Income Statement: Its Equations, Preparation Steps, and the Difference Between It and the Comprehensive Income Statement

Table of contents:

- Key Summary

- What is an Income Statement?

- What are the Components of an Income Statement?

- How to Prepare an Income Statement?

- Key Income Statement Equations

- What are the Types of Income Statements?

- Illustrative Examples of Income Statement Types

- Uses of the Income Statement

- Factors Affecting Income Statement Preparation

- Objectives of the Income Statement

- Importance of the Income Statement

- What is the Comprehensive Income Statement

- Elements of the Comprehensive Income Statement

- The Difference Between Income Statement and Balance Sheet

- Frequently Asked Questions

- How is the income statement generated in Daftra?

The main objective of any organization is to know what its profits and losses are during a specific period, but how can profits and losses be determined?

Any accountant can determine an organization's profit or loss through the income statement because it is responsible for them by identifying all revenues and expenses for each time period. Profits are also an important source for investors, as any investor seeks to invest their money in an organization that has profits and continues operating activities.

Therefore, we present in the following article a comprehensive guide about the income statement, its objectives, and how it works step by step, while clarifying how the income statement can be a tax authority guide to determine what the real taxes are for any organization, and learning about the format of the income statement and the format of the comprehensive income statement.

What is an Income Statement?

The definition of an income statement is that it is a financial statement for any institution that shows its profits and losses, by showing revenues minus expenses. The income statement is also called the profit and loss statement, and the income statement is known by other names such as "operating statement - profit statement - income statement" and other terms that carry approximately the same meaning. The income statement is considered one of the most important four financial statements prepared by the financial accountant, alongside the balance sheet, cash flow statement, and shareholders' equity statement. Therefore, it should also show:

- Business activity details

- The revenue statement shows sales details, cost of goods sold, and elements that demonstrate business continuity.

What are the Components of an Income Statement?

The income statement consists of basic elements that help in making informed and accurate decisions based on the statement results. Learn about the income statement elements in the following points:

- Revenues: All revenues that the organization earns from selling products or services are included.

- Expenses: Here, all expenditures incurred by the organization are determined.

- Profits: Determining any amounts that entered the organization unrelated to work, such as asset sales.

- Losses: Statement of any losses incurred by the organization that are unrelated to work.

.webp)

- Example of the Most Important Income Statement Elements:

| Item | Amount |

| Sales Revenue | XX |

| (-) Cost of Goods Sold / Cost of Sales | (XX) |

| Gross Profit | XX |

| Operating Expenses | XX |

| Operating Profit | XX |

| (-) Other Expenses | |

| Loss on sale of fixed asset | (XX) |

| Depreciation expense | (XX) |

| + Other Revenues | |

| Profit on sale of investments | XX |

| Net Income Before Interest and Taxes | XX |

| (-) Interest expense | (XX) |

| (-) Tax expense | (XX) |

| Net Income/Loss | XX |

Details of what these elements mean and what they indicate:

- Sales Revenue: This term refers to all organizational revenues resulting from sales during the time period covered by the income statement.

- Cost of Goods Sold: This is the production cost for all goods and products, such as raw materials, labor costs, shipping costs, and any other expenses related to packaging and wrapping the product.

- Gross Profit: This is the difference between sales revenue and cost of sales, and is considered an approximate profit figure.

- Operating Expenses: These are expenses spent on business activities, such as equipment expenses and marketing expenses.

- Operating Profit: Operating profit is the profit of a business activity, after deducting all expenses that can be controlled, and differs from operating expenses in that they are expenses not related to operating the business, such as taxes and interest.

- Depreciation Expenses: When purchasing an asset (such as equipment), and after a period of time, it depreciates, this means there are depreciation expenses that must be incurred.

- Profit on Sale of Investments: These are profits not related to work but rather from selling one of the assets, resulting in profits.

- Interest Expenses: Any business that has bank loans and therefore has interest installments paid during the period covered by the income statement.

- Tax Expenses: This term refers to the amount that will be paid to the tax authority.

How to Prepare an Income Statement?

