Everything You Want to Know About Cost Accounting

Table of contents:

- What is Cost Accounting?

- What is the History of Cost Accounting?

- What are the Objectives of Cost Accounting?

- What are the Types of Cost Accounting?

- What are the Characteristics of Cost Accounting?

- What are the Types of Costs in Cost Accounting?

- What are the Methods of Calculating Costs?

- What are the Fields of Use for Cost Accounting?

- What is the Role of Cost Accounting in Determining Product Price?

- What is the Difference Between Cost Accounting and Financial Accounting?

- What are Cost Accounting Systems?

- What is the Role of a Cost Accountant in an Organization?

- What are the Main Challenges of Cost Accounting?

- What is the Role of Daftra Software in Cost Accounting?

- Frequently Asked Questions About Cost Accounting

How can companies control their costs while achieving desired profits? The answer simply lies in cost accounting. Its role in any institution cannot be neglected, because cost accounting serves as a pivotal tool in making decisions regarding the pricing of products and services, and determining whether production can be expanded, new markets opened, and more products launched. We also cannot overlook its role in financial oversight, accountability, and future planning for the institution.

Therefore, in this article, we present a comprehensive guide that explains cost accounting, its objectives, types, key elements, and methods for calculating and processing costs. All these details, along with more, can be found with detailed explanations that help you achieve your financial and commercial goals.

What is Cost Accounting?

Cost accounting is a branch of accounting that calculates, records, and classifies all direct and indirect costs associated with the production process. This includes calculating variable costs for each stage, as well as fixed costs.

For example, if you have a project like a coffee roastery, you can calculate its fixed costs, such as rent and electricity, and calculate variable costs, such as the price per ton of coffee. Through cost accounting, the institution records and studies the costs spent on any operation or product as they are part of different production stages. Through cost accounting, management can reduce and control company expenses, taking measures and making decisions to improve the institution's position.

What is the History of Cost Accounting?

The Industrial Revolution took place in the eighteenth century and led to the transformation of the manufacturing system from manual manufacturing to the machine system, resulting in the emergence of fixed and variable costs specific to production stages. Problems arose related to calculating fixed and variable costs during the production process, as well as determining the cost of machine operating hours and the cost of loading them onto production.

From here, the concept of cost accounting emerged and began to receive attention at the beginning of the twentieth century. Based on this, it became easy to determine the total costs of production, and therefore, the project owner can request the cost accountant to provide all costs incurred on the project, allowing them to accurately calculate the project's net profit.

