types of each in accounting, the reasons for their formation, and also reviewed how Daftra software can help in calculating and identifying them.