The income statement is prepared through a series of basic steps that must be followed to implement a comprehensive and accurate statement that includes all statement items due to the future decisions that depend on it. Learn how to prepare an income statement in the following points:

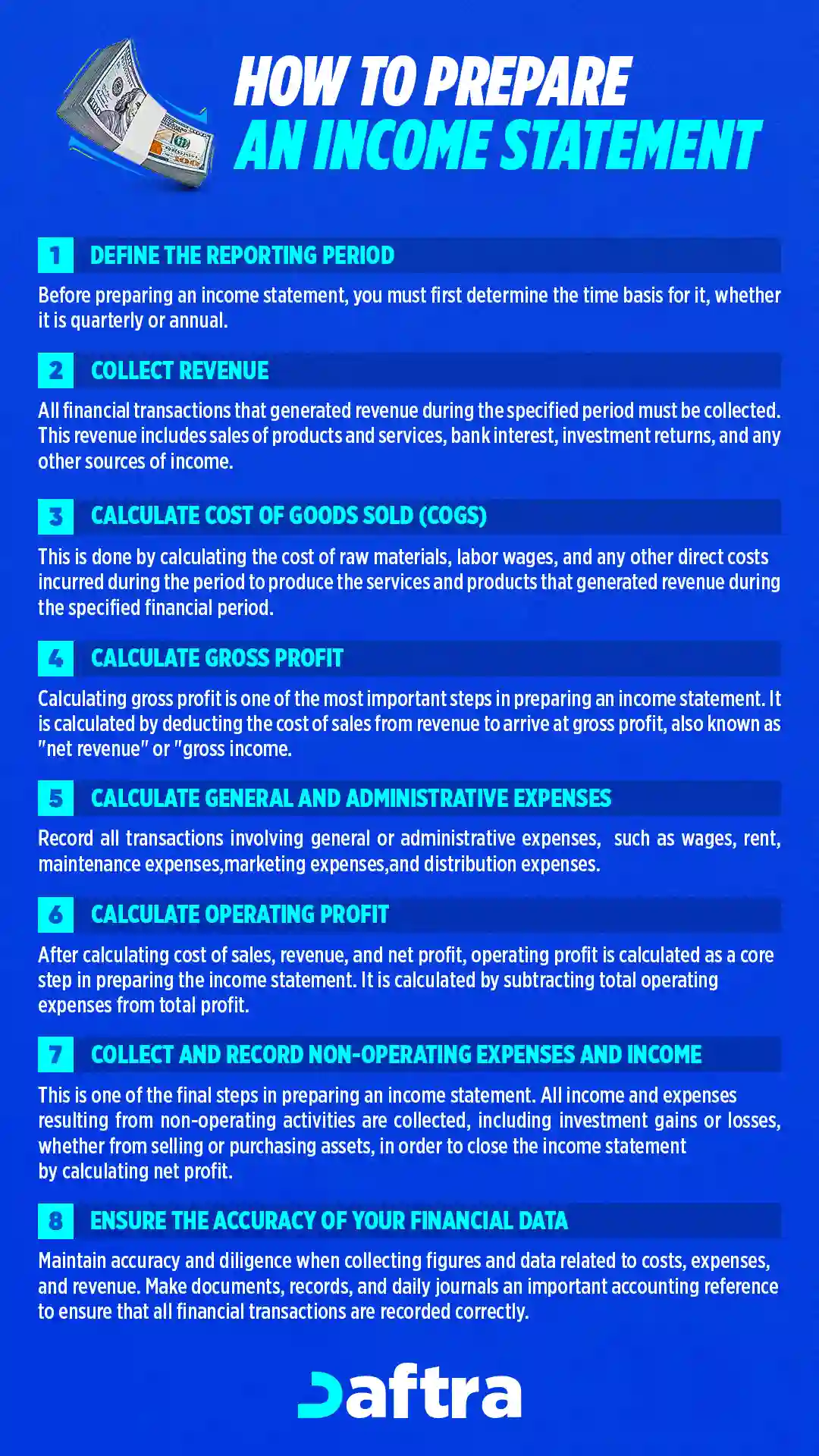

1- Determine the Time Period

Before starting to prepare the income statement, you must first settle on its time basis, which can be quarterly or annually.

2- Collect Revenues

All financial transactions that resulted in revenues during the specified time period must be collected. Forms of these revenues include sales of products and services, bank interest, investment returns, and any other income sources.