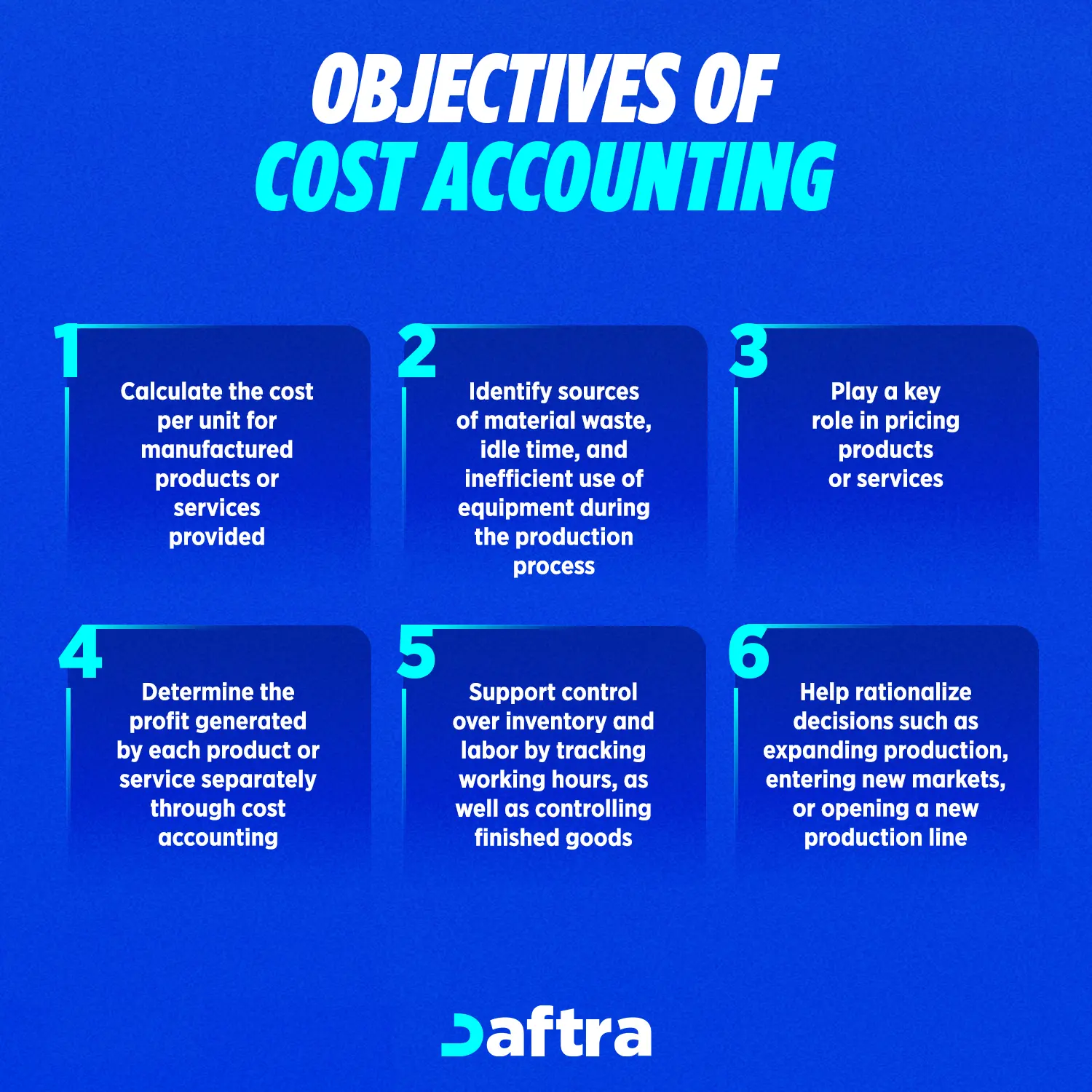

What are the Objectives of Cost Accounting?

As we agreed, cost accounting records and classifies expenses to determine the cost of a product or service, and also helps with management control purposes. The following is a detailed explanation of the objectives of cost accounting:

As we agreed, cost accounting records and classifies expenses to determine the cost of a product or service, and also helps with management control purposes. The following is a detailed explanation of the objectives of cost accounting:

1- Calculating the cost of units of products or services

Calculating the cost for each unit of manufactured products or services provided is one of the main objectives of cost accounting. After determining the unit cost, it can be easily priced.

This can be calculated, for example: If you have a company that produces several different products, you must first identify all products with their different types, then determine all cost elements, such as the costs of purchasing materials used in manufacturing the product, and also determine the labor costs that contributed to producing this product. After that, determine the variable and fixed costs and add them to each unit of manufactured products.

2- Monitoring Resource Allocation

Cost accounting works to monitor inventory and workers by determining work hours and also monitoring finished goods, which helps identify sources of material waste and time lost in equipment use or during the production process. This enables determining how to control this waste and improve operational efficiency, all of which helps reduce invested capital.

3- Accurately Identifying Profits

Through cost accounting, the profits of each product or service can be determined separately, enabling management to apply profit-maximization strategies.

4- Making Financial and Investment Decisions

One of the primary objectives of cost accounting is to analyze fixed and variable costs and understand their impact on financial performance, providing the necessary information for management to make informed decisions regarding product pricing, resource allocation, and budget preparation based on estimated costs.

5- Enhancing Investor and Financier Confidence

The accurate information available about cost accounting contributes to enhancing the confidence of investors, financiers, suppliers, and other stakeholders.

