Reverse Charge Mechanism (RCM) in UAE VAT: Rules & Reporting Guide

Table of contents:

The UAE has a solid VAT handbook to make people and businesses compliant with the VAT. The UAE VAT Law has mandated a few transactions as a VATable transaction. Among these transactions, some taxes are paid by suppliers while some taxes are paid by buyers.

The Reverse Charge Mechanism (RCM) plays a vital role in the UAE VAT framework, aiming to simplify VAT collection on cross-border transactions and guarantee compliance for imports. In contrast to the conventional VAT procedure in which the supplier bills the customer for VAT, RCM transfers the obligation of reporting and remitting VAT from the supplier to the purchaser or recipient of goods or services.

What is Reverse Charge Mechanism (RCM) in UAE VAT?

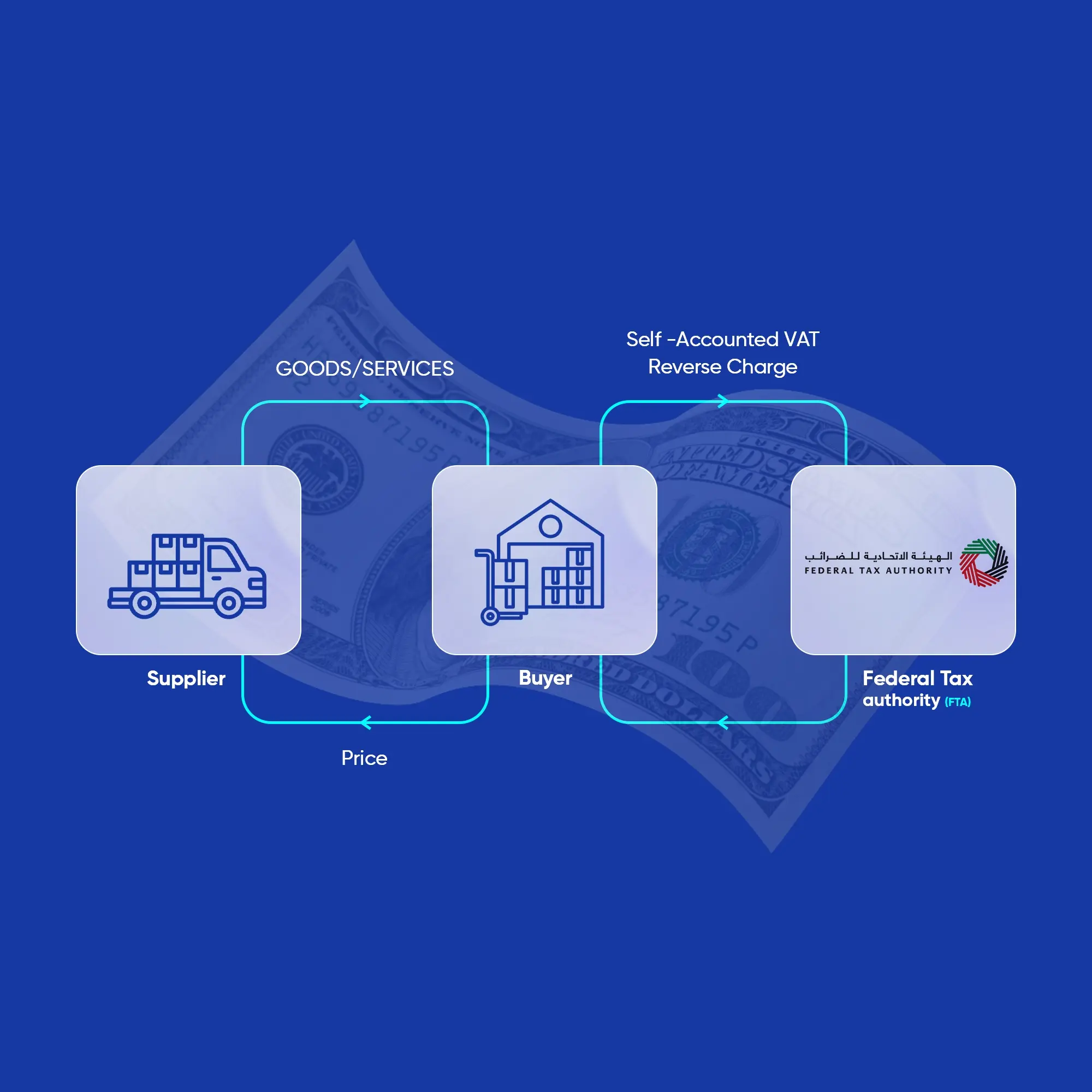

The Reverse Charge Mechanism (RCM)is a regulatory procedure where the tax liability for the supply of goods or services is shifted from the supplier to the recipient. Under the standard, or forward charge mechanism, the registered supplier is responsible for collecting the charge from the buyer and paying that VAT amount directly to the Federal Tax Authority (FTA). It applies under Article 48 of the VAT Law and related Cabinet Decisions, and businesses must report it in the VAT 201 return.