3- Calculate Cost of Goods Sold

This is done by calculating the cost of raw materials, labor wages, and any other direct or indirect costs related to producing the services and products that generated income during the specified financial period. The formula for cost of goods sold is:

Cost of Goods Sold = Beginning Inventory Balance + Inventory Purchases During the Period - Ending Inventory Balance

4- Calculate Gross Profit Margin

Calculating gross profit margin is considered one of the most important steps in preparing the income statement. It is done by subtracting the cost of sales from revenues to obtain the gross margin known as "net revenues" or "gross profit."

5- Calculate General and Administrative Expenses

Recording transactions involving general or administrative expense outflows, such as wages, rent, maintenance expenses, marketing expenses, and distribution expenses.is very important. These records, appearing in the journal or ledger and trial balance, are primarily used in preparing the profit and loss statement and identifying net revenues and operating profit.

6- Calculate Operating Profit

After calculating the cost of sales, revenues, and net profit, operating profit is calculated as a basic part of the income statement preparation steps by subtracting total operating expenses from total gross profit.

7- Compile and Balance Non-Operating Expenses and Revenues

This step is considered one of the final steps in how to prepare an income statement, where all revenues and expenses resulting from non-operating activities represented in fixed asset investments, whether through sale or purchase, are collected. This is to close the income statement by calculating net profit through adding the value of operating profit and non-operating revenues and subtracting them from non-operating expenses to obtain (net profit or net income).

8- Ensure Accuracy of Your Financial Data

Observe accuracy and investigation standards while collecting numbers and data related to costs, expenses, and revenues. Make documents, records, and journals an important accounting reference to ensure that all financial operations are recorded correctly as intended. Verify the amounts allocated to transactions in records and actual figures, and the differences between revenues and expenses resulting from these transactions.

Key Income Statement Equations

Here are the key income statement equations for determining revenues, gross profit, and operating profit to determine the extent to which a company achieves profit during a specific time period:

- Revenue = Product Price × Quantity Sold

- Gross Profit = Revenue - Cost of Sales

- Operating Profit = Gross Profit - Non-Operating Expenses

What are the Types of Income Statements?

There are two types of income statements: single-step and multi-step. Each method displays statement items in a specific way to clarify the company's financial picture. The two types are:

1- Single-Step Income Statement:

The single-step income statement combines all revenues in one step, meaning both operating and non-operating revenues, matched against expenses, whether operating or non-operating. Total expenses are subtracted from total revenues to arrive at net profit or loss. This type of income statement is not useful for evaluating the financial performance of operating activities because it does not calculate operating profit.

2- Multi-Step Income Statement:

The multi-step income statement separates operating revenues from non-operating revenues, as well as expenses. Therefore, revenues are detailed as well as expenses, and in this type, we reach the organization's operating profit. The multi-step income statement takes longer to complete as all its data must be written in detail.

Illustrative Examples of Income Statement Types

Here are some illustrative examples of all types of income statements and how to prepare them easily. Here are solved exercises:

1- Practical Example of Single-Step Income Statement

Organization (A) had sales revenue for 2019 of 100,000 Saudi riyals and investment revenue of 75,000 Saudi riyals. There were expenses during the period, divided into:

- Operating expenses: 40,000 riyals

- Marketing expenses: 15,000 riyals

- General and administrative expenses: 10,000 riyals

- Other expenses: 5,000 riyals

- Required: Determine the net income for this organization for 2019 according to the single-step income statement:

| Description | Item | Amount |

| Revenues | Sales Revenue | 100,000 |

| Investment Revenue | 75,000 | |

| Total Revenues | 175,000 | |

| Expenses | Operating Expenses | 40,000 |

| General and Administrative Expenses | 10,000 | |

| Marketing Expenses | 15,000 | |

| Other Expenses | 5,000 | |

| Total Expenses | (70,000) | |

| Net Profit | Revenues - Expenses | 105,000 |

2- Practical Example of Multi-Step Income Statement

Organization (B) had sales revenue in 2020 estimated at 100,000 riyals, and the cost of goods sold during this period equaled 20,000 riyals:

- Total operating expenses equal 20,000 riyals

- The organization sold one of its buildings, resulting in a loss of 5,000 riyals

- Equipment depreciation expense for this period equals 4,000 riyals

- In May 2020, one of the organization's lands was sold, resulting in a profit estimated at 20,000 riyals

- The organization borrowed an amount from the bank; interest expense for this period was calculated at 10,000 riyals

- Tax expenses were calculated at 7,000 riyals

Required: Calculate net income for 2020 according to the multi-step income statement:

| Description | Amount |

| Sales Revenue | 100,000 |

| (-) Cost of Goods Sold / Cost of Sales | (20,000) |

| Gross Profit | 80,000 |

| Operating Expenses | (20,000) |

| Operating Profit | 60,000 |

| (-) Other Expenses | |

| Loss on sale of fixed asset | (5,000) |

| Depreciation expense | (4,000) |

| + Other Revenues | |

| Profit on sale of investments | 20,000 |

| Net Income Before Interest and Taxes | 71,000 |

| (-) Interest expense | (10,000) |

| (-) Tax expense | (7,000) |

| Net Income/Loss | 54,000 |

Uses of the Income Statement

Business plans in organizations are closely linked to the income statement, and the revenue and expense statement is considered the mirror reflecting the financial and operational performance of the institution. Therefore, before preparing the business plan and its objectives, you must first pay attention to variables in product prices, operating costs, and production volume, which the income statement expresses. The following are the most prominent uses of the income statement:

1- Compliance with Accounting Principles and Standards

One of the basic uses of the income statement is compliance with international accounting standards and financial compliance requirements, which require companies to adhere to principles of transparency and accountability in presenting financial reports based on correct and documented data.

2- Making Important Operational Decisions

The income statement is used to make necessary operational decisions related to reducing expenses or identifying areas that need improvement to increase productivity and profit, efficiently reallocating resources, and managing costs. All these procedures depend on analyzing expenses, revenues, and profit rates that the income statement tells us about.

3- Evaluating the Organization's Operational Efficiency and Risk Management Capability

The income statement is considered one of the most important financial analysis tools used in evaluating the company's operational efficiency and its ability to generate positive cash flow, as well as evaluating the institution's ability to bear risks, meet financial obligations, achieve sustainable profits, and maintain financial stability. This is done by considering important indicators resulting from the income statement, such as operating and gross profit.

4- Using the Income Statement to Improve Company Financial Performance

The income statement is used to improve the company's financial performance through the following uses:

- The income statement can be used to identify new investment opportunities through the accurate financial data it provides about revenues and expenses, profits and losses, enabling the company to analyze its financial performance and identify areas for improvement or expansion, and new investment opportunities.

- Using the income statement to calculate return on investment (ROI) in a service or product, and then identifying the most profitable activities to enhance financial sustainability and increase profits.

- Using the income statement as one of the most important comparative financial statements enables the company to compare its performance across different time periods, or compare with competitors in the same field of work, helping to better identify strengths and weaknesses and then make more sound decisions that help with growth and financial expansion.

- Benefiting from the income statement in identifying gaps that can be exploited in the market, with the aim of maintaining the company's competitive position. Through the information that the income statement provides about profits and costs of products and services in markets, new ideas can be developed to improve financial performance.

Factors Affecting Income Statement Preparation

The income statement is affected by several factors, and consequently, these factors affect the accuracy of financial reports. Among the most important factors to pay attention to when preparing the income statement are:

1- Compliance with Accounting Standards and Policies

Compliance with accounting standards is one of the most important factors affecting the accuracy of the income statement during preparation and its freedom from errors, as well as choosing the accounting policy that suits the nature of the company's work, such as choosing methods of recognizing and recording revenues either on a sales basis, or percentage of completion basis in projects especially in long-term projects such as construction projects, or on a cost basis, or on an installment basis, or the revenue recovery method which is one of the most conservative methods because revenues cannot be recognized until all expenses are incurred and calculated.

2- Nature of Expense Classification and Cost Management

Correctly classifying expenses into operating and non-operating expenses affects the accuracy of financial analysis, and cost management methods also affect net profit.