Cost accounting plays a vital role in attracting investments and supporting business relationships through reliable financial data that demonstrates the company's ability to manage its costs efficiently and rationalize expenses. It enables the maintenance of operational efficiency and the achievement of profits, making investors aware of costs and how to manage them. This, in turn, facilitates their understanding of the company's strategy and financial performance, allowing them to direct their investment decisions more effectively.

Use our free investment calculator to find out the return on different investments.

6- Review and Auditing

Cost accounting facilitates accounting review and auditing processes, identifies financial or accounting errors, and predicts potential risks at an early stage, to take necessary corrective measures that enhance financial management efficiency.

What are the Types of Cost Accounting?

There are four main types of cost accounting: standard cost accounting, activity-based cost accounting, marginal cost accounting, and lean accounting. Cost calculation must be considered according to legal accounting. The following are details of the types of cost accounting:

1- Standard Cost Accounting

This involves using standard costs rather than actual costs in order to determine and analyze the difference between the cost that would have occurred and the actual cost of production. Standard costs are used in factories to determine goods, and the difference between actual costs and standard costs is called "variance analysis."

Simple example: A factory expected standard costs of 5,000 Saudi Riyals, but the actual costs paid were 4,500 Saudi Riyals, resulting in a variance of 500 Riyals. In this case, it's clear that the variance is positive, and vice versa if the variance is negative. This is an indicator that encourages management to improve costs and reduce them.

2- Activity-Based Cost Accounting

Costs are determined for each activity separately, such as a product design activity or service distribution activity. From this, the most costly activities for the institution and those that use the most time can be identified. This helps improve the cost of each activity and avoid waste in both costs and time.

3- Marginal Cost Accounting

Costs in this case can be calculated based on variable costs only and charged to the product without allocating fixed costs and adding them to the product. Based on this, the contribution margin of the product can be calculated through the total revenue of this product minus the variable costs.

4- Lean Accounting

This is one of the cost accounting methods used to eliminate waste, whether in time or production materials. It relies on increasing profits and reducing waste.

You can rely on the "Daftra" system for calculating and tracking company expenses by classifying them and linking them to cost centers, and issuing detailed financial reports that clarify the company's financial position.

What are the Characteristics of Cost Accounting?

To create a strong and effective cost accounting system for cost estimation, it must possess key cost accounting characteristics that enable comprehensive analysis, serve various departments, monitor performance, and inform decision-making. Learn about the characteristics of cost accounting in the following points:

1/ Cost Analysis

Simplicity in presenting and analyzing costs. Cost accounts should be disclosed in an easily understandable way, so it's better to avoid complex and unnecessary details.

2/ Economic Efficiency

The cost accounting system should be characterized by economic efficiency so that it returns profits to the institution. The cost of operating the system should be within the financial capacity of the institution.

3/ Accuracy and Reliability

Accuracy in the data and information provided by the cost accounting system is crucial because this data is relied upon in the results used for decision-making.

4/ Completeness and Documentation

Comparison between internal applications and programs that distinguish the ideal cost accounting system. It should be capable of maintaining cost records for different periods so that costs can be compared over each period and another, which can be done by using one of the electronic accounting systems like the Daftra program. In addition to that, the cost accounting system should be characterized by reconciling results, in terms of reconciliation between cost accounts and the company's financial accounts.

5/ Speed

Speed is an essential element for the system's success, so that all information and data related to costs can be provided at any time. This can be achieved by accurately recording all costs incurred in a timely manner.

6/ Flexibility and Appropriateness

System flexibility is important so that it can adapt to all variables that occur. The system should be capable of handling more work and various changes. The cost accounting system should also be compatible with all the institution's work, as well as with the nature and size of each activity. It should be suitable for the accounting standards followed, whether they are international accounting standards or even Islamic accounting standards, and it should serve all the institution's objectives.

By applying all these characteristics to the institution's cost accounting system, a system capable of achieving the desired goals will be produced.

What are the Types of Costs in Cost Accounting?

