How to Calculate Break-Even Point, Its Objectives, and Importance

Table of contents:

- Key Summary

- What is the Break-Even Point?

- What is the Importance of Calculating the Break-Even Point?

- What are the Use Cases of Break-Even Point in Business?

- What is the Break-Even Point Formula?

- What are the Factors that Lead to an Increased Break-Even Point?

- What are the Benefits of Calculating Break-Even Point?

- What is the Objective of Achieving the Break-Even Point?

- How Can I Comment on Break-Even Point in Accounting?

- What is the Break-Even Equation?

- What is the Relationship Between Selling Price and Break-Even Point?

- How Do I Calculate Break-Even Point for a Single Product?

- How is Break-Even Point Calculated for Multiple Products?

- Solved Examples on Break-Even Point

- When Does a Project Start Generating Profits After Break-Even Analysis?

- How Does Daftra Help You Calculate Break-Even Point?

- Frequently Asked Questions

Can profit or loss be achieved, or neither? Every business seeks to achieve significant profits from sales of products or services it offers to its audience. This is achieved when total revenue exceeds the costs and expenses incurred by the business. Loss occurs when expenses exceed revenue generated during a specific period.

However, there is a completely different situation involving profit and loss, known as the break-even point, where neither profit nor loss occurs. This is the point of cost equilibrium, where total costs equal total revenue.

In this blog, we will learn in detail about the break-even point and how to calculate it.

What is the Break-Even Point?