3- Review and Credibility

Review and audit processes of data entered into the income statement are among the most important factors affecting the reliability and credibility of financial information from the income statement, such as profits, thus affecting the confidence of users, such as investors and others, when using this information to make some crucial decisions.

Objectives of the Income Statement

There are many objectives that the income statement helps you achieve, and these objectives revolve around helping the institution improve the financial and investment efficiency of business activity. Among the most important objectives of the income statement:

- Determining the organization's performance and helping investors evaluate the investment options available to them, represented in different companies and institutions.

- Determining the organization's profitability and interpreting its revenues and expenses.

- Managers rely on the income statement to make future decisions, plan, and create strategies.

- Raising the value of the organization's shares on the stock exchange if there is an increase in profits in the income statement.

- The income statement shows the financial worthiness of the organization in paying its obligations.

- Banks and financial institutions use the income statement as collateral for companies in matters related to loans and other. matters

Importance of the Income Statement:

- The income statement is considered one of the most important accounting operations that must be available in any institution, due to the many advantages it provides:

- The income statement helps summarize all activities that took place in the organization during a specific time period.

- It is considered a good tool for analyzing the organization's performance in the past and present year, and also comparing it with the performance of other organizations in the same industry.

- Through it, future revenues and future growth of the organization can be predicted by analyzing data from past years.

- It provides a detailed statement of the organization's expenses, helping to reduce expenses that are not important.

- It is an important source for completing data for the rest of the organization's financial statements, such as the balance sheet, which can only be completed through income statement data.

What is the Comprehensive Income Statement

The comprehensive income statement is a way to clarify that there are other income sources that can contribute to the organization's growth. Therefore, a comprehensive income statement is prepared that includes all different elements that increase income growth, making it an important tool for stakeholders and investors to assess income growth. Thus, the comprehensive income statement is considered one of the statements published for sources that are interested in increasing investment in the organization.

The comprehensive income statement includes any operations that occurred and led to changes in stockholders' equity, such as increases or decreases in capital and dividend distributions.

Therefore, comprehensive income is the total real income of the organization plus other comprehensive income resulting from foreign currency transactions, increases or decreases in securities available for sale, and others.

Elements of the Comprehensive Income Statement

Elements of the comprehensive income statement or items of the comprehensive income statement are gains and losses. Learn about the components of the comprehensive income statement in the following points with an illustrative example:

- Gains or losses made through foreign currency operations

- Gains or losses in exchange rates

- Gains or losses in buying or selling securities

Comprehensive income is considered to be: Net profit/loss + Total comprehensive income elements.

Here is an example of a comprehensive income statement:

Note: Figures are in thousands of Saudi riyals

| Item | 2019 | 2020 |

| Profit/Loss for the year | 50 | (20) |

| Comprehensive Income/Loss: | ||

| Value of reclassified securities | 20 | 10 |

| Value of foreign currency operations | 75 | (20) |

| Total Comprehensive Income/Loss | 145 | (10) |

In the end, it can be said that the income statement is one of the most important financial statements for any institution and helps in many internal and external decisions. Any error in it threatens many situations in the institution. Therefore, as a financial accountant, you must focus well when preparing the comprehensive income statement.

The Difference Between Income Statement and Balance Sheet

Although both the income statement and balance sheet are of great importance to the organization in terms of management decisions, investor decisions, and tax determination, and the financial accountant does not neglect preparing either the balance sheet or income statement, there is a significant difference between the income statement and balance sheet. The following are the most prominent of these differences:

| Comparison Aspect | Income Statement | Balance Sheet |

| Definition | Expresses the organization's profits and losses, and shows data and information about revenues and expenses that occurred in the organization. | Shows the organization's possession of assets, whether fixed assets or current assets, and also shows various obligations and ownership rights, and expresses the organization's liquidity. |

| Focus | Reflects the company's financial performance. | Reflects the company's overall financial position. |

| Objective | Attracting investors by evaluating the company's ability to achieve profits. | Helps creditors and financiers evaluate the company's ability to meet its obligations. |

| Basic Equation | Net Profit = Operating Profit - Non-Operating Expenses | Assets = Liabilities + Stockholders' Equity |

Frequently Asked Questions

What are the common mistakes individuals make when preparing income statements, and how can they avoid them?