Cost elements can be classified into eight main types, all of which aim to provide comprehensive and accurate information for making sound administrative decisions. Learn about the types of cost accounting in the following points:

1/ Direct Costs

From their name, we can define them as costs that are directly linked and related to producing the product, such as labor costs and materials used to manufacture the product. For example, a car manufacturing company can determine the direct costs of producing a car as the total cost of workers' wages and the cost of parts manufactured for the car only.

2/ Indirect Costs

These are costs that contribute to producing the product but are not direct, such as lighting and water costs, and these costs are used for the factory as a whole. Costs such as equipment maintenance and machine depreciation can fall under this category.

3/ Fixed Costs

These are costs that the institution spends whether production occurs or not, such as rent costs. The institution can pay rent periodically, and it is not linked to any production process. Also, loan interest payment is considered a fixed cost.

4/ Variable Costs

These are costs that change with the change in production volume, where the institution spends these costs with changes in activity volume and nature of work, such as product packaging costs. In this type of cost, the real and actual value of costs is calculated regardless of changes resulting from the passage of time or economic effects.

Therefore, costs change as a result of differences in work volume or something related to the company's activity and expansion, not because of differences in the timing of recording them, for example, and the natural increase resulting from inflation.

5/ Operating Costs

These are costs associated with daily operational activities, but are not indirect costs, such as rent and utilities. They are related to business operations and can be either fixed or variable costs.

6/ Sunk Costs

These are costs that the company cannot recover in the production process, meaning they do not return any profits to the company. They include fixed costs that cannot be avoided at the current time, or unnecessary variable costs. Sunk costs are not relied upon in making future business decisions because they do not affect financial results.

7/ Controllable Costs

These are costs that management can control, either by increasing or decreasing them, such as donations, bonuses, and advertisements. It is not preferable for these costs to equal zero in order to maximize profits, as they are indispensable in any institution.

8/ Opportunity Cost

If there is more than one opportunity and there is a possibility of gaining from one of these opportunities and losing the others, this is the opportunity cost. In other words, opportunity cost can be referred to as the profits or benefits that are lost from other alternative opportunities as a result of choosing one alternative.

With the "Daftra" accounting system, you can manage expense accounts of all types in your company. The system helps calculate taxes, track transactions, manage assets, and provides other advantages.

What are the Methods of Calculating Costs?

When calculating costs, we must calculate inventory costs as well as calculate expenses related to taxes according to the tax accounting system and the laws of your country, prepare financial reports, and also price products and determine profits.

Learn about the types and equations of cost accounting in the following points:

1/ Variable Costs

Here, attention is paid to calculating variable costs and charging them to the product, but the calculation of fixed costs on the product is overlooked, and they are charged to the income statement. The following is the accounting equation for calculating variable costs:

Number of units produced × Cost of materials used in production + Direct wages + Variable manufacturing costs = Variable cost calculation

This method is used to help management control variable costs.

2/ Total Costs

This method gives the lowest gross profit compared to other methods, and is calculated through the following accounting formula:

Total Costs = Direct Costs + Manufacturing Costs (whether fixed or variable)

3/ Direct Costs

Only direct costs related to production are calculated, and indirect costs are excluded and counted as general expenses. The accounting formula for calculating direct costs is as follows:

Direct Costs = Direct material costs + Wages and salaries costs + Direct manufacturing costs (variable and fixed)

4/ Utilized Costs

This is the calculation of any cost that was used to produce products, meaning all variable costs are calculated in addition to only the utilized fixed costs, because there is a portion of fixed costs that is not utilized. Utilized costs are considered one of the most widespread methods for calculating different production costs and then determining the unit cost of the product. Utilized costs can be determined through the following accounting formula:

Utilized Costs = Total Fixed Costs × Actual Capacity ÷ Available Capacity

What are the Fields of Use for Cost Accounting?