When a sale is made, it's normally the supplier who is obliged to account for any VAT due. Under some circumstances, though, it's the responsibility of the recipient. This is known as the Reverse Charge Mechanism, and it's important to be aware of when it applies to your business. Reverse charge VAT shifts the responsibility for VAT reporting from the supplier to the buyer, helping to simplify cross-border transactions within the UAE. While it reduces the need for VAT registration in other countries, the rules can vary depending on the situation.

Helpful Template: VAT Return Form 201 Template in UAE

When does Reverse Charge apply in UAE? (Goods, Services + Domestic cases)

Reverse charge VAT shifts the responsibility for VAT reporting from the supplier to the buyer, helping to simplify cross-border transactions within the UAE. While it reduces the need for VAT registration in other countries, the rules can vary depending on the situation.

Domestic Business Covered by the Reverse Charge Mechanism

- Imports of services and goods from outside the UAE: RCM applies when a VAT-registered business in the UAE imports goods or services from a supplier located outside the UAE. This includes suppliers from GCC and non-GCC countries who are not registered for VAT in the UAE.

- Oil, gas and hydrocarbons for resale or energy production: Article 48 provides domestic reverse charge when a VAT-registered buyer acquires specified products for resale, or for producing or distributing energy.

- Electronic devices supplied B2B for resale or manufacturing: Starting from 30 October 2023, mobile phones, computers, tablets and related parts are reverse-charged to the VAT-registered buyer when the relevant conditions and buyer declarations are met.

- Precious metals and precious stones: Since 26 February 2025, Cabinet Decision No. 127 of 2024 applies reverse charge to a broader list that includes gold, silver, platinum, palladium, and a range of precious stones when traded between UAE VAT registrants.

Read also: Gold Tax in UAE

What services are covered by reverse charge? (common examples)

Think of RCM as making you act as both the customer and your own supplier for tax purposes. You "charge" yourself the VAT and then, in the same breath, "claim it back".

Example 1: Ali owns a retail shop in the UAE and is a VAT registrant. He sometimes procures goods (which is subject to VAT) from a retailer in Berlin, Germany. Mr. Ben, the retailer who sells goods to Ali, is not registered for VAT in the UAE, so he doesn’t have to file taxes for the supply. Ali will have to file taxes through reverse charge for the goods because the supply is from outside the UAE.

Example 2: Mr. John receives digital marketing services from Mr. Mohammed, who is a non-resident supplier in the UAE. According to that, the services are supplied by a non-resident, VAT is accounted for under the reverse charge mechanism. Therefore, Mr. John must account for the VAT due on the imported services in his VAT return.

Who is liable to pay tax under reverse charge?

Under Reverse Charge Mechanism-UAE, the buyer of goods or recipient of services will be liable to pay tax to the government. Thus, the concerned person shall discharge the below responsibilities under the reverse charge mechanism:

- Account for the VAT due on reverse charge supplies

- Claim Input Tax, based on eligibility

- Determine the value of supply on which VAT must be levied

- Pay the VAT to the government

- Maintain the records as proof of tax payment and to claim input tax

How is reverse charge calculated in UAE VAT? (with example)

Under the RCM in the UAE, the responsibility for reporting and paying VAT shifts from the supplier to the buyer (recipient of goods or services). This ensures proper tax collection, especially in cross-border or specific domestic transactions.

How tax payment calculates under RCM?

The recipient calculates VAT on the purchase and reports it as output tax in their VAT return. In the same return, the buyer can claim the same amount as input tax, provided the purchase is for business purposes and eligible for recovery. Since output and input VAT are recorded together, there is typically no immediate cash payment, unless input tax recovery is restricted. VAT is calculated at the standard rate (5%) or as applicable, based on the nature of the supply.

Example: Emirati company in the UAE imports services worth AED 200,000 from a French-based supplier. Under the reverse charge, The Emirati company calculates 5% VAT (AED 10,000), reports AED 10,000 as output VAT and claims AED 10,000 as input VAT.

Don't let RCM errors lead to an unexpected tax bill. Contact Daftra for a comprehensive review of your RCM of imported services.