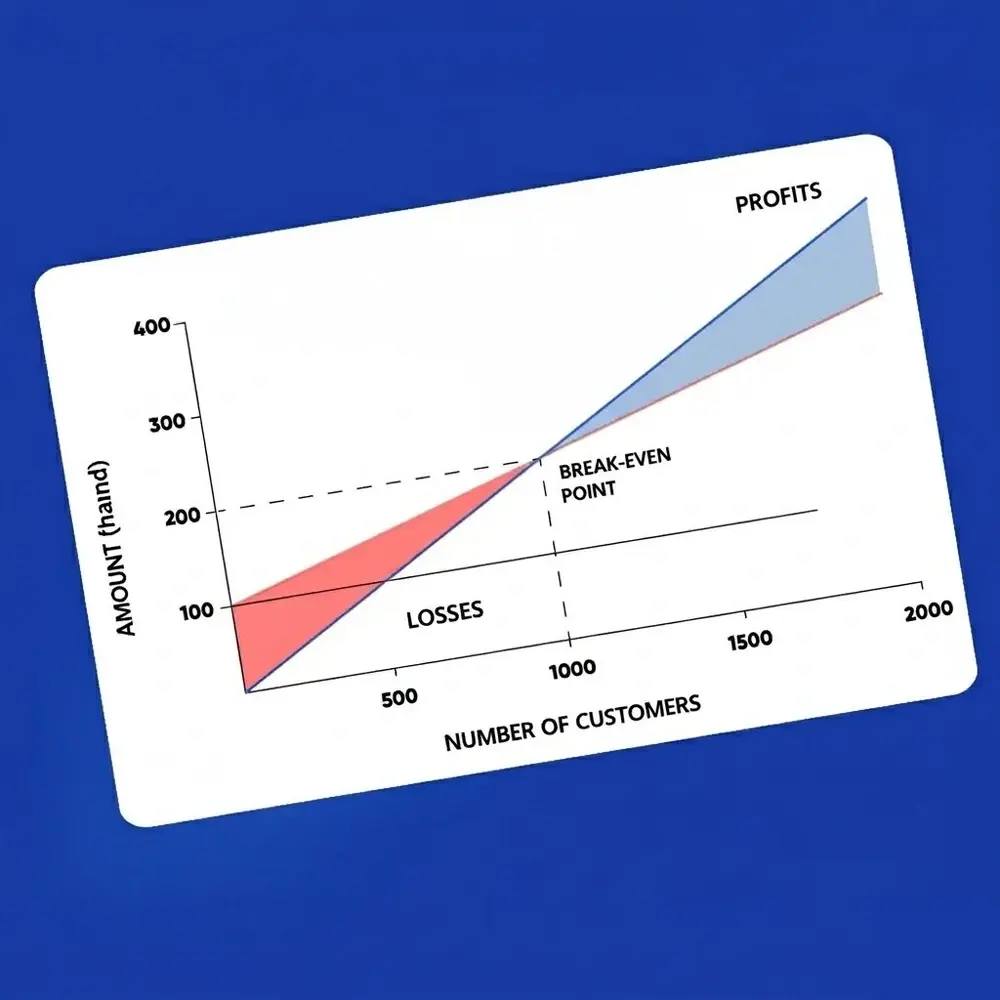

The break-even point is the intersection between the revenue curve and the total expense curve, where total revenue equals total expenses, whether fixed or variable costs. In other words, it is the point where the company achieves neither profit nor loss.

Beyond the break-even point is considered profit, and what precedes it is considered loss. Therefore, your company can determine the total units it needs to produce to start generating profit.

The expense curve is the sum of two curves: the fixed costs curve and the variable costs curve. Fixed costs are expenses incurred regardless of production volume, whether the company produced five units or did not produce at all, such as rent and salaries.

Variable costs are any expenses that increase or decrease according to the number of units. If production volume increases, variable costs rise, and if production volume decreases, variable costs decrease. These include all direct costs related to the activity.

Illustrative Example of Break-Even Point:

If fixed costs during March equal 4,000 SAR, and the variable cost per unit is 50 SAR.

Revenue equals 9,000 SAR because 100 units were produced.

Therefore, total variable costs for one hundred units equal 5,000 SAR, and fixed costs equal 4,000 SAR.

Thus, total costs equal 9,000 SAR and equal revenue.

Consequently, break-even sales value is achieved when 100 units are produced.

What is the Importance of Calculating the Break-Even Point?

Break-even point is a financial tool used to ensure that the selling price covers the incurred costs. Therefore, any business must calculate the break-even point due to its numerous interests and benefits, which can be clarified in the following points:

- Cost Determination: Through calculating the break-even point, fixed and variable costs can be determined, as well as the extent of impact that increases and decreases have on business profits.

- Production Volume Determination: It helps the business determine the production volume necessary to achieve profit or avoid loss by calculating fixed and variable costs, making it easy to know the sales required to achieve expected profit.

- Forecasting: Future losses that will be realized at a specific production volume can be known.

- Decision Making: Calculating the break-even point helps management make decisions regarding adding new products or discontinuing a product that brings a loss to the business.

- Pricing Strategy Support: It supports the company in its product pricing plans, as any increase in selling price leads to needing to sell fewer products.

What are the Use Cases of Break-Even Point in Business?

There are situations where break-even points must be used to determine sales levels, pricing plans, project evaluation, and other desired objectives. Learn about the use cases of break-even analysis equations:

- Need to Start New Activity: Break-even point calculation can be considered part of the feasibility study for establishing a new company or starting a new activity within an existing company.

- Pricing Adjustment: Your company may want to reduce the price of a specific product to increase its competitive opportunities, relying on reducing fixed and variable costs.

- Making Critical Company Decisions: Every administrative decision that may affect company revenue should be preceded by a break-even point calculation to understand how it will be affected by the decision to be implemented.

What is the Break-Even Point Formula?

Using the break-even point formula is important in evaluating projects and production lines, and it also plays a role in budgeting and forecasting near-term losses or gains. Use the following accounting equation to obtain the break-even point:

Break-Even Point = Fixed Costs / (Unit Selling Price - Variable Cost per Unit)

What are the Factors that Lead to an Increased Break-Even Point?

The closer the break-even point is to the origin on the graph, the easier it appears to achieve. Factors affecting the increase in break-even point:

- Fixed Cost Stability: When fixed costs are low, the break-even point becomes achievable from the project's beginning. This indicates the importance of reducing fixed costs as much as possible.

- Increased Variable Costs: Increasing variable costs per unit leads to a higher break-even point and the need for more time to reach it.