Cost accounting is used in many fields and industries with the aim of improving efficiency and maximizing profit through accurate cost analysis, and then making sound financial decisions that enhance the sustainability and success of institutions regardless of their activities and fields of work. The following are the most prominent fields of use for cost accounting:

1- Manufacturing and Services Field

Cost accounting is used in the industrial business sector to determine production costs, analyze operational efficiency, monitor the distribution of financial and human resources, and evaluate profits for each product. In addition to that, it is used in the service sector to estimate the costs of providing services and analyze and evaluate financial performance, such as healthcare costs, related treatment expenses, and other medical services. Cost accounting is used in many other fields, such as educational services, legal consulting services, and others.

2- Retail

Cost accounting is used in the retail field to determine inventory costs, estimate costs associated with product distribution, and analyze profit margins compared to the cost of goods sold.

3- Construction and Contracting

Cost accounting helps track costs associated with materials, labor, and equipment in the contracting field and construction and architectural projects, contributing to managing budgets and allocating resources effectively.

4- Agricultural Sector

Cost accounting is used in the agricultural sector for planning and estimating agricultural production costs, and determining appropriate strategies to improve return on agricultural investment.

5- Non-Profit Organizations

Cost accounting is used in non-profit organizations to determine costs associated with each program or project, understand the financial resources required to achieve the social goals of these organizations, and then analyze costs and evaluate the efficiency of programs and services that achieve desired results at the lowest cost.

Then, necessary decisions are made regarding modifications to the budget or programs, which contribute to improving the organization's overall performance and better resource allocation. Cost accounting is also used to provide accurate data to donors or funders about how financial resources are distributed, which enhances the organization's transparency and credibility.

What is the Role of Cost Accounting in Determining Product Price?

Cost accounting clarifies the necessary information to understand costs associated with producing goods, and then enables the accurate determination of product price. The following are the steps that illustrate the role of cost accounting in determining product price:

- Determining direct costs used in producing the product, such as raw materials and labor wages, makes it easier to calculate the total cost of the product.

- Determining indirect costs such as rent, utilities, and administrative salaries, and understanding how to distribute these costs across different products and services, thus enabling estimation of the actual cost of each product.

- Calculating the profit margin for each product by comparing the expected selling price with total costs, which contributes to determining the appropriate price to achieve the planned profit.

- Cost accounting provides the necessary information that helps companies apply proactive dynamic pricing strategies to determine whether prices need to be adjusted based on actual costs, market and economic conditions, and variables, as well as price differences resulting from comparisons with competitors.

What is the Difference Between Cost Accounting and Financial Accounting?

The difference between cost accounting and financial accounting lies in the objective and target audience. Learn about the most prominent differences between cost accounting and financial accounting in the following points:

1/ Beneficiaries

The beneficiaries of cost accounting are internal parties - management, which are the same parties concerned with management accounting, while the beneficiaries of financial accounting are external parties such as investors, banks, and suppliers.

2/ Objective

The objective of financial accounting is to determine an institution's activities and budget, while cost accounting is used to determine production costs.

3/ Nature of Available Data

Financial accounting data is aggregated and not detailed like cost accounting.

4/ Method of Use

Cost accounting is used for making management-related decisions, while financial accounting helps in making investment and credit decisions.

What are Cost Accounting Systems?

Types of cost accounting systems are the methods used to allocate and estimate costs in the budget. The most prominent cost accounting systems are as follows:

1/ Job Order Cost System

Used to track costs specific to customized products, or goods and services that are produced or provided on demand, where costs are allocated to each job order or project separately, including direct costs and indirect costs. Through this system, detailed reports are generated for each job order, enabling accurate evaluation of profitability for each project or customized product.

2/ Process Cost System

Used in companies that produce large quantities of standard products, such as food factories or car manufacturing companies, where costs are aggregated at the operations or department level, and costs are distributed across all units produced during a specific time period, instead of individual orders (unlike the job order system). This results in obtaining reports specific to total production costs for each operation.

In general, cost accounting systems are used at the internal management level, unlike financial accounting, with the aim of managing and calculating costs in ways that suit the nature of production, which ultimately leads to making sound decisions related to managing operations smoothly and improving their efficiency, and increasing profits through accurate product pricing, affecting the company's success and growth.