- Overlooking the recording of some revenue sources or recording them incorrectly. Therefore, all revenue sources must be documented, whether from sales, interest, tax revenues, or others.

- Calculating expenses inaccurately. Therefore, a comprehensive review of all operating and non-operating expenses should be conducted.

- Failure to recognize revenues in the specified accounting period for preparing the income statement leads to manipulation of figures and incorrect results. Therefore, recognized accounting standards that determine the timing and methods of revenue recognition must be followed.

- Not reviewing the income statement before submitting or publishing it. Therefore, it's better to prepare the income statement through integrated accounting software, such as cloud-based systems, and have it reviewed by relevant personnel.

How do you evaluate your company through the income statement?

You can evaluate your company's financial performance using the income statement through the following:

- Reviewing and analyzing revenues and comparing them with previous periods to identify income growth indicators.

- Evaluating income diversification sources by examining revenue sources listed in the income statement.

- Analyzing expenses and determining if there are unjustified cost increases, and understanding how non-operating expenses affect net income.

- Calculating net profit margin through the income statement using the income statement equation (net profit margin = net income ÷ sales revenue) to determine the company's efficiency in achieving profit.

- Analyzing gross profit margin and operating profit margin to evaluate production efficiency and operational performance.

- Through income statement results, factors affecting financial performance can be identified, such as the effects of economic changes on sales and profits.

What is the difference between an income statement and net income?

The difference between the income statement and net income is that net income is considered the final result that focuses on the company's ability to achieve profits, while the income statement shows the company's financial and operational performance comprehensively and in detail by focusing on details related to revenues and expenses.

What is the difference between an income statement and a comprehensive income statement?

The main difference is that the comprehensive income statement provides a clearer picture of the company's financial performance because it includes all income statement elements of revenues, expenses, and net profits or losses, in addition to elements that affect the company's net assets and stockholders' equity.

What is the difference between an income statement and a balance sheet?

The main difference between the income statement and the balance sheet is the time period. The balance sheet shows the company's financial position and what it owns in assets and its obligations at a specific moment or date, such as January 1, 2023, while the income statement shows the company's performance and financial position during an extended time period, such as January 1 to March 31, 2023. Despite these differences, it's preferable to use both the balance sheet and the income statement in an integrated manner, as the income statement serves as evidence of the company's profitability and ability to pay any obligations, thus enabling logical and studied decisions regarding the company's current and future financial position.

What account does not appear in the income statement?

Depletion expenses sometimes do not appear in the income statement. Although it's classified as a non-cash expense eligible for tax deduction, it largely appears in the cash flow statement or appears in the balance sheet as an adjusted value on the related asset value.

What is the difference between a cost center and an income statement?

The difference between a cost center and an income statement is that they are two different tools. The cost center focuses on tracking and analyzing all costs specific to departments within the company, while on the other hand, the income statement works to display all revenue and profit data during a specific time period.

What principle is the income statement based on?

The principle on which the income statement is based is either the accrual principle or the matching principle. The accrual principle in the income statement is recording revenues and expenses at the time the transaction occurred.

While the matching principle focuses on recording revenues and expenses at the time the transaction occurred (it's not necessary for cash to be paid or received under this principle).

What is the difference between an income statement and a profit and loss statement?

There is no difference between an income statement and a profit and loss statement. Both express the same definition, importance, and objective. It is a financial report that shows the company's total revenues and expenses during a specific time period.

Does value-added tax appear in the income statement?

Value-added tax appears in the income statement in only two cases: either when purchasing, it appears in the balance sheet under current assets as a debit, and the second case is when selling, it appears in the balance sheet under short-term liabilities as a credit.

How is the cost of sales calculated in the income statement?

Cost of sales in the income statement is calculated using the following equation:

Cost of Goods Sold (Cost of Sales) - Total Revenues.

*Note: Cost of sales appears directly below revenues in the income statement.

What are the disadvantages of a comprehensive income statement?

The disadvantages of a comprehensive income statement include incomplete information. For example, the statement contains unrealized gains and losses, or fluctuations in exchange rates, and others. Additionally, it doesn't provide complete details about cash flows, and finally, it's difficult for non-specialists to read.

What are the types of provisions in the income statement?