- Increased Units or Elements: The need to produce a larger number of units leads to increased variable production costs, affecting the break-even point and increasing its value.

- Stability of Conditions: Unexpected equipment maintenance leads to significant cost increases, which is reflected in an increased break-even point.

What are the Benefits of Calculating Break-Even Point?

The purpose of calculating break-even points is to establish pricing plans, budget plans, operational plans, and other key plans that contribute to maintaining business continuity and achieving positive profit. Learn about the benefits of calculating the break-even point at both the administrative and financial levels:

- Determining the production and sales volume required to start generating profit and exit the loss phase.

- Exploring opportunities through which fixed and variable expenses can be reduced to achieve break-even points faster.

- Regular business monitoring and identifying important milestones that separate the company from achieving the required production volume to reach the break-even point.

What is the Objective of Achieving the Break-Even Point?

The objective of achieving the break-even point is cost analysis and profitability improvement, which results in maintaining your company's financial safety level. When calculating the break-even point, it tells us several things; learn about them in the following points:

- Determining Required Production Units: The number of units produced that must be sold to cover fixed costs and variable costs.

- Determining Safety and Financial Stability Level: The break-even point is considered an important measure of the margin of safety.

- Decision Making: Management can use break-even points in important decisions, such as reducing unnecessary costs and production needed to achieve profit.

- Product Pricing: Knowing the appropriate price for the unit that was produced.

- Wage Determination: It helps determine employee wages by knowing fixed costs and how to deal with them.

How Can I Comment on Break-Even Point in Accounting?

Commenting on break-even points in accounting requires understanding fixed and variable costs and sales revenue to be able to make various decisions. Here are some observations that help you comment and analyze break-even point results through:

- Safety Indicator: Break-even point gives an idea about how "safe" the project is in facing market fluctuations.

- Absence of Profit and Loss: Reaching the break-even point does not mean achieving profit, but only means that the project is no longer incurring losses.

- Impact of Changes in Costs and Prices: You must monitor how changes in fixed and variable costs and selling prices can affect the break-even point.

What is the Break-Even Equation?

It is an accounting method used to calculate the break-even point in business, which is the point where total revenue equals total costs, meaning the company achieves neither profit nor loss. The basic equation for calculating cost coverage is:

Total Revenue = Fixed Costs + Variable Costs

This equation can be detailed as follows:

- Selling Price per Unit × Number of Units Sold = Fixed Costs + (Variable Cost per Unit × Number of Units Sold)

- To finally become the Break-Even Point in Units = Fixed Costs / (Selling Price per Unit - Variable Cost per Unit)

What is the Relationship Between Selling Price and Break-Even Point?

With other factors remaining constant, the unit selling price directly affects the break-even point. If the unit selling price increases, the break-even point is achieved by selling fewer units, because each unit sold contributes a larger amount to covering fixed costs. Conversely, if the selling price decreases, the company needs to sell more units to cover fixed costs.

- A higher selling price affects selling fewer units to achieve the break-even point, as it covers fixed costs.

- Lower selling price affects increasing the number of units produced to cover fixed costs.

How Do I Calculate Break-Even Point for a Single Product?

There are two approaches to calculating the break-even point: either calculating the break-even point for a single product or for multiple products. Here we will learn how to calculate the break-even point for a single product only using three methods, as follows:

1- Trial and Error Method for Calculating Break-Even Point for a Single Product

The first method for calculating break-even points is the trial-and-error method. You have three types of numerical data:

- Number of units (sales volume)

- Revenue achieved

- Total cost

Through experimentation, the value where both sides are equal is determined; cost and sales in a way that achieves neither profit nor loss.

Using Daftra's sales management software helps you provide the necessary revenue data for calculating break-even points with other required accounts in equations due to the interconnection of programs in their systems.

2- Graphical Method for Calculating Break-Even Point for a Single Product

The second method, which is the most widespread, is the graphical method for calculating cost coverage. This is done through basic steps:

- Determine fixed costs

- Determine variable cost per unit

- Determine the selling price per unit

- Place the number of units on the horizontal axis of the graph, and place costs and sales on the vertical axis.