What is the Role of a Cost Accountant in an Organization?

The cost accountant is responsible for a precise and sensitive task, so they must be chosen carefully to ensure their suitability for the assigned role. We must consider their personal integrity and distance from using manipulation methods that fall under creative accounting, as we look for technical proficiency. We can define the job description and tasks of a cost accountant in several ways:

- They are responsible for all analyses and reports related to costs.

- Preparing detailed budget reports for each activity.

- Setting cost expectations for each activity, whether annual or monthly.

- Determining all costs, whether fixed or variable.

- Assisting in creating cost reports that are added to the financial position.

- Recommending solutions and decisions to the board of directors to improve the activity specifically and the institution in general.

What are the Main Challenges of Cost Accounting?

Despite the benefits and advantages of cost accounting, when practicing its functions and related tasks, several challenges can be faced that must be well understood to know how to deal with them with effective strategies to improve the accuracy and efficiency of results from cost accounting. The following are the most prominent of these challenges:

- Collecting cost data requires significant time and effort.

- Difficulty in correctly classifying costs, especially fixed and variable costs, affects the accuracy of financial analysis.

- Inaccuracy of cost estimation assumptions.

- The complexity of production processes and stages leads to difficulty in accurately tracking costs for each product, project, or production stage.

- Market changes and intense competition affect the accuracy of cost estimates.

- Lack of integration between cost accounting systems and other institutional management systems may lead to problems in collecting and analyzing cost-related data.

Instead of facing challenges and obstacles that drain time and effort, you can simply use Daftra accounting software to collect data, estimate costs, and accurately track cost accounts.

What is the Role of Daftra Software in Cost Accounting?

In the Daftra accounting program, to calculate costs related to a specific production unit, the concept of cost centers is employed, where costs associated with a particular project, department, or branch are allocated to this center. You can create multiple cost centers in Daftra to control accounts related to these centers and audit the differentiation of profit and loss sources in your company.

Frequently Asked Questions About Cost Accounting

What is the need for cost accounting?

Every institution needs cost accounting to know the costs of production and manufacturing stages, to help management in controlling inventory and company expenses, and to assist in making decisions specific to the institution.

What are cost accounting reports?

Cost accounting reports are reports that help analyze company costs accurately, with the aim of improving financial performance. The most prominent reports of cost accounting are:

- Cost Center Report: Displays details related to indirect revenues and expenses associated with different cost centers, and helps understand how costs are distributed across various centers, enabling management to identify the most efficient cost centers or those that need improvement.

- Distribution Report: Provides comprehensive information about general expenses and expenses allocated to each cost center based on specified distribution rules, whether for indirect or variable costs. Its purpose is to make necessary decisions to rationalize costs while maintaining production quality.

- Cost Accounting Summary Report: Provides summarized information about direct and indirect costs.

- Its purpose is to evaluate financial performance and make decisions related to cost and production.

- Comparative Budget Report with Cost Accounting: Its main purpose is to compare the approved budget and actual costs, making it easier to identify deviations from the estimated budget, analyze the reasons for these differences, and enable management to make corrective decisions.

- Cost Reconciliation Report: Contributes to understanding the differences between estimated costs in cost accounting and actual costs in financial accounting that appear in income statements, balance sheets, and cash flow statements. This helps in accurate analysis of differences between expected and actual costs, and making decisions based on accurate data to enhance business efficiency and support future financial planning.

What is the most common method in cost accounting in industrial companies?

Activity-Based Costing (ABC) is the most common method in cost accounting in industrial companies, because it focuses on analyzing costs associated with activities that consume resources, and then determining the cost of each activity separately, such as production, distribution, and storage. After determining activity costs, these costs are distributed to products based on how much each product consumes these activities, which enables internal management to understand cost factors more accurately and determine prices based on these analyses.

What are the advantages of cost accounting?