Provisions in the income statement play an important role in evaluating financial performance clearly and accurately, and making the best decisions. Here are five types of income statement provisions:

- Allowance for doubtful accounts, meaning uncertainty about customers paying their debts

- Provision for asset price decline, meaning a decrease in fixed asset values

- Asset depreciation provision, which covers the cost of replacing fixed assets

- Tax provision, which estimates future tax liability

- End-of-service gratuity provision, which covers employee termination costs near the end of their employment contracts

Does accrued revenue appear in the income statement?

Yes, accrued revenue appears in the income statement. Revenue is recorded in the income statement even if it hasn't been collected yet, for the purpose of accurate evaluation of the company's financial performance.

What is the cost of sales in the income statement?

Cost of sales in the income statement is the cost of goods sold and appears directly below revenues in the income statement.

What are financial investments at fair value through comprehensive income?

Financial investments at fair value through comprehensive income is a method used to classify types of financial investments and record changes that occurred in fair value. In other words, it's recording gains and losses resulting from financial investments.

Financial investments at fair value are recorded within stockholders' equity in a separate line item.

What account appears in both the income statement and balance sheet?

Retained earnings are the account that appears in both the income statement and the balance sheet.

What is the difference between an income statement, a balance sheet, and a cash flow statement?

The difference between the income statement, balance sheet, and cash flow statement is their presentation of different information and data. Each plays a special role in clarifying and evaluating financial position from different aspects.

The income statement focuses on showing profits and losses during a specific time period.

A balance sheet focuses on presenting assets, liabilities, and stockholders' equity during a specific time period.

The cash flow statement focuses on showing money coming in and going out of the company's accounts during a specific period.

What is the difference between a trading account and an income statement?

The difference between a trading account and an income statement lies in scope and purpose. A trading account focuses on determining gross profits and losses resulting from direct buying and selling operations with customers. On the other hand, an income statement focuses on presenting the company's revenues and expenses, whether direct or indirect.

What is the difference between a trial balance and an income statement?

The difference between a trial balance and an income statement lies in the objectives achieved. Trial balance focuses on collecting accounts in the general ledger to verify their accuracy and the balance of account balances. The income statement presents both revenues and expenses during a specific time period.

What are accrued expenses in the income statement?

Accrued expenses in the income statement are expenses that haven't been paid yet and are considered an obligation on the company that must be paid later.

Do provisions appear in the income statement?

Yes, all types of provisions appear in the income statement and also in the balance sheet.

What is net income in the income statement?

Net income in the income statement is the amount remaining from revenues achieved by the company after deducting all expenses, taxes, and direct and indirect costs to determine net profit.

Do purchases appear in the income statement?

Yes, purchases appear in the income statement after subtracting the cost of goods sold and operating expenses from revenues.

What is the beginning inventory in the income statement?

Beginning inventory in the income statement is the amount paid for the cost of goods in inventory at the beginning of the accounting period.

Cost of Goods Sold = Ending Inventory - Cost of Goods Available for Sale.

Where are credit sales recorded in the income statement?

Credit sales are recorded in the income statement under sales revenue (which is an increase in revenues whether the amount was received or not) in the accounting period when the sale transaction occurred.

What is the sales discount allowed in the income statement?

Sales discount allowed in the income statement is a discount granted by the seller to the buyer to encourage early payment. It's recorded in the income statement under expenses.

How is the income statement generated in Daftra?

Most business activities rely on the income statement to estimate net profit or loss and predict growth or decline in company indicators. In Daftra, once you select the income statement report from the general accounting program reports in Daftra, the report is generated automatically and instantly. Then you can share the report with investors, potential partners, and your employees. You won't need strong accounting knowledge to understand the report and make critical financial and administrative decisions based on it.

.webp)

Conclusion In conclusion, the income statement is one of the financial analysis tools that reflects the essence of business activities in organizations, through its accurate information that clarifies the financial health of the entity based on performance analyses related to profit and loss ratios. This information can then be used to identify financial strengths and weaknesses, enabling wise financial decisions that lead to success and economic sustainability. Therefore, don't overlook the importance of preparing the income statement correctly and ensuring its information accuracy, as it will determine the fate of a large part of your financial stability and success.