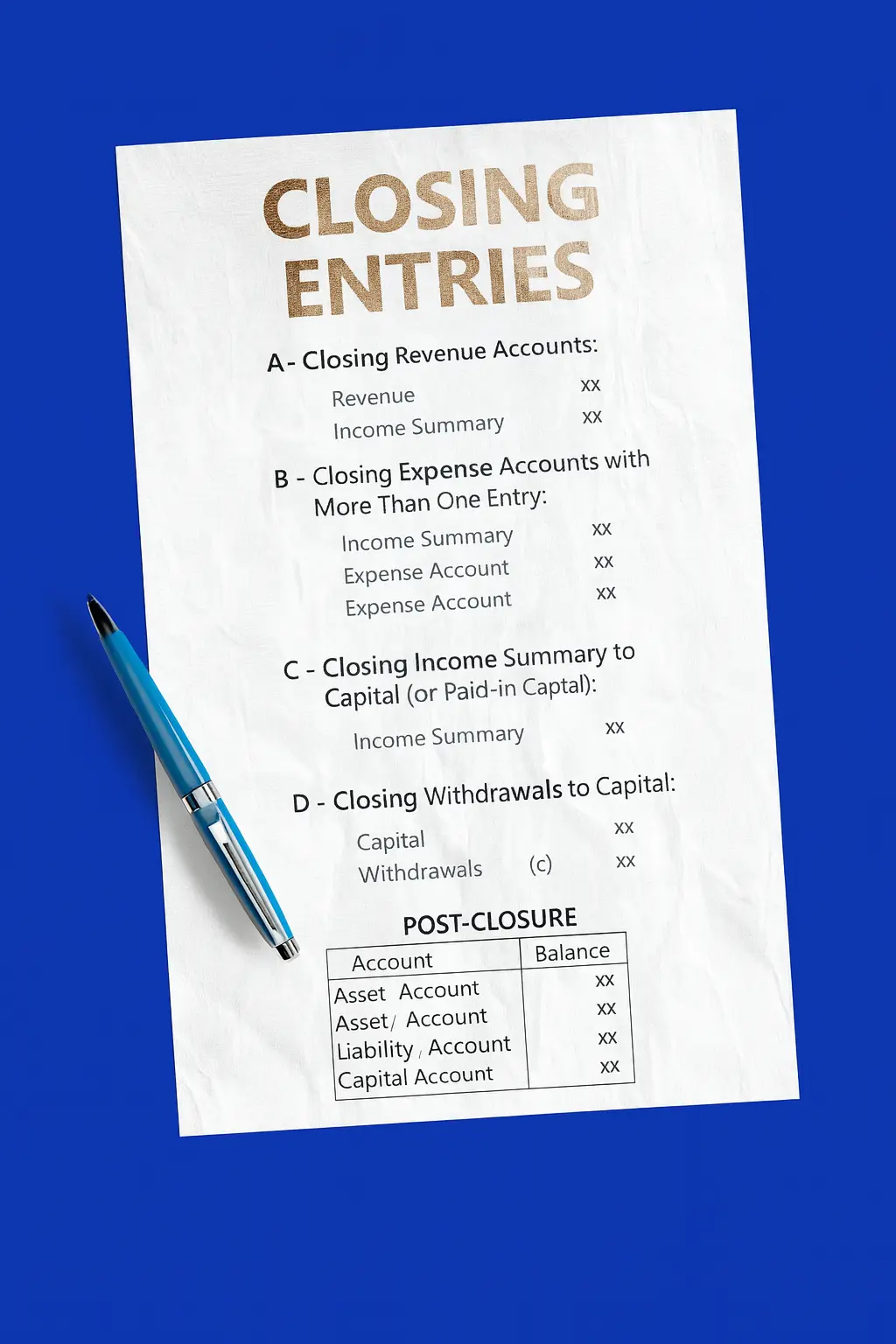

RCM accounting entries (Output VAT + Input VAT) and recoverability

Journal Entries for RCM

Example: AED 20,000 software import. The accounting entries would be:

- To record the expense:

Dr. Software Expense AED 20,000

Cr. Supplier Payable AED 20,000

- To record the RCM VAT transaction:

Dr. VAT Input Tax Recoverable AED 1000

Cr. VAT Output Tax Payable AED 1000

This second entry perfectly captures the dual nature of the RCM on the balance sheet, with the debit and credit netting to zero. Proper account reconciliation is needed to ensure these accounts are cleared correctly upon filing.

VAT Return Filing

On the VAT 201 Return Form, RCM transactions are reported as follows:

Output Tax (The "Charge"): The value of the imported services (AED 20,000) is declared in Box 3 -"Sales and all other outputs," and the VAT amount (AED 1000) is included in the output tax calculation. For goods, it's Box 6.

Input Tax (The "Reverse"): The VAT amount (AED 1000) is claimed as recoverable in Box 10 - "Input tax."

For Input VAT rules and documentation, you should keep the supplier's invoice, proof of payment, and any contracts or agreements related to the supply. For goods (invoices, customs papers, buyer declarations), you may also keep the customs declaration and shipping documents. These are essential for any future FTA audit.

These Input Tax Recovery + Non-Recoverable Input VAT are set out in the FTA VAT Guide, which clarifies how reverse-charged supplies should be declared in the VAT 201 return.

At the end, the reverse charge mechanism (RCM) in UAE VAT is key to a fair and efficient tax system. It helps businesses understand international transactions and electronic purchases better. This knowledge boosts confidence in handling these complex areas.

Read also: How to file VAT return in UAE