It helps management improve profits and reduce costs, and through it, production methods can be changed and improved. It also helps reduce losses and waste, and contributes to determining product price.

What is a cost record?

It is a record where all information related to costs is entered, and the total costs of the product are placed in it. And it is done monthly or quarterly.

What are the advantages of the cost accountant job position?

This position is considered one of the most important jobs in any institution because high-level financial and administrative decisions depend on it to a large extent. The most prominent advantages of the cost accountant job position are:

- Increased demand for the cost accountant position, and therefore a sense of job stability, as the cost accountant works in many fields and projects.

- Possibility of career advancement to higher positions such as manager or financial advisor.

- Working as a cost accountant gives the job holder more analytical skills necessary to understand costs and analyze financial performance.

- High salary for cost accountants.

What is the difference between construction company accounting and cost accounting?

Construction accounting is part of cost accounting, but cost accounting focuses on analyzing costs in general, while construction accounting focuses on managing costs and revenues related to construction projects, building services, and technical maintenance work related to this type of project.

Are cost principles used in government accounting?

Yes, cost accounting is used in government accounting, but the same principles are directed to calculate government costs and revenues instead of company profits and expenses, taking into consideration the different nature of government accounting and the different handling of public revenues and expenditures, and the absence of material return in many cases despite injecting many costs, such as building government schools or hospitals, and providing services to the community.

What are cost accounting constraints?

Cost accounting constraints are the process of recording and documenting expenses for the ability to track them, with the aim of providing complete and accurate information about the company's financial position for the ability to make informed administrative decisions.

What are the modern methods of calculating costs?

Modern methods of calculating costs either calculate costs based on activity, target costing method, quality-based costing, or environmental costing.

What are the most important cost accounting equations?

There are 3 of the most important cost accounting equations that you should know:

Prime Cost = Direct Materials + Direct Labor + Direct Expenses

Conversion Cost = Direct Labor + Indirect Manufacturing Costs

Product Cost (Manufacturing) = Direct Materials + Direct Labor + Indirect Manufacturing Costs

What are the disadvantages of cost accounting?

The disadvantages of cost accounting lie in the difficulty of accurately classifying all expenses paid, and it requires hiring specialized experts in financial data analysis to be able to identify errors and make appropriate estimates.

What is the difference between management accounting and cost accounting?

The difference between management accounting and cost accounting lies in the target audience, objective, and type of reports prepared.

Management accounting provides management with the most important financial and non-financial information related to improvement and development decisions in the company, while cost accounting focuses on determining and analyzing all expenses spent inside and outside the company.

What is the overhead rate in cost accounting?

The overhead rate in cost accounting is a percentage calculated by dividing total indirect costs by direct costs.

The purpose of calculating the overhead rate is to distribute indirect costs to the products or services provided.

The formula used in calculating the overhead rate in cost accounting is:

Overhead Rate in Cost Accounting = Indirect Cost ÷ Direct Cost

What are the stages of development of cost accounting?

The stages of development of cost accounting begin with the professional stage, which aims to track production costs and determine product prices. Then comes the academic stage, which aims to develop accounting tools in cost analysis. This is followed by the information systems stage, which includes modern systems that have facilitated transaction recording processes and access to more accurate results.

What are the reasons for the emergence of cost accounting?

The reasons for the emergence of cost accounting lie in the rapid developments in various industries and trades that made cost accounting of utmost importance for tracking and analyzing expenses comprehensively and accurately, which results in many decisions, the most important of which is pricing products.

How does management accounting depend on cost accounting?

Management accounting depends on cost accounting in providing the necessary data and information for making decisions related to planning within the organization and analyzing and evaluating the current status of the company.

Is cost accounting better than financial accounting?

No, cost accounting is not better than financial accounting. You should know that both are important and essential in serving the company's objectives, and neither type can be dispensed with.

What is cost accounting in hotels?

Cost accounting in hotels relates to recording financial transactions, analyzing reports, summarizing payments, and determining the cost of each department within the hotel. This results in making important financial and administrative decisions.