- Express fixed costs with a line parallel to the horizontal axis that intersects with the vertical axis at the point representing fixed cost.

- Calculate the variable cost for one unit and two units

- Place a point representing the cost of one unit and the cost of two units

- Draw a straight line starting from the origin and passing through the two specified points

- The fixed cost curve intersects with the variable cost curve

- Add the two curves together to form one curve representing the total cost

- Determine the selling price for one unit and calculate the selling price for two units. Place the two points on the graph

- Draw a straight line from the origin passing through the two points and intersecting the total cost curve

- The intersection point of the total cost curve with the sales curve is the required break-even point

3- Mathematical (Algebraic) Method for Calculating Break-Even Point for a Single Product

The third method is the mathematical method, using a fixed equation to calculate the break-even point for a single product as follows:

Break-Even Point = Fixed Costs / (Unit Selling Price - Variable Cost per Unit)

(Unit Selling Price - Variable Cost per Unit) is the contribution margin per unit.

Note that the break-even point to be calculated represents the number of units that must be produced and sold to start generating profits.

The contribution margin achieved when producing one unit is the selling price of this unit minus the variable cost of this unit.

Illustrative Example:

If fixed costs for project (A) equal 50,000 SAR, and variable costs per unit equal 100 SAR...

And the selling price for this unit equals 300 SAR.

Required: Calculate the break-even point below which production volume should not fall to achieve profits.

First, calculate the contribution margin per unit = Unit selling price - Variable cost per unit.

Contribution margin = 300 - 100 = 200 SAR

Break-Even Point = Fixed Costs / Contribution Margin

Break-Even Point = 50,000 / 200 = 250 units

Therefore, the number of units below which production volume should not fall is 250 units, from which profit generation begins.

Another Example:

Project (B) had variable costs for producing one unit as follows:

Raw material costs: 40 SAR Product packaging costs: 8 SAR Shipping fee costs: 22 SAR Other direct costs: 30 SAR Fixed costs equaled 80,000 SAR.

Unit selling price equals 200 SAR for the product.

Required: Calculate the break-even point from which profit generation begins.

First, calculate variable costs per unit = Raw materials + Product packaging + Shipping fees + Direct costs.

Variable costs per unit = 40 + 8 + 22 + 30 = 100 SAR

Therefore, the variable cost for producing one unit equals 100 SAR.

Second: Contribution margin can be calculated as follows

Contribution margin = Unit selling price - Variable cost per unit

Contribution margin = 200 - 100 = 100 SAR

Third: Calculate the break-even point

Break-Even Point = Fixed Costs / Contribution Margin

Break-Even Point = 80,000 / 100 = 800 units

Therefore, the business must produce 800 units to start generating profits.

How is Break-Even Point Calculated for Multiple Products?

If the business produces several different products and not just one product, there are several steps that must be followed to determine the break-even point for each product separately.

The first step that should be implemented to determine the break-even point in the case of multiple products is to determine the sales mix ratio:

1- Determine the sales mix ratio for each product, which is the expected ratio for the product to achieve profits. It can be determined through the following equation:

Sales Mix Ratio = Expected Sales for Product / Total Expected Sales for Products

First: Calculate the average selling price for the sales mix: Average selling price for sales mix = Product selling price × Sales mix ratio

To understand sales mix, it is the ratio that the company targets to achieve its sales from a specific product. For example, if the company produces three products. Based on its market study, it finds that the first product has greater sales opportunities. So the company makes its sales mix 50% of total revenue.

While the other two products each have a sales mix of 25%, suppose the total target revenue is 100,000 Saudi Riyals. Based on the established sales mix, the target revenue for the first product becomes 50,000 Saudi Riyals. At the same time, the target revenue for the second and third products is 25,000 Saudi Riyals.

Second: Calculate average variable cost for sales mix: = Variable cost per unit × Sales mix ratio

Third: Calculate average contribution margin for sales mix: Average selling price for sales mix - Average variable cost for sales mix

Fourth: Calculate break-even volume for sales mix: Fixed Costs ÷ Average contribution margin for sales mix

Illustrative Example:

Business (M) produces three products, which are (A), (B), and (C), and this table shows data related to them:

| Product | Unit Selling Price | Variable Cost per Unit | Sales Mix Ratio |

| A | 50 SAR | 10 SAR | 50% |

| B | 100 SAR | 20 SAR | 30% |

| C | 150 SAR | 50 SAR | 20% |

| Fixed costs reached | 200,000 SAR for all products |

Required: Determine break-even volume for the three products.

First: Calculate the average selling price for the sales mix: = Product selling price × Sales mix ratio

| Product | Unit Selling Price | Sales Mix | Average Selling Price |

| A | 50 SAR | 50% | 25 SAR |

| B | 100 SAR | 30% | 30 SAR |

| C | 150 SAR | 20% | 30 SAR |

| Average selling price for sales mix | 85 SAR |

Second: Calculate the average variable cost for the sales mix: = Variable cost per unit × Sales mix ratio

| Product | Variable Cost per Unit | Sales Mix Ratio | Average Variable Cost |

| A | 10 SAR | 50% | 5 SAR |

| B | 20 SAR | 30% | 6 SAR |

| C | 50 SAR | 20% | 10 SAR |

| Average variable cost for sales mix | 21 SAR |

Third: Calculate average contribution margin for sales mix: Average selling price for sales mix - Average variable cost for sales mix = 85 - 21 = 64 SAR

Fourth: Calculate break-even volume for sales mix: Fixed Costs ÷ Average contribution margin for sales mix = 200,000 ÷ 64 = 3,125 units

If calculating break-even volume for each product separately is required, we perform this step:

Break-even volume for each product = Break-even volume for sales mix × Sales mix ratio

Break-even volume for product (A) = 3,125 × 50% = 1,562 units Break-even volume for product (B) = 3,125 × 30% = 937 units Break-even volume for product (C) = 3,125 × 20% = 625 units

Solved Examples on Break-Even Point

1- If a business produces only one product, and the variable cost of producing one unit of this product equals 50 SAR.

The business incurs these costs monthly:

Salaries 10,000 SAR Tax expenses 5,000 SAR Rent 5,000 SAR Equipment depreciation expense 2,000 SAR Insurance expense 3,000 SAR Loan interest 5,000 SAR Production volume equals 5,000 units, where revenue reached one million SAR.

Required: When is break-even achieved?

First: Calculate unit selling price = Total revenue ÷ Number of units produced.d = 1,000,000 ÷ 5,000 = 200 SAR

Second: Calculate contribution margin = Unit selling price - Variable cost per unit = 200 - 50 = 150 SAR

Third: Calculate total fixed costs = Salaries + Tax expenses + Rent + Equipment depreciation expense + Insurance expense + Loan interest = 10,000 + 5,000 + 5,000 + 2,000 + 3,000 + 5,000 = 30,000 SAR

Therefore, break-even volume = Fixed costs ÷ Contribution margin = 30,000 ÷ 150 = 200 units

Consequently, any increase in the number of units above 200 units will achieve significant profits for the business.

2- There is a business that produces two products, and this data relates to them:

| Product | Unit Selling Price | Variable Cost per Unit | Sales Mix Ratio |

| A | 40 SAR | 10 SAR | 60% |

| B | 60 SAR | 20 SAR | 40% |

| Fixed costs for all products | 80,000 |

Required: Calculate break-even volume for each product.

First: Calculate the average selling price: = Product selling price × Sales mix ratio

| Product | Unit Selling Price | Sales Mix Ratio | Average Selling Price |

| A | 40 SAR | 60% | 24 SAR |

| B | 60 SAR | 40% | 24 SAR |

| Average selling price for sales mix | 48 SAR |

Second: Calculate the average variable cost for the sales mix: = Variable cost per unit × Sales mix ratio

| Product | Variable Cost per Unit | Sales Mix Ratio | Average Variable Cost |

| A | 10 SAR | 60% | 6 SAR |

| B | 20 SAR | 40% | 8 SAR |

| Average variable cost for sales mix | 14 SAR |

Third: Calculate average contribution margin for sales mix: Average selling price for sales mix - Average variable cost for sales mix = 48 - 14 = 34 SAR

Fourth: Calculate break-even volume for sales mix: Fixed Costs ÷ Average contribution margin for sales mix = 80,000 ÷ 34 = 2,353 units

Calculate break-even volume for product (A) = Break-even volume for sales mix × Sales mix ratio = 2,353 × 60% = 1,412 units

Calculate break-even volume for product (B) = 2,353 × 40% = 941 units

When Does a Project Start Generating Profits After Break-Even Analysis?

A project starts generating profits after exceeding the break-even point. This means that every additional unit sold after the break-even point contributes to profit, because fixed costs have already been covered, and variable costs per unit remain constant.

For example, let's assume that a company sells its product at 90 SAR per unit, variable cost per unit is 40 SAR, and total fixed costs are 35,000 SAR, then the break-even point in units would be 35,000 / (90 - 40) = 700. After selling the 701st unit, the company starts generating profits.

How Does Daftra Help You Calculate Break-Even Point?

Revenue and expense reports in Daftra's sales software provide indicators that you can input into the break-even point calculation equation to easily reach the desired result without needing many preliminary steps.

In conclusion, it has become easy to know how to calculate break-even points, whether for a single product or multiple products. And also knowing that the break-even point has a significant role in determining future decisions and forecasting profits and losses.

Break-even point can be relied upon initially, as it is considered an indicator for several factors, such as determining sales volume, determining units produced to avoid losses, and others, as disclosed in this blog.

Frequently Asked Questions

What is better for break-even points: increase or decrease?

To add a safety factor to the break-even point, it is preferable to have it increased, where the number of units produced becomes larger than what should be produced, and thus, when sold, revenues automatically increase. This makes the increase in targeted revenues larger.

What is the break-even point in restaurants?

Break-even point in restaurants deals with more than one meal and food item. To calculate, we use break-even points for multiple products, and based on experience, meals with high sales mix ratios and others with low sales mix are determined.

What is the break-even point in a feasibility study?

Before starting any project, the implementer needs to know the total units required to be sold to start generating profits. By determining the number of units, one can easily predict the duration the business needs to continue before starting to generate profits.

What is the concept of break-even analysis?

The concept of break-even analysis addresses the relationship between sales achieved by units, their cost, and the net profit realized from them.

What is the break-even point by value?

Break-even point by value is the moment when sales volume is achieved, after which the business starts generating profit. A company can achieve sales estimated at one million riyals without generating profits yet, but upon entering the first riyal after the million, the company began achieving its profits.

What are the elements of the break-even point?

1- Number of units (sales volume) 2- Total revenue achieved (unit price multiplied by number of units) 3- Total cost (fixed cost + total variable cost for units produced)

What is the break-even point in entrepreneurship?

Break-even point represents great importance in entrepreneurship as it helps entrepreneurs evaluate the feasibility of their business ideas, and it contributes to financial risk management. The break-even point provides an understanding of financial risks.

Calculating break-even points helps make informed decisions about investment and expansion by determining how changes in costs and selling prices affect profitability, allowing effective adjustment of pricing and cost strategies.

What are the determinants of the break-even point?

There are four determinants of the break-even point: fixed costs, variable costs, selling price, and product volume.

What are the assumptions of break-even analysis?

Break-even analysis assumptions include: a constant selling price that does not change according to sales volume or market conditions, determining fixed and variable costs, and ensuring that sales equal production volume. Using groups of similar products in calculating the break-even point facilitates calculations and obtains accurate results.

What are the disadvantages of break-even points?

Break-even point calculation factors focus on stability in price, market, quantity, and other factors without taking into account other external factors such as competition, demand, inflation, and others.

What is the cost equilibrium point?

Cost equilibrium point and break-even point are the same thing. Both terms refer to the point where cost equals revenue, meaning there is no loss or profit.

When does the break-even point become null?

The break-even point becomes null when revenues equal costs, whether fixed or variable costs.